AGM Alts Weekly | 11.17.24: Stuck in the middle

AGM Alts Weekly #78: Making private markets more public, every week.

👋 Hi, I’m Michael.

Welcome to AGM, the meeting place for private markets.

I’m excited to share my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in private markets so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Presented by

In today’s data-intensive, fast-paced financial environment, alternative asset managers face overwhelming data volumes that challenge traditional valuation approaches and seriously hinder accurate, timely reporting to LPs.

73 Strings leverages proprietary AI algorithms to enhance transparency and efficiency by automating data collection, portfolio monitoring, and valuations. Their platform delivers faster, more accurate insights, ensuring data integrity, traceability, and auditability while boosting operational efficiency.

Discover how 73 Strings revolutionizes asset management with advanced technology and AI-driven workflows.

Good afternoon from London, where I’m here for a week of meetings and to speak at an event organized by Citywire with alternative asset managers.

Stuck in the middle

Being in the middle can be hard. Just ask any middle child.

As private markets mature, the gap between the haves and the have-nots appears to be widening.

A few weeks ago, Sujeet Indap of the Financial Times authored a Lex opinion piece titled “A thinning of the big private equity herd is coming.”

He started his piece with an anecdote from a recent investor event, where he said that a “Goldman Sachs banker … repeated a well-worn joke about private equity executives investing their final-ever funds: the punchline was that the PE executives just did not know that their demise had arrived.”

Indap went on to list off a number of concerns about the growing landscape of private equity funds and, how it could lead to lower returns, challenged fundraising efforts, and ultimately, a thinning of the market.

Fundraising figures have stalled in recent years. As the number of private equity firms grew over the past five years by 50%, ballooning to over 18,000 private funds in the US, according to data compiled by the Securities and Exchange Commission, firms looking to fundraise have faced significant headwinds as of late.

It’s notable that fundraising for private markets funds is still significantly higher than a decade ago, but it’s also worth wondering which funds are receiving that capital.

Blue Owl put out great research in January of this year in their 2024 GP Strategic Capital Outlook paper, highlighting that the top 10 funds are increasingly raising the lion’s share of the assets.

This trend is certainly the case in private equity, with over 25% of the capital from 2022-2023 flowing into the industry’s top 10 managers.

Blue Owl’s September 2024 Pulse Check further highlights that the big are the beneficiaries.

Funds under $1B raised the smallest percentage of capital compared to their $1-5B and $5B+ sized counterparts in 2023, as they have since 2009. Funds sized $1-5B AUM didn’t fare much better. Of late, it’s been the $5B+ funds that have raised more capital in aggregate.

While personalization and customization are making its way to the wealth channel, it’s hard to see why the trend of the big getting bigger won’t continue to persist.

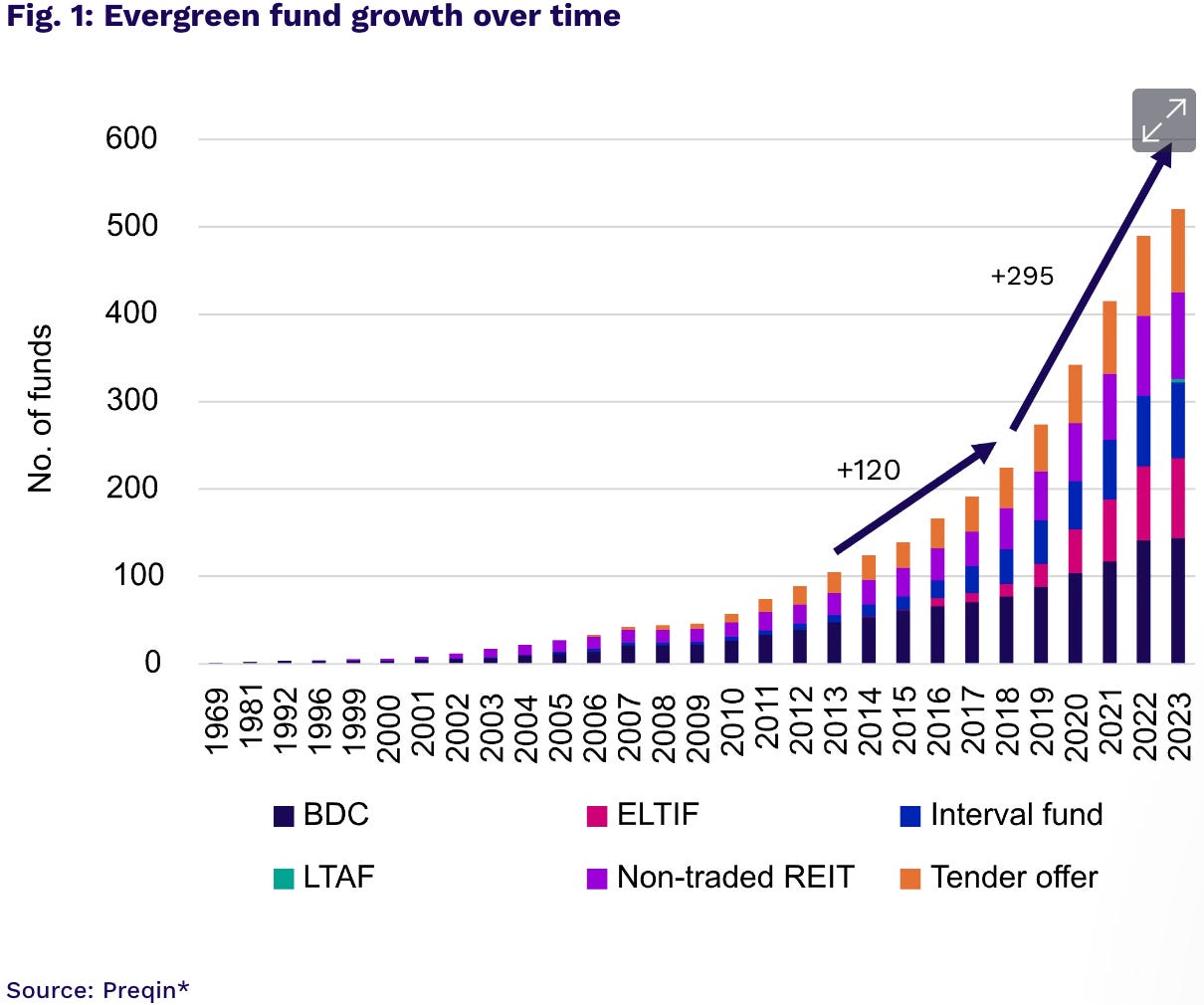

In fact, with the growth of evergreen funds and the focus that the largest alternative asset managers have on productizing and distributing evergreen fund structures to the wealth channel, the gap should only widen.

And it’s the funds in the middle whose future appears to be most in peril. The largest firms have the resources, scale, capital, and brand to create, manufacture, and distribute evergreen funds (and closed-end funds). They have the ability and heft to win their spot on private bank menus. They have the scale and headcount to distribute evergreen funds to the wealth channel, where education and time spent helping the wealth channel is critical (well, at least until model portfolios go mainstream).

The coming consolidation

A little over a year ago, $150B AUM Partners Group CEO Dave Layton said that “private markets has entered a new phase of maturation and consolidation.”

Citing fundraising pressures, higher interest rates, increasing regulatory costs, an intensifying focus on M&A, and the industry’s focus on the wealth channel, Layton said he foresees the scaled platforms as those best positioned to navigate the current industry landscape. So much so, in fact, that Layton predicted that “we could see the current 11,000 or so industry participants shrink to as few as 100 next-generation platforms that matter over the next decade.”

Layton went on to say something crucially important: “There is a real bifurcation between the managers that can raise money and those that cannot. This will accelerate the process of natural selection as the industry grows in size.”

Firms both large and small understand this natural selection. Large firms understand that they have to acquire capabilities and expand footprint to grow. Smaller firms understand the uphill battles they might face in scaling alone — and see the value of leveraging the brand, reach, and resources of a bigger platform.

That’s why we’ve seen a raft of acquisitions from many of the industry’s largest firms. They’ve leveraged their public currency to buy managers in areas that expand their reach by sector / strategy, geography, or LP base.

A 2023 Bain & Company report highlighted the various rationales for alternative asset manager M&A. Half of recent M&A (up to 2023) was for asset class expansion, with (unsurprisingly) credit being the most popular capability for the acquiring alternative asset managers to add to their platform.

While there’s been an explosion of alternative asset manager acquisitions in recent years, it’s been relatively contained to a smaller cohort of firms.

The acquiring firms? In most cases, the acquirers are publicly traded alternatives managers, as Bain’s report finds.

Acquisitions are much easier for firms that are publicly traded. They have the balance sheet, currency in the form of stock, and the ability to access debt to finance transactions if necessary.

Global scale also enables for the creation of a brand that’s not possible for managers in the middle. And, as we’ve discussed in the past, the importance of brand is even more critical for firms that want to work with the wealth channel.

This feature is yet another reason for a widening of the haves and have-nots in private markets. The firms with the most size and scale stand to benefit in ways that smaller firms cannot.

If it’s the survival of the fittest, size will matter

In Partners Group’s Dave Layton’s comments about “natural selection” of asset managers, size will matter in the survival of the fittest.

For an alternative asset manager that’s thinking about growing or staying the same, in almost virtually every scenario, if the goal is to continue to build the firm, the right strategic decision is to grow AUM.

All roads really do lead to growth, even if investment performance diminishes nominally. Purely from a business perspective (I’m not talking from the LP’s perspective), the managing partners of an alternative asset manager will likely choose growth of AUM every time. Increased AUM grows fee-related earnings, resulting in more revenues for the management company.

Increased AUM also enables the firm to put more capital behind larger opportunities, which are more likely to have a better risk / reward (but not necessarily multiple on invested capital). After all, if the manager’s own GP commitment and carry are at stake, sometimes they might choose a less risky but surer bet.

A larger firm also enables for the manager to attract and hire more high-quality talent. In an ever-competitive landscape for alternative asset managers, this point shouldn’t be lost.

Perhaps Layton’s prediction will ring true and the industry will see massive consolidation to a smaller number of consequential platforms. But there are also plenty of $1-50B AUM firms that are “stuck in the middle.”

What can those in the middle do to tactically move the chess pieces in their favor?

Strategic partnerships

If a firm wants to maintain some level of independence as a brand or access the distribution capabilities of a larger firm without consolidating into a larger alternative asset manager, they can follow the path of a Churchill or Pemberton. Both firms started by partnering with a larger platform, $1.2T AUM Nuveen in Churchill’s case, and $1.16T AUM Legal & General in Pemberton’s case. Sure, they gave up ownership in their firm, but they also gained immeasurable benefits in the form of initial seed capital, distribution resources, and brand association by joining forces with larger asset managers. Today, Churchill stands at over $50B in committed capital, and Pemberton has over ~$18B AUM.

“Riches in niches”

A smaller firm can carve out a niche by focusing on a category that’s not currently big yet, but will undergo consolidation as larger alternative asset managers will look to buy that capability rather than build.

Sports investing is a good example. As institutional investor interest in sports grows — and as leagues open up to private equity investors — there will be opportunities for sector specialists to emerge. Sure, sector-focused firms like Arctos, Avenue, RedBird, and others and larger firms like Ares, CVC, and others are building strong brands in sports investing, but given the size of the opportunity, there’s likely room for more funds in this space. Perhaps some large alternative asset managers will house sports investments under their media or consumer investment strategies, but sports might be a big enough opportunity where it deserves its own standalone strategy / fund where LPs allocate solely to sports. There’s certainly a case to be made for LPs to allocate to a standalone sports strategy, particularly when there’s low correlation to other asset classes, as this data from Arctos (in an Akin Gump report) illustrates.

Private equity and credit secondaries, GP stakes, infrastructure, and venture capital / growth equity appear to be other private markets strategies that could be on the radar of scaled firms that are looking to expand beyond their core areas of focus.

Figure out your customer

For a manager in the middle, it’s critical for them to hone in on their ideal LP customer profile and where they can differentiate for that LP base. Is there a strategy in which they can excel as a firm? Is there a strategy where scale is the enemy of performance and differentiation? There are still enough “riches in niches” in private markets where sometimes size will be the enemy of returns. Performance should beget popularity. LPs will want to allocate to firms that generate strong performance. If performance can be sustained even as fund size increases, then a firm may have found its calling card.

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

Post of the week

A few months ago, Blackstone’s Global Head of Private Wealth Solutions Joan Solotar highlighted the need for large scale capital to invest into the growing trend of data center demand due to the growth of AI by sharing a CNBC interview done by her colleague, Kathleen McCarthy Baldwin, Blackstone’s Global Co-Head of Real Estate.

More on data centers as an investment below in the Weekly news recap.

AGM News of the Week

Articles we are reading

📝 Stonepeak to acquire specialist lender for digital infrastructure push | Madeline Shi, PitchBook

💡PitchBook’s Madeline Shi reports that $70B AUM infrastructure alternative asset manager Stonepeak Partners has agreed to acquire specialist private credit investor Virginia-based Boundary Street Capital. Boundary has over $700M in capital commitments and lends to digital infrastructure, digital services, and enterprise software companies. This transaction will allow Stonepeak’s credit team to bolster its investment capacity in digital infrastructure. Data center investing is a popular area of the market — and for good reason. Data center demand is growing due to the continued migration to the cloud and the rise of spending on IT capacity for generative AI. Tech titans like Amazon and Microsoft have been investing billions of dollars into building new data centers. But it won’t only be the large tech companies that build and own data centers. According to a CBRE report on data center investing, the share of leased assets will grow significantly in the coming years, paving the way for investment firms to invest in data centers. Moody’s estimates global investments in new data center capacity will hit $2.2T from 2024 to 2028. Moody’s SVP of Global Project and Infrastructure Finance John Medina said that this wave of investing should lead to a raft of refinancing activities in the coming years. Data center developers finance these projects with credit facilities from banks or equity investments. Once the construction is completed and the data center starts to receive lease payments from tenants, investors and lenders can realize their investment by refinancing the initial funding through debt markets like CMBS and ABS. Private credit ABS is becoming a larger part of this market, with 2023 witnessing 14 data center ABS deals totaling $6.2B, according to a Moody’s report. 2024 has seen the market finance 9 US data center ABS deals worth $4.7B through July 15.

💸 AGM’s 2/20: The explosion of data center demand, in large part due to the growth of generative AI, has a major effect on the worlds of infrastructure, private credit, and real estate investing. The world has an insatiable — and growing — demand for data. A February 2024 report by KKR on digital infrastructure states that in 2024 alone, the world is expected to generate 1.5x the amount of digital data it did two years ago. KKR compares networks of data centers to the railways and pipelines of the 18th-century industrialization. These data centers, says KKR, house the entire value chain of the digital economy. They “support the massive amounts of new data, similar to farming and mining in the physical economy; they refine and analyze data to produce something new, like manufacturers, and they help to distribute data across transmission networks, like logistics hubs and warehouses.” Not surprisingly, demand for data centers has grown rapidly.

According to KKR, vacancy has declined worldwide and is at a decade-low in North America. Most existing data center capacity is under lease. Data centers aren’t just assets owned by big tech companies. They are also very much investable opportunities for infrastructure, private credit, and real estate investors.

Large tech and telecom companies currently account for nearly half of total occupied data center space, according to a CBRE report.

CBRE breaks down data center assets into three distinct categories:

Enterprise: Owned and operated by the companies they support and usually housed on the corporate campus. These assets are not available to outside investors.

Colocation: Where multiple tenants share a data center. In a retail model, tenants rent racks or cabinets in a data center as a service contract that includes power consumption and cooling. Wholesale colocation features longer leases than retail, typically five to 20 years, and each tenant pays for power delivery.

Hyperscale: These high-capacity data centers are the most modern and are designed to meet the significantly higher technical and security requirements of the largest technology companies, as well as their pricing demands.

Many of these hyperscale data centers have high levels of outsourcing, which is changing ownership models. This shift in ownership models is opening up opportunities for investment. Data centers are becoming both larger and highly customized to the needs of tenants. Current demand trends suggest that the number of hyperscale data centers built could double from the 900 built worldwide (which account for 37% of total capacity) and could represent half of all capacity.

So, how can investors access exposure to data centers and the growth in the space? CBRE asks an important preceding question: “are data centers real estate or infrastructure investments? (the below is from CBRE’s report):

Data centers are infrastructure investments because they provide an essential service — in this case, digital interconnectivity, such as data processing, data storage, and computational services that are critical to our daily lives and economic growth. Data centers share similarities to wireline and wireless infrastructure with high barriers to entry due to high cost to build and relatively predictable revenues thanks to medium- to long-term contracts.

Data centers are also real estate investments because they are physical buildings. Like real estate investments, the location and underlying land, such as access to power and the ability to obtain necessary permits, are critical drivers of asset performance and market appeal. Many data centers offer stable rental income, like real estate investments, because they are leased to a third party.

Investors can access exposure to data centers in a few different ways: (1) directly invest in stabilized or near-stabilized data centers, (2) develop new data centers, and (3) acquire a minority or controlling stake in a data center platform.

At present, the US data center market is comprised of large real estate operators and non-traded REITs and big technology companies, which is not surprising due to the scale of capital required to invest into data centers.

There’s another way to access this trend: invest into the GP of a manager like Stonepeak — or a smaller manager that can be acquired by a larger infrastructure manager. That’s precisely what Blue Owl did. Their GP Strategic Capital business took a stake in Stonepeak, which, in turn, has looked to consolidate in the space with this week’s news of their acquisition of Boundary to add private credit infrastructure capabilities to their platform.

All of which brings me back to this week’s news of Stonepeak acquiring Boundary. Of all the strategies within private markets, Infrastructure (and natural resources) are dominated by the scaled platforms, as the below chart from Blue Owl illustrates. The top 10 managers in Infrastructure have raised the overwhelming majority of capital from LPs. This data makes sense. Size and scale are required to invest into large-scale infrastructure projects, such as data centers.

This week’s news is significant because it only serves to reinforce that Infrastructure is a space where we’ll likely see continued consolidation. And the alternative asset managers with the most size and scale stand to benefit disproportionately from this trend.

📝 Apollo Invests in Fintech to Boost Service for Private Markets | Irene Garcia Perez, Bloomberg

💡Bloomberg’s Irene Garcia Perez reports on Apollo’s investment into Vega, a technology platform that aims to provide alternative asset managers with the infrastructure required to help them manage their investors. Apollo and fintech-focused investment firm Motive, which is part-owned by Apollo, are leading a $20M Series A to support the further build-out of Vega’s AltOS software. Alexis Augier, Vega’s founder, said that the idea was rooted in the observation that alternative asset managers require a better comprehensive solution to conduct client services from pre-investment, execution, and post-investment management. “The current landscape offers a bunch of separate point solutions for things like marketing, product discovery distribution, onboarding, or reporting after a transaction, and you’ll need a lot of resources — staffing or time — to put them together and they may still be disjointed,” he said in an interview. Apollo’s Chief Client and Product Development Officer Stephanie Drescher said that the investment in Vega is aligned with the firm’s broader push for innovative solutions that will drive scale and adoption of private markets in wealth channel investors’ portfolios. “The client demand for private markets is far exceeding the markets’ current infrastructure, and we believe that this investment among others help the experience and can be quite valuable to our full range of clients across channels,” she said in an interview. Apollo has become a Vega client, using Vega’s AltOS to run its client services across its institutional, family office, and global wealth channels. “Ultimately as a GP, as an asset manager, we believe that this is the type of technology that will enable us to improve and digitize the client journey and client experience,” Drescher said.

💸 AGM’s 2/20: Client experience is top of mind for alternative asset managers as they look to scale their operations and serve the wealth channel in an efficient but also effective manner. Wealth channel investors and their advisors demand a high-quality client experience. I’ve heard from some on the wealth channel that client experience matters as much as anything else — and that client experience is one of the deciding factors in a wealth manager deciding to invest in private markets. To this end, it’s not surprising that GPs are focused on delivering a high-quality experience. Certain GPs have the size and scale to build out large distribution and operations teams to handle the heavy lift and operational burdens of working with the wealth channel. But, as I discuss in this week’s newsletter, how can firms in the upper middle market and down effectively and efficiently work with the wealth channel? They need a scalable and modular solution that enables them to reach the wealth channel in a way where client experience is front and center.

Vega represents part of the growing trend of software solutions that are being built to focus on the GP. There are now clear winners that have built solutions — and operating systems — for the wealth channel investor, such as iCapital. In the process, platforms like iCapital have become the operating system for both GP and LP alike. A business like iCapital or CAIS couldn’t be built without both the GP and the LP in mind. But it’s interesting — and notable — that a business like Vega is being built to focus on the GP. Vega’s “Alternatives-as-a-service” framework allows any platform or client to connect to an alternative asset manager via API, according to Apollo’s press release on their investment. Vega’s software is designed to “transform internal GP client operations,” according to Jake Walker, Partner and COO of Client and Product Solutions at Apollo. A number of point solutions have been built over the years to try to solve pieces of the value chain. Now, we are starting to see comprehensive solutions built — and Vega has made a big statement by throwing its hat into the ring to build an end-to-end solution for asset managers.

Congrats to Alexis and team on the continued buildout of Vega and the investment by Motive and Apollo teams into the business. It’s great to see both innovation and focus on building solutions that will make private markets more efficient and effective for asset managers and investors.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know, and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Blackstone (Alternative asset manager) - Private Wealth Solutions - Product Marketing, VP, EMEA. Click here to learn more.

🔍 Apollo (Alternative asset manager) - Distribution & Wealth Services Associate. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - RIA, Family Office Business Development - VP. Click here to learn more.

🔍 Carlyle (Alternative asset manager) - Vice President, Client Relationship Manager, Wealth Management (Southeast). Click here to learn more.

🔍 Northern Trust (Asset manager) - Head of Alternatives Sales Specialists. Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Private Wealth Strategy Senior Lead - Click here to learn more.

🔍 Ultimus Fund Solutions (Fund administrator) - Manager, Fund Accounting - InvestOne. Click hear to learn more.

🔍 Hamilton Lane (Alternative asset manager) - Vice President, Private Wealth Operations (Australia). Click here to learn more.

🔍 Arcesium (Financial data management platform) - SVP, Business Development, Private Markets. Click here to learn more.

🤝 Interested in partnering with Alt Goes Mainstream? 🤝

Alt Goes Mainstream is a community of engaged experts and executives in private markets.

Fill out this form using the link below to explore partnership opportunities.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

🎙 Hear Churchill Asset Management by Nuveen’s MD, Senior Investment Strategist & Co-Head of the Chicago Office Alona Gornick discuss the evolution of private credit, the power of permanent capital, and the importance of the product specialist. Listen here.

🎥 Watch Stepstone Private Wealth CEO Bob Long discuss StepStone Private Wealth’s edge and nuances with their evergreen structures in the first episode of “What’s Your Edge.” Watch here.

🎙 Hear $5B AUM Ritholtz Wealth Management’s Director of Institutional Asset Management Ben Carlson bring a wealth of common sense to asset allocation and private markets. Listen here.

🎙 Hear Blue Owl, Inc. Board Member and Blue Owl GP Strategic Capital Senior Managing Director Sean Ward on how $57.8B AUM Blue Owl GP Strategic Capital has pioneered GP staking and transformed GP stakes into an industry. Listen here.

🎥 Watch HGGC Partner, Chairman, Co-Founder & Former NFL Hall of Fame Quarterback Steve Young and True North Advisors CEO & Co-Founder Scott Wood discuss how “the score takes care of itself” on the field and in investing / wealth management. Watch here.

🎥 Watch the first episode of Going Public on Alt Goes Mainstream with Evercore ISI Senior MD and Senior Research Analyst Glenn Schorr as we discuss trends and business models for the publicly traded alternative asset managers. Watch here.

🎥 Watch Eileen Duff, Managing Partner & Chief Client Success Officer at iCapital on episode 12 of the latest Monthly Alts Pulse as we discuss the future of AI and automation in private markets. Watch here.

🎥 Watch Co-Founder & Managing Partner of Cantilever Group and former Goldman Sachs and Broadhaven Capital Partners Partner Todd Owens discuss the middle market opportunity in GP stakes investing. Watch here.

🎙 Hear Intapp’s President, Industries, and Co-Founder of DealCloud by Intapp Ben Harrison discuss how data and automation are transforming private markets. Listen here.

🎙 Hear how a $1.59T AUM asset manager is approaching private markets with T. Rowe Price’s Global Head of Product Cheri Belski in a special live episode of the Alt Goes Mainstream podcast at a Pangea x AGM Breakfast in London. Listen here.

🎙 Hear Bernstein Private Wealth Management’s CIO Alex Chaloff discuss how a $125B wealth manager navigates private markets. Listen here.

🎙 Hear me discuss why and how alts are going mainstream on The Compound’s Animal Spirits podcast with Ritholtz Wealth’s Michael Batnick and Ben Carlson. Listen here.

🎙 Hear Mercer Investments’ US Financial Intermediaries Leader Gregg Sommer and CAIS’ MD and Head of Investments Neil Blundell on following the fast river of alts. Listen here.

🎙 Hear Manulife’s Global Head of Private Markets Anne Valentine Andrews share how to approach building a private markets investment platform at an industry behemoth and the merits of infrastructure investing. Listen here.

🎥 Watch Dan Vene, Co-Founder & Managing Partner, Head of Investment Solutions at iCapital on episode 11 of the latest Monthly Alts Pulse as we discuss the evolution of the industry. Watch here.

🎙 Hear Partners Group’s Co-Head of Private Wealth, Head of the New York Office, Member of the Global Executive Board Rob Collins share the how and why of one of the most exciting trends in private markets: evergreen funds. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, on the AGM podcast discuss driving efficiency across the entire value chain to transform private markets. Watch here.

🎙 Hear VC legend New Enterprise Associates’ Chairman Emeritus and Former Managing General Partner Peter Barris discuss how he transitioned from operator to VC and transformed NEA into a venture juggernaut in the process. Listen here.

🎙 Hear Blue Owl’s Global Private Wealth President & CEO Sean Connor share insights and lessons learned from working with the wealth channel. Listen here.

🎙 Hear Ritholtz Wealth Management’s Managing Partner Michael Batnick share views on how wealth managers are navigating private markets. Listen here.

📝 Read about the evolution of GP stakes, why alternative asset management business models are better than SaaS, and our partnership with Todd Owens and David Ballard at Cantilever, a mid-market GP stakes firm anchored by BTG Pactual. Read here.

🎥 Watch internet pioneer Steve Case, Chairman & CEO of Revolution and Co-Founder of America Online, share lessons learned from building the first internet company to go public and an investment firm built for the Third Wave of the internet. Watch & listen here.

🎙 Hear how Chris Long, Chairman, CEO, and Co-Founder of Palmer Square Capital Management has built a $29B credit investment firm and a winning NWSL soccer franchise, the KC Current. Listen here.

🎙 Hear stories from building market-defining companies Blackstone, Airbnb, and private markets from Laurence Tosi, former CFO of Blackstone and Airbnb and Managing Partner & Founder of $7.6B investment firm WestCap. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear wealth management industry titan Haig Ariyan, CEO of Arax Investment Partners, share his thoughts on the private equity opportunity in wealth management. Listen here.

🎙 Hear Blackstone CTO John Stecher discuss how technology is transforming private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with both a macro and VC lens. Listen here.

📝 Read how 73 Strings CEO & Co-Founder Yann Magnan and team are leveraging AI to build a modern and holistic monitoring and valuation platform for private markets in The AGM Q&A. Read here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, discusses how they approach alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Michael Rutter and Nick Owens for their contributions to the newsletter.