AGM Alts Weekly | 6.16.24

AGM Alts Weekly #56: Making private markets more public, every week.

👋 Hi, I’m Michael.

Welcome to AGM, the meeting place for private markets.

I’m excited to share my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in private markets so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Presented by

3i Members is a community of private investors sharing deals, insights, and contacts.

They pursue esoteric private market deals sourced exclusively from members without any economic interests in the deals presented, and prioritize uncorrelated, off the run, emerging strategies that generate asymmetric and high yielding return profiles.

3i deals also often come with more favorable terms and lower minimums than if an individual invested outside of the network.

Learn how 3i sources & diligences investment opportunities and how to get involved as a member here.

Good afternoon from London and Happy Father’s Day.

A new asset manager looks to be joining the fray. Bloomberg reported this week that Todd Boehly’s Eldridge Industries is planning to transform into a new firm that will combine at least six existing platforms and launch with $65B in assets, which could include the sale of a minority stake or pursuit of a public offering.

News of Boehly’s new venture highlights what’s becoming an increasingly popular trend among alternative asset managers: a focus on permanent capital.

Boehly’s success in asset management has very much been a result of his long-standing focus on leveraging the power of permanent capital. The crown jewel of Boehly’s expansive Eldridge Industries empire? A life insurance business based in Topeka, Kansas.

Security Benefit Life is the $52B retirement solutions provider that specializes in annuities. But it also does something much more for the Eldridge constellation. It affords Eldridge with the capital to purchase stakes in companies, alternative asset managers, and other properties, such as the LA Dodgers, Chelsea FC, and compelling assets.

Boehly recognized the power of permanent capital when he was at Guggenheim, where he built their credit business to over $60B and acquired Security Benefit Life on behalf of Guggenheim’s asset management business. When Boehly decided to leave Guggenheim to start his own business, Eldridge Industries, he didn’t want to leave without the crown jewel that could propel his business into various asset classes and business ventures. So, he purchased Security Benefit from Guggenheim.

Security Benefit Life is once again the centerpiece of what will be his newly formed asset manager, Eldridge. Security Benefit will be a large investor in the credit investments originated through Eldridge’s asset management arm, which will include real estate investment firm Cain International, private credit firm Maranon Capital, Panagram, which specializes in collateralized loan obligations and other structured products, and Stonebriar Commercial Finance.

Eldridge certainly isn’t the only alternative asset manager who can see the value in having permanent capital, which some call the “holy grail of private investing.”

The power of permanent capital

In their own ways, the publicly traded alternative asset managers have turned to permanent capital to fuel business and revenue growth.

Apollo chose to create a permanent capital structure through its merger with life insurer Athene. Athene affords Apollo the ability to generate revenue on spread-related earnings in addition to the fee-related earnings (FRE) from investments into Apollo funds.

Blackstone went down the path of creating open-ended permanent capital vehicles, becoming a behemoth in evergreen structures like BCRED (Blackstone’s credit fund) and BREIT (Blackstone’s real estate fund) which account for a meaningful portion of their fee-paying AUM.

But the leader of them all when it comes to permanent capital? Blue Owl.

Evercore ISI’s Senior MD and Senior Research Analyst Glenn Schorr recently shared an insightful analysis on the power of permanent capital in terms of its impact on FREs, margin, and valuation multiples.

The results of Schorr’s analysis were illuminating.

Schorr’s research highlights just how much of Blue Owl’s management fees come from permanent capital. It turns out that 100% of the earnings base is from fee-related earnings, and 92% of their management fees come from permanent capital. The result? Fee-paying capital that stays around for a long time and earns steady and consistent management fee revenues.

What does Blue Owl’s permanent capital structure tell us? That not all capital raised is necessarily created equal.

Not all permanent capital is created equal

Schorr posits that every $1B raised by Blue Owl is the equivalent of peers raising ~$3B. He finds that $1 of fundraising capital generates an average 3.2x more FRE and 2.7x FRE revenue due to the permanent nature of its capital, a higher fee rate, and a better FRE margin, which is a staggering ~60% FRE margin.

Blue Owl’s three areas of investment focus — Direct Lending, GP Stakes, and Real Estate (Triple Net Lease) — play well with their desire to focus on driving increased management fee revenues. Blue Owl Co-CEO Marc Lipschultz said as much on their Q1 2024 earnings call:

Said plainly, our earnings consist almost entirely of management fees, so we're not subject to the volatility and uncertainty of revenues tied to realized gains and capital markets activity. And having long-duration capital means very little leaves our system, providing us with a resilient asset base that grows faster than our peer group for the same number of dollars raised.

We think the market is starting to understand and appreciate the value of these stabilizing attributes and how they contribute to our premium growth profile. On a 12 month year-over-year basis, we grew FRE revenue and FRE by 24% and DE by 20%. We're humbled to be among the leaders in these metrics across our whole peer group, that includes very accomplished firms in our industry, and it's something we don't take lightly as we continue to plant the seeds for future growth at Blue Owl.

Permanent capital, permanent questions

Blue Owl’s success with permanent capital raises a number of interesting questions, both for the future of Blue Owl as well as its industry peers.

For Blue Owl, the question becomes how do they continue to expand their suite of alternatives strategy while staying true to their roots of permanent capital. In addition to growing AUM in their three core business lines, they will likely want to continue to find strategies that are long-duration capital. According to Schorr, initial focus areas will be expanding direct lending and triple net lease products in Europe, growing other debt verticals across healthcare lending, real estate debt, launching an alternative credit fund, and buying more CLOs, and scaling GP stakes into the middle market as they are with their new $2.5B fund in partnership with Lunate.

What’s next for Blue Owl? Perhaps their BOSE Strategic Equity (GP-led secondaries) launch and their acquisition of Kuvare Asset Management provide hints. Surely, the acquisition of Kuvare, which provides asset management services to the insurance industry, is on theme for their desire to continue focus on FREs.

But would they ever expand into private equity like their other peers? It’s possible that being a fast follower who’s seen a rapid ascent to the upper echelons of the alternative asset management industry helps them if their quest is to maintain a focus on management fees, as Lipschultz said.

By being later to the party, Blue Owl didn’t have to transform a closed-end fund business into a permanent capital business. And that may have helped them get to where they are today.

For other alternative asset managers, the strategic question becomes how do they continue to find ways to create vehicles that will enhance their ability to attract permanent capital? That will be easier said than done. Creating and managing BDCs and evergreen funds is far from trivial.

While evergreen structures are certainly attractive to GPs and LPs for a number of reasons, they are not easy to do well. Building a track record in the management and performance of evergreen funds will take time — and will require meaningful internal investment across the fund’s lifecycle, from pre-investment sourcing to fund and liquidity management to post-investment operations and reporting that a manager will have to execute.

As for Boehly’s Eldridge selling a stake in the business or taking it public? Tell me the percentage of permanent capital AUM and I’ll tell you how it might be valued.

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

AGM News of the Week

Articles we are reading

Secondaries in two

📝 Pro Take: StepStone Sees Opportunity in Venture Capital’s Liquidity Crunch | Marc Vartabedian, Wall Street Journal

💡Structural challenges in private markets are turning into an opportunity for secondaries funds. StepStone’s $3.3B raise for its new secondary venture fund, a figure higher than the entire amount raised last year for all such funds and over $700M greater than their $2.6B 2022 vehicle, highlights the growing opportunity for venture secondaries. StepStone is witnessing increased demand for its venture secondaries strategy as venture funds that are looking to show distributions to their LPs and LPs that are seeking liquidity are turning to secondary markets. “LPs are saying, ‘You haven’t sent us any money back in a few years. We’re set up to be that liquidity provider,” said StepStone’s Brian Borton. Secondaries funds like StepStone have a major advantage in buying stakes at attractive prices, largely due to the number of fund relationships they have and the company-level data that comes with it. Borton said that StepStone has the opportunity to find deals where fund stakes might be worth more than what LPs think. “This creates a tremendous arbitrage opportunity for us to capitalize on,” Borton said. The firm has bought stakes over the past year at 50% to 100% discounts, noting 90% of gains within its secondary venture fund portfolio come from valuation growth as opposed to discounted entry. Purchasing stakes in companies accounts for almost two-thirds of StepStone’s secondary venture business, with buying LP stakes comprising of the remaining third.

Secondary markets are being driven by liquidity issues that many early-stage investors are having, according to Kyle Stanford, the lead US VC Research Analyst at PitchBook. Secondary funds collectively raised $100M in the first quarter of 2024 after raising $3B in 2022 and $1.6B in 2023, according to PitchBook. “LPs need to get some money back to rebalance their portfolios,” Stanford said. “Now there’s a reason for someone like StepStone to raise $3.3 billion to invest solely in secondaries.”

📝 Silicon Valley’s Lightspeed shifts focus to secondary markets | Tabby Kinder, Financial Times

💡In a sign that both secondaries are an attractive part of the venture market and that the traditional model of venture capital is evolving, one of venture’s largest firms, Lightspeed Venture Partners, is shifting its focus to the secondary market. Lightspeed has focused on buying stakes in some of the industry’s largest startups in the secondary market at discounts. Lightspeed’s Chief Business Officer Michael Romano said: “Given market dislocation we were able to purchase a lot of very compelling new opportunities at significant discounts of 45 to 50 percent to the last fundraising round.” In February, they brought on former Goldman Sachs banker and Forge early employee Jack Fowler to lead their efforts in the secondaries space. They’ve already invested 20% of their $2.4B growth fund in secondary deals, first looking at companies in their own portfolio where they want to increase exposure. Lightspeed, which has over $25B AUM, has been amongst the most active venture capital firms in purchasing secondaries, spending over $580M on such deals in the past three years, including investments into Anduril, Rippling, and Stripe. Lightspeed’s activity in the secondary market is symptomatic of a growing trend of private companies staying private longer. “Absent an IPO or any M&A, venture capital firms need to get more creative to identify paths to liquidity,” Romano said. “Secondaries are a really important component of that.” Secondary trading volume has grown by more than 50% this year to the end of May compared to the same period last year, according to data provider Caplight. Some of the startup industry’s biggest companies were also the most traded names in the first quarter of 2024, according to Caplight. Anthropic, Discord, OpenAI, SpaceX, Epic Games, Databricks, and Rippling saw the most trading volume of their shares. Lightspeed also launched a “continuation fund” to sell around $1B of its existing stakes in startups in order to provide liquidity to investors. All of these moves are representative of a bigger trend amongst the largest venture firms. They are thinking about different ways to play across the continuum of primary and secondary investments, with many of the biggest firms becoming RIAs in recent years to invest in cryptocurrencies and to continue to hold large stakes in portfolio companies even after they have gone public. As many as 19 venture firms have become RIAs. Lightspeed could be next, as they are applying to become an RIA as well.

💸 AGM’s 2/20: Liquidity is top of mind for GPs and LPs alike. The structural dynamics in the industry have created a ripple effect in terms of how GPs and LPs are approaching the new game on the field. There’s certainly an opportunity for secondaries funds to find attractive discounts from LPs that need liquidity or from funds that have the pressure to return capital to investors as they look to raise a new fund. Advantage goes to the largest secondary and venture fund-of-funds platforms due to the depth and breadth of their data. Firms like StepStone benefit from their fund investments, which afford them with access to information on company metrics and valuations. This data should give them the ability to more accurately price and value secondary transactions at both fund and company levels.

According to a Wall Street Journal article by Jonathan Weil from last week, this structural advantage has reportedly paid off for fund managers. Weil finds that secondary funds like Hamilton Lane and StepStone have benefitted from buying fund secondary stakes at discounts from LPs. Weil highlights that these secondary firms bought stakes at significant discounts to what they then marked at a much higher value soon thereafter. That highlights both the opportunity and challenge in the secondary market. Buyers and sellers are operating with imperfect information, so firms with access to data and private fund and company valuations will have the biggest advantage. If there’s a seller willing to sell at a certain price, for whatever the reason, then that’s part of the game of secondaries.

The focus on secondaries also brings rise to a broader point about buying and selling assets in private markets — and one that relates to the comments earlier about permanent capital. One of the advantages of permanent capital vehicles is that investors are not forced sellers. That can be a benefit for GPs when they face calls from LPs to return capital to generate liquidity. A quote in a 2015 Financial Times article about permanent capital vehicles from Fortress’ Wes Edens highlights just how powerful permanent capital can be at the right time. Fortress was a forced seller of a portfolio of mobile phone towers in 2008 when the dotcom bust meant they had to unload the assets. “Had we owned that in a permanent capital vehicle we would still own it today.” I’m sure some sellers of their positions in companies or funds over the past few years are wishing they, too, had been able to hold those assets in permanent capital vehicles (note: some funds and investments, not all, as recent vintages also saw valuations that may be difficult to achieve going forward).

📝 Here’s How US Pension Giants Are Pursuing PE Club Deals | Marion Halftermeyer, Bloomberg

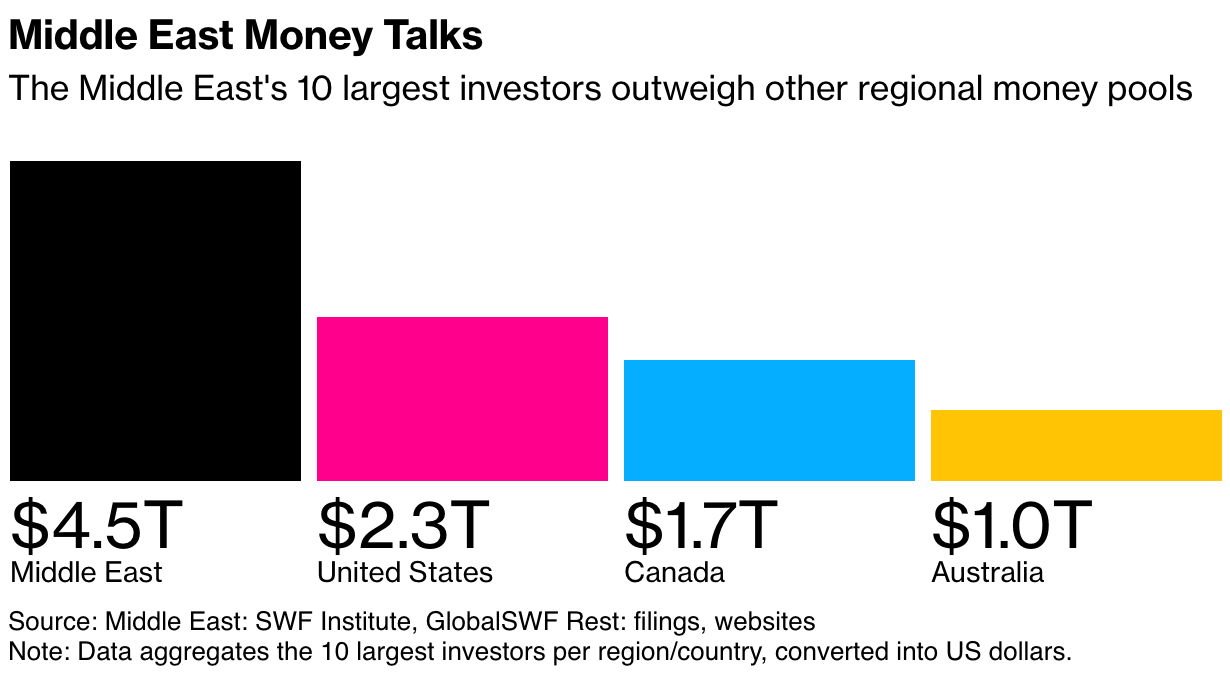

💡Bloomberg’s Marion Halftermeyer observes that some of the largest US pension funds are following the path of other sovereign wealth funds and pension funds by increasing their focus on co-investments to blend down overall fee loads in private equity. Many of the world’s largest institutional investors have shifted a focus to co-investments in order to gain increased exposure to private equity funds and deals at more cost-efficient fee levels. According to Halftermeyer, some US pension plans, such as CalSTRS and CalPERS, have lagged behind their international peers in co-investments. Middle Eastern sovereigns like Abu Dhabi Investment Authority and Saudi Arabia’s PIF have been active co-investors with many of the largest PE funds. Halftermeyer reports that KKR, EQT, and Brookfield all turned to Middle Eastern sovereigns to complete large deals last year. Apollo’s CEO Marc Rowan said earlier this year that the UAE is amongst the best places to find investors.

That now may change as US pension funds have been working to re-architect their decision-making processes. At times, these investment processes have included investment committees, consultants, and even politicians, making it more difficult for US pension funds to move swiftly to process co-investment opportunities. CalSTRS is now targeting to do a co-investment for every fund allocation it makes. In 2022, they saved $190M in fees, in part due to co-investing.

💸 AGM’s 2/20: Pensions and sovereigns have been pioneers in evolving the way that private markets investments are financed. They’ve increasingly become active in co-investments alongside private equity firms they partner with as LPs. This shift has occurred in part to blend down the overall fee load that they pay to GPs, enabling them to scale their commitments to private markets in a fee-efficient manner and generate excess returns. Long gone are the days of 2/20 in PE for many of the industry’s largest LPs. It appears that US pensions are looking to catch up to their institutional investor peers, which would be a boon for the large alternative asset managers. Deals are getting larger, particularly in areas like private equity, private credit, infrastructure, and real estate, meaning that large institutions will have an important role to play in financing the future of private markets. If they can move fast as co-investment partners, as Bloomberg’s article highlights, then they could benefit from first looks for co-investments from GPs. There’s plenty of capital to be consumed by investment opportunities, so it doesn’t appear that institutional investors and the wealth channel will compete for co-investments. Still, it’s interesting to think about whether or not the wealth channel will become more active co-investment partners for GPs as they increase their activity in private markets. Perhaps it will come down to the structure of the investment for the wealth channel. Some evergreen structures are focused on accessing direct investments from alternative asset managers alongside their closed-end vehicles. That could be another way for GPs to deploy capital more quickly and at a larger scale into opportunities.

📝 Banks, Private Credit Need to Team Up for Sake of New Economy | Eleanor Duncan and Francine Lacqua, Bloomberg

💡Enemies or frenemies? Bloomberg’s Eleanor Duncan and Francine Lacqua share comments from Deutsche Bank’s Co-Head of Capital Markets Hoby Buvat that investment banks and private credit firms need to work together to meet the massive capital expenditure requirements for the new economy, such as digitization and decarbonization. Buvat said, “As a bank, we are already working quite seriously on that. We are going to be working together with private credit providers to meet those needs for our core clients.” One of the big trends in private markets looming over banks is that private credit funds appear to be encroaching on their territory as they expand their tentacles into more areas of a bank’s balance sheet. Banks have responded in kind by building out direct lending operations of their own, or, as reported a few weeks ago with JP Morgan’s exploration of the acquisition of Monroe Capital, will look to acquire private credit capabilities to compete directly with their alternative asset manager counterparts. Buvat said it’s more likely that private credit firms and banks “converge.” “We compare private credit a lot to the syndicated capital markets,” said Buvat. “We are going to move away from that and just talk about how do we converge.” Buvat cites the capex requirements for the new economy in areas like digitization and decarbonization, which will require massive amounts of private and public capital to meet demand.

💸 AGM’s 2/20: It will be interesting to see how the battle between banks and alternative asset managers unfolds. It appears that everything is on the table for both types of firms. Banks are looking to build or buy private credit capabilities, with recent news of Goldman raising a $20B private credit fund and JP Morgan exploring an acquisition of $19B AUM private credit firm Monroe Capital highlighting that banks are looking to compete directly with their alternative asset management counterparts. But banks also face regulatory constraints that could make it difficult for them to go head-to-head with alternative asset managers. That could be one reason that banks may try to collaborate with private credit firms, particularly where meaningful capital is required for investments. The big trends appear to be the “3 D’s”: digitization, decarbonization, and deglobalization, which was highlighted in a recent interview between Bloomberg’s Francine Lacqua and Sixth Street’s Co-CIO Julian Salisbury. Salisbury, like many others, view these trends (digitization, decarbonization, and deglobalization) as major shifts that require large amounts of capital. That capital will likely have to come from collaboration between banks and private capital or collaboration between private capital funds, as we discussed last week with the $25B regional infrastructure partnership between KKR, GIP, and Indo-Pacific Group. But will banks and alternative asset managers look to work together? That’s the question going forward.

📝 Aflac Takes a Different Approach to GP Stakes — And It’s Not Buy and Hold | Alicia McElhaney, Institutional Investor

💡Institutional Investor’s Alicia McElhaney reports that Aflac Global Investments, which manages a $100B general account, has taken a different approach to GP stakes investments. Rather than hold their stakes in GPs they’ve invested into for the long term, Global CIO Brad Dyslin said that their approach has been “very opportunistic.” The insurer has already sold two of the five GP stake investments that it’s made. Just last month, Aflac announced its fifth deal, acquiring a 40% stake in Tree Line Capital Partners, a direct lending manager focused on the lower middle market that manages $2.7B AUM. McElhaney notes that the GP stakes space has grown in recent years, punctuated by Blue Owl Strategic Capital’s growth to almost $56B in AUM. GP stakes investments have tended to be investments that stakes firms or other investors have preferred to hold for the long term due to the compounding nature of the investment. According to Dyslin, Aflac has already sold its stakes in NXT Capital, its first GP stakes investment, and Varagon Partners. Aflac had invested $50M into NXT, which managed a $500M portfolio on its behalf in 2017. But NXT was acquired by Orix in 2018, resulting in a liquidity event for Aflac. Varagon sold a minority stake to Aflac in 2020, but when Man Group decided to acquire a majority controlling interest in the firm in 2023, Aflac ended up with another exit in their GP stakes portfolio. Dyslin called the exits “opportunistic.” He said, “The portfolio has done well for us. We were content to continue to support the platform by leaving our mandate there, but we got attractive terms on the equity.”

💸 AGM’s 2/20: What’s interesting about Aflac’s approach to GP stakes is not that they’ve decided against a buy-and-hold strategy with this investment thesis but that they’ve been able to generate liquidity from their GP stakes investments. One of the questions that many GP stakes funds face is the question of liquidity. Part of what makes a stakes investment attractive is its compounding features that come from holding it for the long-term. That’s led many stakes firms to structure their funds as virtually permanent capital vehicles. Firms are thinking about different ways to offer liquidity features to investors in the absence of exits, but that question still remains top of mind for LPs. The middle market, where Aflac has made the majority of its GP stakes investments, does represent more ample opportunity for exits for stakes investors due to the likely consolidation occurring in alternative asset management. Aflac may have a different approach to its GP stakes investing than others, but the most important takeaway of all is that consolidation might be on the menu in the middle market, which would bode well for stakes investors who are making bets in the middle market.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know, and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Blackstone (Alternative asset manager) - Private Wealth Solutions - Educational Content Strategist, Vice President. Click here to learn more.

🔍 Apollo (Alternative asset manager) - Distribution & Wealth Services Associate. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - US Asset Management Channel, Business Development - Managing Director. Click here to learn more.

🔍 AltExchange (Alternative asset management data) - Fund Accountant. Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - VP / Principal, Private Wealth Market Leader. Click here to learn more.

🔍 73 Strings (Private markets data and valuation software) - Credit Portfolio Valuation Senior Manager. Click hear to learn more.

🔍 LemonEdge (Fund accounting) - Implementation Manager. Click here to learn more.

🔍 PitchBook (Private markets media, data, analytics) - Reporter, Private Equity (London). Click here to learn more.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

🎙 Hear Ritholtz Wealth Management’s Managing Partner Michael Batnick share views on how wealth managers are navigating private markets. Listen here.

🎙 Hear HgT’s Chairman of the Board Jim Strang provide us with a masterclass in private markets. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, and I welcome special guest Robert Picard, Managing Director, Head of Alternative Investments at Hightower Advisors, as we take the pulse of private markets on the 10th episode of our monthly show, the Monthly Alts Pulse. We discuss the operational challenges and solutions in private markets. Watch here.

📝 Read about the evolution of GP stakes, why alternative asset management business models are better than SaaS, and our partnership with Todd Owens and David Ballard at Cantilever, a mid-market GP stakes firm anchored by BTG Pactual. Read here.

🎙 Hear 3i Members Co-Founder Mark Gerson share how to build engaged investing communities. Listen here.

🎙 Hear Yieldstreet Founder & CEO Michael Weisz discuss how to deliver private markets investment opportunities directly to consumers. Listen here.

🎥 Watch internet pioneer Steve Case, Chairman & CEO of Revolution and Co-Founder of America Online, share lessons learned from building the first internet company to go public and an investment firm built for the Third Wave of the internet. Watch & listen here.

🎙 Hear Carlyle Operating Partner & Net Health CEO Ron Books discuss lessons learned from growing ECi Software Solutions to $500M revenue and $200M EBITDA and working with private equity. Listen here.

🎙 Hear Blue Owl’s Global Private Wealth President & CEO Sean Connor share insights and lessons learned from working with the wealth channel. Listen here.

🎙 Hear Blackstone CTO John Stecher discuss how technology is transforming private markets. Listen here.

🎙 Hear how Chris Long, Chairman, CEO, and Co-Founder of Palmer Square Capital Management has built a $29B credit investment firm and a winning NWSL soccer franchise, the KC Current. Listen here.

🎙 Hear stories from building market-defining companies Blackstone, Airbnb, and private markets from Laurence Tosi, former CFO of Blackstone and Airbnb and Managing Partner & Founder of $7.6B investment firm WestCap. Listen here.

🎥 Watch me talk with David Weisburd of 10X Capital Podcast about why the wealth channel is becoming a centerpiece of the LP universe, drawing on my experience helping to build the wealth channel at iCapital as an early, pre-product employee and our investments at Broadhaven Ventures in private markets technology. Watch here.

🎥 Watch the replay of the fireside chat at Future Proof decoding the rise of alts with some of the most influential players in private markets: Stephanie Drescher, Partner, Chief Client & Product Development Officer, and member of the Leadership Team at Apollo, and Shannon Saccocia, the CIO at Neuberger Berman Private Wealth. Watch here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear wealth management industry titan Haig Ariyan, CEO of Arax Investment Partners, share his thoughts on the private equity opportunity in wealth management and why the intersection of wealth and alts is one of the biggest trends in private markets. Listen here.

📝 Read how 73 Strings CEO & Co-Founder Yann Magnan and team are leveraging AI to build a modern and holistic monitoring and valuation platform for private markets in The AGM Q&A. Read here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, discusses how they approach alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Michael Rutter and Nick Owens for their contributions to the newsletter.