AGM Alts Weekly | 6.25.23

AGM Alts Weekly #7: Making private markets more public, every week.

👋 Hi, I’m Michael and welcome to my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in alts so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Hi from Washington, D.C. I was in NYC last week, where I caught up with some of the players in the alts space.

The retailization of alts is in full force. Alt Goes Mainstream represents two things: 1) that the 60/40 portfolio is no longer, so the mainstreaming of alts means private market investments becoming a larger portion of an investor’s portfolio and a mainstay in asset allocation strategies, and 2) that the mainstreaming of alts also results in the downstreaming of alts, which enables investors beyond the institutional investor and ultra wealthy to participate in private markets. This downstreaming first occurs with UHNWIs, then continues down the curve to accredited investors, and ultimately to non-accredited investors, all at successively lower minimum investment entry points.

Data suggests that expanding access to all corners of the wealth channel will drive AUM growth in private markets. A 2022 BCG & iCapital report highlights that HNWI allocations to private equity will grow at almost 19% annually, resulting in HNWIs accounting for over 10% of all capital raised by private equity funds at over $1.2T.

Many of the big platforms — whether technology providers like iCapital, large asset managers like Blackstone, Apollo, KKR, Carlyle, Fidelity, and others, and private banks — all have the concept of downstreaming of alts top of mind.

Recent announcements, like the expansion of iCapital’s iDirect Private Markets Fund for accredited investors to include Warburg Pincus and Vista Equity Partners and BMO’s launch of two access funds with Partners Group and Georgian Partners, respectively, to Canadian accredited investors, highlight the focus on the accredited investor.

This recent news of structuring products for the accredited investor represents a bigger theme and trend: large alternative asset managers are looking to create ways that enable accredited investors to access their funds. Historically, the challenge for these funds has been one of infrastructure. It was difficult for them to accept a large number of investors at low minimums due to the administrative, compliance, and reporting burdens. Thanks to the advent of infrastructure solutions in this space, private banks and funds are now able to accept these investor commitments and have a dedicated effort working with the high net worth channel either on their own or in partnership with technology platforms.

Now the questions shift to the investor side — will a different product structure lead to better returns, net of fees?

The $1T opportunity is here — and everyone in the space is well-aware of it. The question now is how will it impact the end investor.

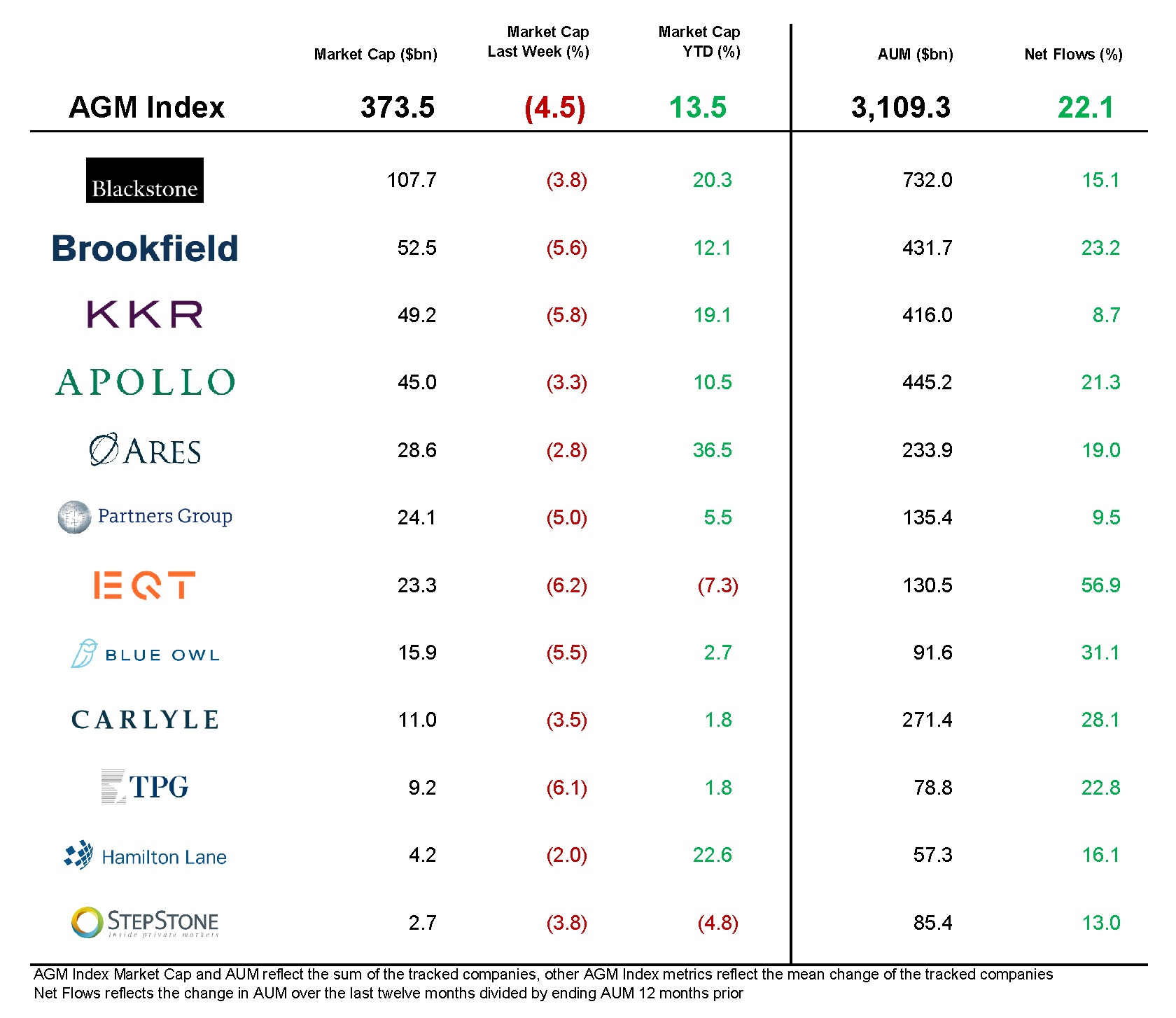

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

AGM News of the Week

Articles we are reading

📝 Pejman Nozad on ripening Pear VC into a top seed-focused firm | Marina Temkin, PitchBook

💡Pitchbook’s Marina Temkin interviews Pejman Nozad, the co-founder of Pear VC, on the heels of the close of their $432M fourth fund. Pejman and his co-founder, Mar Hershenson, have built a strong brand at pre-seed and seed stage, investing early in the likes of DoorDash, Gusto, Guardant Health, and others. Despite a difficult fundraising environment for VCs currently in market raising funds, Pear was able to almost 3x the size of their fund, besting their previous $160M fund closed in 2019. Pejman discusses the current state of VC fundraising, why LPs are interested in dedicated pre-seed and seed strategies, and why they’ve expanded the size of their fund (Congrats Pejman and Mar on your continued success at Pear, very impressive to see the firm you’ve built. For those who haven’t yet heard about Pejman’s story of how he became a VC, this blog post by him back in 2016 about how he’s “tech’s most unlikely venture capitalist” is worth a read).

AGM’s 2/20: Pejman’s interview with Pitchbook is interesting for a few reasons. It sheds light on some of the trends in VC that are worth noting. 1) Pejman said that Pear increased their fund size in part because they are writing bigger checks at seed stage. This comment coincides with the fact that many of the large, multi-stage funds are also investing at Seed and, due to their fund sizes, they are also writing larger checks at Seed stages to make it meaningful for their fund size. Despite a slowdown in funding in 2023, median and average round sizes at Seed rounds in the US in Q1 2023 are still significantly higher than they were even just a few years ago. Crunchbase data shows that the average Seed round size in the US in Q1 2023 was $3.6M. Compare this to 2014, where the average Seed round size was $0.8M or 2018, where the average Seed round size was $1.0M. What’s the punchline? Seed funds may need to increase their fund sizes to keep up with the rising size of Seed rounds. But it’s worth noting that Seed funds should also be wary of growing their fund size too much, as fund size is your strategy and larger fund sizes can make it harder to drive higher returns. 2) Pejman said that some of the largest institutional LPs are interested in having a dedicated pre-seed and seed strategy. This is also an important trend to note — specialist managers, whether by stage or by sector, are becoming more attractive to LPs. I’d hypothesize that specialist managers, particularly at early-stage, are also more attractive to founders because the managers are able to build a well-defined brand that resonates with founders, which leads to better dealflow for the manager, potentially leading to outperformance.

📝 Partners Group has become one of the first global private markets firms to implement the large language model GPT-4 for use by a global employee base | Partners Group, LinkedIn

💡Partners Group is continuing it’s tradition of innovation. The firm has launched an evergreen program, developed products for all three of the largest Defined Contribution pension markets, and tokenized part of a flagship private equity fund. Now, the firm has become one of the first in the industry to implement the large language model GPT-4 for use by a global employee base. Through this latest innovation, the firm aims to increase efficiency by allowing GPT-4 to find attractive sub-sectors for investment, identify competitors to its portfolio companies, and support RFP writing. This language model also increases potential use cases for teams across the platform by offering a ring-fence that guarantees data privacy and confidentiality.

AGM’s 2/20: We are in the early days of just how much AI can impact private markets. Partners Group, a $135B AUM private markets firm, implementing LLM GPT-4 for use to drive efficiency internally and leverage the technology to better analyze internal data is foreshadowing of more to come. AI can certainly help fund managers do diligence and be more efficient with analysis, particularly when it comes to taking large data sets and making sense of them, with areas like market sizing, competitive analysis, portfolio monitoring, and valuations. It should only be a matter of time before the largest funds start to implement AI for internal operations and sourcing / diligence functions and also before a number of newer funds crop up planning to use AI as a core part of their investment operations.

📝 VC giant Andreessen Horowitz expands into wealth management | Dan Primack, Axios

💡Venture capital firm Andreessen Horowitz is expanding into the wealth management space with the launch of the "a16z Perennial Venture Capital Fund," according to a recent SEC filing. The new fund, similar to Sequoia Capital's "Heritage" effort, aims to provide diversified investment opportunities to high-net-worth individuals, both within and outside the tech ecosystem. It will offer exposure to various asset classes, including real assets, bonds, and startup equity, catering to different investor profiles. This move signals Andreessen Horowitz's foray into wealth management and its focus on offering a broader range of investment options to its clients.

AGM’s 2/20: Andreessen’s move into wealth management signals a few things for the future of venture capital as a business. One, it shows that they are building a multi-strategy, multi-product investment platform. Although this is slightly different than the evolution of private equity platforms like Blackstone, Apollo, KKR, and Carlyle, which have built out multiple business units as they’ve grown, it has similar features in the sense that they are expanding beyond their initial business — venture capital funds — into other asset and wealth management businesses. This speaks to a broader trend for the large VC funds — they are evolving into platforms much like their private equity counterparts have done over the years. Adding a wealth management unit is also a fantastic way to distribute their private fund strategies to a broader group of LPs. HNW investors who invest in the Perennial Fund will likely have access to a16z fund products in addition to other strategies that the Perennial Fund offers across real assets and fixed income in addition to private funds. This move also represents a way to keep their founders in the a16z ecosystem, as founders of a16z portfolio companies may choose to manage their wealth with the Perennial Fund. I’d anticipate that we see more of the large platforms, as Sequoia has done with Sequoia Heritage, manage partner capital and capital from others in their ecosystem since it can further expand their wallet share with their founders and LPs.

📝 Private Credit Fuels Asset Management Deals | Michael Thrasher, Institutional Investor

💡Asset management M&A activity remains robust, in large part because firms are looking to add private credit firms to their offering. Buyers view private credit as attractive in the current rate environment, as rising interest rates make private credit attractive. The fallout from the SVB and other regional bank failures means that banks are pulling back from lending and the current environment makes this a market where lenders, rather than borrowers, can drive attractive terms. Asset managers view the prospective of diversifying their businesses as more attractive to investors because they can handle market cycles and have more consistent revenue.

AGM’s 2/20: Private credit appears to be en vogue. And for good reason. Private credit should be attractive in the current environment, both from an investment perspective given the current industry dynamics and from a capital raising perspective. Private credit appears to be one of the more attractive strategies within private markets for fundraising, particularly from the wealth channel based on conversations I’ve had with capital raising platforms and wealth managers. Now is a good time for a niche private credit manager who has built a strong business in recent years to explore opportunities with a larger platform that can enhance their distribution and grow their AUM. BlackRock’s acquisition of Kreos and TPG’s acquisition of Angelo Gordon represent two recent cases of firms looking to diversify their offerings and move into private credit, and I anticipate that this is only the beginning of continued M&A in this space.

📝 Shares of Startups Are Turning Dirt Cheap, Attracting Venture Funds | Hema Parmar, Linly Lin, Sarah McBride, Bloomberg

💡The late stage startup market may be unthawing. The previously glacial secondary market may finally be starting to see narrowing bid-ask spreads as investors are beginning to buy up discounted shares of startups. Bloomberg reports that VCs and hedge funds see a buying opportunity, particularly with existing portfolio companies. Andreessen Horowitz is reportedly increasingly buying shares on the secondary market, as are Bain Capital Ventures, Bessemer Venture Partners, Kleiner Perkins, and Accel, amongst others. In Q1 2023, VCs and growth equity funds have represented almost 80% of the purchase volume of secondary market shares. Hedge funds, like Tiger Global and Coatue, are also actively snapping up shares. EquityZen Founder Phil Haslett shares another interesting observation about the current state of the secondary market: institutions overseeing billions of dollars in AUM are even open to buying small stakes ($2M+ deal sizes) so they can get exposure to companies at discounts. This news comes at a time when institutional LPs and hedge funds are looking to sell portfolios or specific private company holdings. It’s been reported that Tiger Global and Third Point are looking to sell stakes in private companies and CPPIB is said to be mulling a sale of $3B of private assets.

AGM’s 2/20: It appears that there may be movement in secondary markets. Just weeks ago, we heard news of hedge funds like Tiger looking to offload private company stakes. Now, we hear news of VCs being active buyers in secondary markets. The secondary market was at a standstill, with bid-ask spreads too wide for buyers and sellers to transact. Perhaps there’s now enough clarity in the markets, or steep enough discounts on high-quality companies, for buyers to get comfortable with prices and for sellers to be comfortable selling in a quest for liquidity. The big question about an unthawing in the secondary market: does this activity provide foreshadowing that investors anticipate the IPO window to open towards the latter half of 2023 and into 2024?

📝 Asset Management’s Winners and Losers After the Rate-Hike Pause | Michael Thrasher, Institutional Investor

💡The Federal Reserve's decision to pause interest rate hikes is expected to create winners and losers in the asset management industry. Investment firms focused on fixed income such as Apollo Global Management, Ares Management, and Blue Owl have seen their shares rise due to higher interest rates in the past year. A prolonged high-rate period could amplify these effects. Smaller alternative managers benefitting from the same market circumstances, particularly private credit managers, are coming into focus as attractive acquisition targets.

AGM’s 2/20: The benefits of being a multi-strategy alternative asset manager are becoming clear, perhaps even moreso in an environment with rising interest rates. Publicly traded alternative asset managers who have private credit strategies have seen their stock prices rise over the past 12 months. Apollo’s shares are up 54% over the past 12 months — and higher interest rates should be a boon for their business, which has a big focus on credit. Their insurance business, Athene, will also enable them to benefit from higher interest rates as they support spread related earnings. Apollo’s competitors, Ares and Blue Owl, have also seen strong share price performance, in large part because the majority of their assets within their credit businesses are floating rate. Interest in private credit is also spurring consolidation. We’ve seen a number of recent acquisitions in this space — BlackRock buying Kreos and TPG buying Angelo Gordon — and we should expect to continue to see private credit managers be an interesting acquisition target for managers who want to expand their strategies. Private credit is not only expected to perform well in the current environment, but is also expected to be an attractive strategy for allocators, which will also drive management fee revenues for alternative asset managers.

📝 US investors ditch European VC for domestic deals | Leah Hodgson, Pitchbook

💡US investors appear to be scaling back on European venture investments as they refocus their attention on domestic opportunities. At the beginning of the year, it was thought that European VC deals with US participation would be strong. Pitchbook analysts predicted that US VC participation in European deals would represent over 1/4th of 2023 deal count, which would have been the highest figure yet. But, as numbers stand currently, US presence in European deals is likely to come in lower. As of May 31, US investors took part in 692 deals worth €10.3 billion ($11.3 billion), according to PitchBook's 2023 European Private Capital Outlook: H1 Follow-Up. This represents 19% of overall deal count, a drop from 22% in 2022. The prevailing thought was that comparatively lower valuations and portfolio diversification would drive US participation in European deals. However, a number of factors have led US VCs to retrench to domestic markets and focus on their core.

AGM’s 2/20: European VC has many promising trends in its favor, as I and podcast guests on Alt Goes Mainstream have discussed here before. But it’s worth taking note of this Pitchbook data to recognize some current trends in VC. VCs are turning their focus to core markets rather than looking further afield for deals. While Europe is certainly a promising place for VCs to invest, the geopolitical threats posed by the Russia / Ukraine conflict, which reached new heights this weekend, still loom large and are very real. Furthermore, GBP and EUR have strengthened versus the dollar, which make investing in Europe incrementally less attractive for dollar-denominated investors. I would expect interest in Europe to continue to rise over the long-term, as evidenced by US VC funds continuing to spend time on the ground in Europe, but the short-term deal activity may not be as promising as expected.

📝 BMO Launches Fund with Partners Group to Provide Simplified Access to Private Markets | BMO

💡BMO Global Asset Management has launched the BMO Partners Group Private Markets Fund, in collaboration with Partners Group, to provide simplified access to private markets for Canadian accredited investors. The fund offers a globally diversified portfolio encompassing private equity, private credit, private real estate and private infrastructure, all in one vehicle. This initiative expands on BMO GAM's alternative investment offerings, including the recently launched BMO Georgian Alignment II Access Fund LP, which focuses on privately-held North American software companies. Partners Group brings its expertise as a leading global private markets firm to deliver bespoke solutions for institutional investors, sovereign wealth funds, family offices, and private individuals worldwide. The collaboration aims to simplify private market investing and offer long-term compounding returns, leveraging Partners Group's global platform and investment approach.

AGM’s 2/20: The news of BMO’s new fund in partnership with Partners Group to provide access to private markets funds for Canadian accredited investors represents a bigger theme and trend: large alternative asset managers are looking to create ways that enable accredited investors to access their funds. Historically, the challenge for these funds has been one of infrastructure. It was difficult for them to accept a large number of investors at low minimums due to the administrative, compliance, and reporting burden. Thanks to the advent of infrastructure solutions in this space, private banks and funds are now able to accept these investor commitments and have a dedicated effort working with the high net worth channel. An interesting feature of the BMO Access Funds is that they enable the ability for investors to do a single commitment up front rather than multiple capital calls. Private investments can be a challenge due to liquidity planning — investors generally need to plan for multiple capital calls over the course of the investment period, some of which may be difficult to predict, particularly if it’s newer for them or if they lack the tools to do so. The announcement from BMO comes weeks after iCapital announced their iDirect Private Markets Fund, adding Vista Equity Partners and Warburg Pincus to a multi-manager vehicle that also includes KKR. With $25,000 investment minimums and no capital calls, the iDirect Private Markets Fund is yet another signal that the infrastructure is there to enable many of the larger funds to continue the mainstreaming of alts by moving downstream to accredited investors.

Reports we are reading

📝 KKR Mid-Year Update 2023: Still Keeping It Simple | Henry H. McVey, KKR

💡KKR’s mid-year update posits that investors are too conservatively positioned to take advantage of the current vintage. They believe that the bottom is in for the S&P 500 and, due to a number of factors, believe that “recent dislocations have created some stand-out investment opportunities that traditional 60/40 investors might be overlooking.” Their view is that now is a “really compelling time to be a lender on a global basis.” They also continue to pound the table on the benefits of collateral-based cash flows in portfolios, particularly Infrastructure, Asset-Based Finance, and certain Real Estate projects that are directly linked to positive nominal GDP growth. Furthermore, they are quite focused on the energy transition to green power generation as an investment theme: “Just consider that a recent analysis from Financial Times found green power generation capacity globally may need to increase by roughly 800% by 2050 to meet current climate goals (Exhibit 19). This undertaking will need to span multiple decades and trillions of dollars in capex, including significant investment in all areas of power generation, transmission, and distribution.”

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Goodwater Capital ($4B AUM consumer tech VC) - Director, Seed Investments. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - West, Regional Director, Vice President / Senior Vice President. Click here to learn more.

🔍 Allocate (VC infrastructure investment platform) - Managing Director, Alternatives (Sales). Click here to learn more.

🔍 Republic (Multi-strategy alternative investment platform) - Chief Technology Officer. Click here to learn more.

🔍 73Strings (Valuation and portfolio monitoring for alternatives funds) - Analyst, Portfolio Monitoring. Click here to learn more.

The latest on Alt Goes Mainstream

Recent episodes and blog posts on Alt Goes Mainstream:

🎙 Hear Avlok Kohli, AngelList’s CEO, talk about how they are building the company of companies that is powering private markets. Listen here.

🎙 Hear John Avery, VP Digital Assets, Tokenization, Web3 at fintech giant FIS talk about how evolutionary changes can lead to revolutionary changes in private markets. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, and I take the pulse of private markets on the first episode of our monthly show, the Monthly Alts Pulse. Watch here.

🎙 Hear Seyonne Kang, Partner and member of the private equity team at $134B AUM StepStone, discuss how the VC industry is dealing with today’s venture market. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear 44th Vice President of the United States and Chairman of Cerberus Global Investments Dan Quayle share his insights on geopolitics and investing. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Riley Robinette for his contribution to the newsletter.