AGM Alts Weekly | 7.02.23

AGM Alts Weekly #8: Making private markets more public, every week.

👋 Hi, I’m Michael and welcome to my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in alts so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Hi from New York City, where I’m here to attend the National Women’s Soccer League’s (NWSL) Angel City FC’s match today versus NJ/NY Gotham FC.

Professional athletes embody a form of excellence. They have done great work, utilizing discipline and focus to do little things (drills and practice that sharpen their craft) that turn into big things (becoming a professional athlete, winning a championship) that make them outliers. Their work and achievements are a result of compounding little things over time. When athletes reference their success, they often cite their focus as a major reason why. Success comes from planning — and their achievements are usually ones that can be specific and described in advance.

But not all success can be achieved with planning. So how can people do great work? Paul Graham’s essay, How To Do Great Work, is an illuminating inquiry into the contours and nuances of this topic.

Entrepreneurship, and by extension, investing, is often the exploration of people’s desire to solve problems.

How does an essay about great work — much of which centralizes around unpacking curiosity and how to find, engineer, harness, and expand the frontiers of curiosity — relate to private markets?

Well, in a number of ways, in fact. A passage from Paul’s essay stands out:

Great work happens by focusing consistently on something you’re genuinely interested in. When you pause to take stock, you’re surprised how far you’ve come.

The reason we’re surprised is that we underestimate the cumulative effect of work. Writing a page a day doesn’t sound like much, but if you do it every day you’ll write a book a year. That’s the key: consistency. People who do great things don’t get a lot done every day. They get something done, rather than nothing.

If you do work that compounds, you’ll get exponential growth. Most people who do this do it unconsciously, but it’s worth stopping to think about. Learning, for example is an instance of this phenomenon: the more you learn about something, the easier it is to learn more. Growing an audience is another: the more fans you have, the more new fans they’ll bring you.

The trouble with exponential growth is that the curve feels flat in the beginning. It isn’t; it’s still a wonderful exponential curve. But we can’t grasp that intuitively, so we underrate exponential growth in its early stages.

Something that grows exponentially can become so valuable that it’s worth making an extraordinary effort to get it started. But since we underrate exponential growth early on, this too is mostly done unconsciously: people push through the initial, unrewarding phase of learning something new because they know from experience that learning new things always takes an initial push, or they growth their audience one fan at a time because they have nothing better to do. If people consciously realized they could invest in exponential growth, many more would do it.

Consistency compounds. And the best investments and companies are often those that have compounding potential and qualities.

Investing is in a sense an exercise in the exploration of the compounding impact of curiosity. Investors are learning about founders, they are learning about markets, they are learning about trends, they are learning about psychology and sentiment. The more they learn, the more information they have to make a decision. Information compounds to form a thesis. A thesis creates a world view that can shape an investment. And that investment, when given the freedom to last over a period of time thanks to the investor’s thesis and patience, can result in long-term compounding returns. News of Apple becoming the first company in history to hit $3 trillion in market value is case in point.

We often underestimate long-term potential and overestimate short-term gain and risk. This applies to learning as well as investing.

Private equity and venture capital are exercises in patience, focus, and the ability to invest in work that compounds, which can lead to exponential growth in the long run. And, in some respects, features of private markets, like illiquidity, can be a feature rather than a bug. Of course, liquidity is important in investing and gives investors optionality, particularly important when markets are uncertain. Illiquidity requires patience and the ability to stomach volatility in prices, as well as the opportunity cost of not allocating that capital elsewhere. But over the long-term, illiquidity can result in compounding returns if investors have invested in the right companies that have many of the same features that Paul describes in his essay about people who do great work.

While it’s incredibly hard to maintain dominance as a company, there’s reason to believe private markets will have companies that have those features. Companies like Blackstone embody the concept of how compounding consistency can lead to exponential growth. Blackstone has consistently grown its AUM, a proxy for revenues, thanks to their revenue model of management fees, through growth of its core business (private equity) and the curiosity to expand into other asset classes (private credit, real estate, hedge funds) and customer types (HNW channel). There are many other examples like Blackstone when it comes to asset management businesses, and I’d expect many of these firms to exhibit that compounding consistency as private markets continues to grow. Alts innovators like iCapital, Carta, AngelList, to name a few, also embody this combination of compounding consistency with a curiosity to explore the edges of the industry, knowing well that in the long-run those projects of exploration could shape the development of private markets.

My bet is on companies that have the desire and ability to push the frontiers of curiosity and explore ways of evolving, while also maintaining consistency and focus in doing work that compounds every day. The days may seem long, but the years will be short.

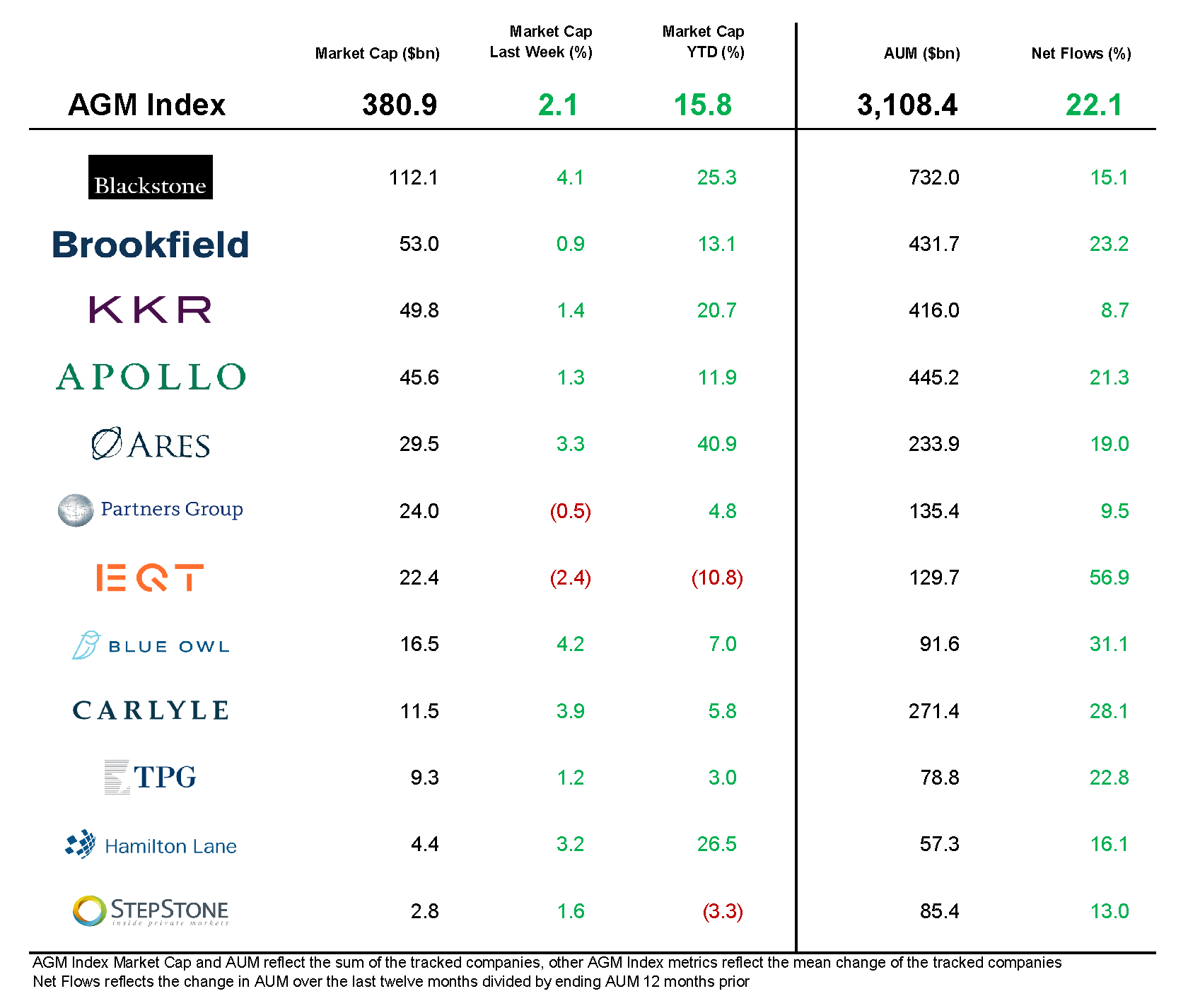

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

AGM News of the Week

Articles we are reading

📝 How PE is paving the way for private wealth | David Stevenson, PitchBook

💡Private equity has historically been the domain of institutional investors, but fund managers see the growth opportunity in high-net-worth investors. Allocations to private equity funds has seen a marked increase in the past few years — and it’s a trend that is expected to continue. By 2025, high-net-worth individuals will have 2.4x more assets in PE funds than they did in 2020, according to a report by Boston Consulting Group. This represents $1.2 trillion globally. Goldman’s Q1 2023 survey found that family offices are planning to increase their exposure to risk assets, including PE, this year. Respondents had an average 26% asset allocation to PE, second only to 28% in public equities. Goldman Sachs also found that 41% were planning to increase their exposure to PE over the course of this year. Private banks are driving meaningful growth in the increase in assets flowing into private equity funds, as many of the big PE platforms have built relationships with the private bank channel. Catering offerings to the HNW channel doesn’t come without its challenges. Liquidity is proving to be one of the biggest barriers for PE investors, and even institutions sometimes balk at the notion of tying up their assets for the 10-year lifecycle of a typical PE fund. In May, two firms launched semi-liquid funds to give private wealth clients access to PE strategies: EQT with EQT Nexus and Apollo Global Management with Apollo Private Markets SICAV, a platform of two funds. But it’s a problem worth solving for the asset managers: keeping investors' money tied up is one draw to PE. "This asset class offers potentially strong growth for the coming decade and more. The fee streams are often very sticky and long duration," said Alistair Watson, Abrdn's head of strategy innovation for PE.

AGM’s 2/20: Inflows and interest in private equity funds from the wealth channel is clearly on the rise. The above AGM Index provides a window into this trend. Many of the large, publicly traded asset managers, including all in the above Index, have seen inflows increase this year. Investors’ appeal of accessing possible strong returns are a part of the story — the outperformance of PE may explain the projected growth in investment. PE has outperformed major public market indices by well over 300 basis points over 5-, 15- and 20-year periods, according to the Cambridge Associates US Private Equity Index as of Jan. 30. Investors seem to have a continued belief that private equity should be part of their portfolio, and the wealth channel now has access to private equity products that were previously out of reach. The big questions going forward will be around product structuring and how fees impact returns. Are the net of fees returns worth investors’ allocating to private equity instead of elsewhere?

📝 CVC secures €25bn for industry's biggest-ever buyout fund | Madeleine Farman, Private Equity International

💡CVC Capital Partners, the third-largest private equity firm in Europe, is on track to raise the industry’s largest private equity fund in history. Sources familiar with the fundraise reveal that CVC Capital Partners IX has secured at least €25 billion ($26.8B USD) in commitments, surpassing Blackstone's previous record of $26.2 billion, allowing for currency conversions. The fund, launched last year, may even exceed its €25 billion target. This achievement is notable in the current market climate, where fundraising has proved to be a formidable challenge for many. CVC's success in accumulating commitments aligns with its plans to go public, with Amsterdam or London potentially hosting its initial public offering. Other firms in the industry have tempered expectations regarding their fundraising efforts.

AGM’s 2/20: It would be quite the impressive feat for CVC to close on the largest private equity fund in a fundraising environment that has been challenging for many funds. CVC’s successful fundraise could signal a few things: (1) that the big PE platforms are proving popular with investors, both with institutions who need to invest large sums of capital and can’t concentrate large pools of capital into smaller managers from a risk management perspective and with the HNW channel, as they look to allocate to brand-name managers, (2) that LPs view the current vintage for private equity as an attractive investment opportunity, (3) that size matters and should drive larger funds’ ability to win deals in private equity. It’s worth nothing that while fundraising success is an important driver of building an asset management business and creating enterprise value, returns are another thing. This point is less a comment on CVC, who has had a track record of strong performance, but more a comment that the adage, “your fund size is your strategy,” usually rings true in private markets. The bigger the fund size, the more challenging it can be to drive meaningful returns.

📝 UK’s biggest startup investor is seeing more demand than ever | Kabir Agarwal, Sifted

💡The biggest investor in the UK’s startup ecosystem is seeing a surge in investment demand from VCs and companies alike as other funding sources dry up. British Patient Capital’s (BPC) CEO Catherine Lewis has said they’ve seen an increase in “knocks on the door” in the past 12 months. This is amidst a fundraising slowdown in the VC industry in Europe. In the first half of 2023, VCs in Europe only managed to raise €7B, according to Pitchbook data. That pales in comparison to 2021 and 2022, when they managed to bag close to €28B each full year. The British Business Bank, the UK's government-run investor, set up BPC in 2018 with the express mandate of “unlocking billions” for high-growth innovative companies. It's now the most significant domestic player in the UK’s startup investment landscape with a budget of over £3B and committed investments totaling £1.6B. To date, BPC has backed 40 fund managers across 70 funds. While BPC is playing a big role in backing the UK’s startup ecosystem, Lewis would like to see more institutional participation in private markets from pension funds. La Torre agrees that it would be “enormously helpful” if there was bigger participation from pension funds. “I say that not just because it would be a nice thing to do. But if you look at the opportunity set and what is actually invested, there's a big gap,” she says. More pension fund participation would follow the precedent of pension funds in places like Canada, Australia, and the Nordics, where pensions are very active in private markets, investing heavily into both companies and funds.

AGM’s 2/20: Comments from BPC’s CEO Catherine Lewis align with the growing interest and activity coming out of Europe, and particularly the UK’s startup ecosystem. Just a few weeks ago a16z announced they would be opening up an office in London — and this follows increased interest from many US VC funds in the UK startup ecosystem. While deal volume and fundraising targets may fall in the short-term due to some of the current headwinds faced by private markets, Europe and the UK are quite interesting places to invest right now, as has been covered on Alt Goes Mainstream. The public sector has long been a supporter of the European and UK startup ecosystems, with the EIF and British Business Bank featuring prominently as backers of both companies and funds. This is a net positive for the ecosystem, as capital greases the wheels for more capital to flow into a market. I agree with the comments from Lewis about more pension fund participation helping to build the market. Pensions (and foundations and endowments, as non-taxable investors) can be an integral investor into private markets, both into funds and companies. Sophisticated pensions like CalSTRS, CalPERS, CPPIB, OTTP, and more have been integral parts of the fabric of the development of private markets with their support of large funds and their innovative ways of thinking about co-investment and direct investment. Their innovation and success shows that LPs can play a part in developing an ecosystem. As more LPs look to invest into Europe, the complexion of LPs in funds should change, which could continue to grow the ecosystem.

📝 The Gap Between Public and Private Real Estate Widens on Office Fears. Did Investors Over-React? | Hannah Zhang, Institutional Investor

💡Have remote workers made the office obsolete? It remains to be seen whether or not remote work will have a negative impact on the stock prices of publicly traded real estate companies. Investors in REITs had been concerned about macro headwinds and negative headlines about remote workers killing the office, but, according to Uma Moriarity, senior investment strategist and global ESG lead at CenterSquare, she believes that the REIT market has clearly “overreacted” to the macroeconomic headwinds. There’s a huge spread between the price of publicly traded properties and their privately held peers. The capitalization rate for REITs (real estate investment trusts) rose from 4.9% to 6%. The current cap rate for REITs is now 50 basis points (0.50%) higher than that for private real estate investments. To Moriarity, this signals that the REIT market “overreacted” to macroeconomic headwinds and “today [makes for] a really interesting opportunity for a real estate investor to put incremental capital into the REIT market, because you are able to get access to the same types of investments, but at a discount. She also notes that the office sector only represents 3% of the REIT market, with a larger portion of the REIT market covering other areas of commercial real estate that are doing well fundamentally in her mind. She’s also particularly bullish on data centers, which she believes will do well given the rise in AI.

AGM’s 2/20: Real estate is in an interesting spot. Interest rates have had an impact on both commercial and residential sectors, creating challenges for investors and real estate operators. What’s interesting about Moriarity’s analysis is that it shines a light on the concept of where investors can find value in the current market environment. Public markets — whether it be equities or real estate — may be mispricing assets relative to private markets. And when liquidity and risk is factored in, then it’s possible that investors may begin to favor public markets investment options over private markets investment options in certain investment strategies. This will be an interesting trend to follow from both a fundraising and alts product innovation perspective, as we are beginning to see more liquid products come to market for investors.

📝 Ryan Reynolds stars in role of investor with savvy eye for sports | Christopher Grimes and Samuel Agini, Financial Times

💡Hollywood actor and entrepreneur Ryan Reynolds continues to take his experience of aligning with successful brands and companies to continue his journey of investing in sports. The Financial Times reports that he has made a significant investment in the Alpine Formula One racing team, alongside other investors including RedBird Capital Partners (which recently bought AC Milan). This move follows Reynolds’ success with the Wrexham AFC, which he purchased in 2021 alongside fellow actor Rob McElhenney and helped revive through clever marketing and a reality show, Welcome to Wrexham, as the club enjoyed a historic season that saw them achieve promotion to League Two of The Football League (listen to more about Wrexham on AGM with this podcast episode featuring Wrexham’s Advisor to the Board, Shaun Harvey). Reynolds, known for his role as Deadpool, has a knack for juggling his roles as dealmarker and Hollywood superstar, with an uncanny ability to focus on the task at hand. Despite his busy acting career, Reynolds has also been involved in several business ventures, including the sale of Aviation Gin and Mint Mobile. The Alpine F1 investment expands his sports portfolio as Formula One gains popularity in the US. The sport, which has long struggled to break into the US market, has slowly grown since US telecoms billionaire John Malone acquired F1 for $8B in 2017 through his Liberty Media Group. Reynolds’ primary focus remains his acting career, with the next installment of Deadpool set to release next year.

AGM’s 2/20: The collision of culture and finance is alive and well — and Ryan Reynolds is a poster child for how to do this well. Combining his marketing acumen and ability to reach millions of people with his cultural influence with a sharp investing prowess, Reynolds has done an incredible job of both leveraging his talents and skillset of building stories and building brands with bringing the right industry experts who possess a wealth of experience and knowledge, like Shaun Harvey (link to his AGM podcast episode above), to the table to help run these operations. Reynolds’ (and McElhenney’s) success with Wrexham and with consumer companies Aviation Gin and Mint Mobile can provide a blueprint for creators on how to take their brand, community, and reach to invest in and build successful businesses, which will result in the continued mainstreaming of alts (as I’ve discussed here).

Reports we are reading

📝 Challenges for emerging managers | Max Navas, Susan Hu, Pitchbook

💡 Emerging managers are facing a much different fundraising environment than the past 18 months. Pitchbook dives deep into just how markedly the fundraising environment has changed, which has presented a myriad of challenges for many new and smaller funds. Market volatility in 2022 has altered the flow of capital, impacting the distribution and investment portfolios of limited partners. 2022 marked a 34.9% YoY decline in capital raised by emerging managers. This trend has continued through 2023 year to date, during which emerging managers secured $2.3B. As a result, 2023 is poised to be the first year since 2016 to see emerging managers close less than $20B in commitments. Emerging managers are now facing a much more difficult fundraising process than those who raised in 2021 and 2022. In 2022, the number of funds closed by established managers outpaced those led by emerging managers for the first time, with established managers commanding a much larger share of the capital raised in the US VC market. Emerging managers only raised 21.1% of the total funds secured. LPs focus on more established managers could have an impact on smaller VC ecosystems if emerging managers, who often grease the wheels for company-building in startup ecosystems, raise less capital.

AGM’s 2/20: Macro impacts micro. The macroeconomic environment and sharp change in interest rates has had an impact that’s flowed through public markets and into private markets. The much discussed denominator effect has had ripple effects on the venture market. Institutional investors have had to modulate their exposure to private markets, which has in part meant cutting back on commitments to PE and VC funds or reducing the number of manager commitments they are making. At the same time, emerging managers generally raise from the HNW channel, with family offices, HNWIs, and non-institutional investors often supporting smaller funds and first-time funds for both structural and non-structural reasons. HNW capital has also experienced a shock from public market declines. Many HNW investors and family offices, while they remain interested in venture and private markets, have had to reduce commitments or cull manager relationships because of how market performance has impacted their liquidity. With a new interest rate regime upon us, it wouldn’t be surprising to see emerging managers continue to face headwinds with capital raising — or to see some emerging managers join bigger platforms or be acquired by larger funds. While the going may be tough, hardship also leads to opportunity, so there will certainly be funds who perform well, even if fund sizes are smaller than anticipated, and will build enduring franchises over time.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Goodwater Capital ($4B AUM consumer tech VC) - Director, Seed Investments. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - West, Regional Director, Vice President / Senior Vice President. Click here to learn more.

🔍 Allocate (VC infrastructure investment platform) - Managing Director, Alternatives (Sales). Click here to learn more.

🔍 Republic (Multi-strategy alternative investment platform) - Chief Technology Officer. Click here to learn more.

🔍 73Strings (Valuation and portfolio monitoring for alternatives funds) - Analyst, Portfolio Monitoring. Click here to learn more.

🔍 Isomer Capital (European VC fund of funds) - Investor, Secondaries. Click here to learn more.

The latest on Alt Goes Mainstream

Recent episodes and blog posts on Alt Goes Mainstream:

🎙 Hear $18B AUM Savant Wealth’s award-winning CIO Phil Huber talk about how LPs can build a strategy for investing in private markets. Listen here.

🎙 Hear Avlok Kohli, AngelList’s CEO, talk about how they are building the company of companies that is powering private markets. Listen here.

🎙 Hear John Avery, VP Digital Assets, Tokenization, Web3 at fintech giant FIS talk about how evolutionary changes can lead to revolutionary changes in private markets. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, and I take the pulse of private markets on the first episode of our monthly show, the Monthly Alts Pulse. Watch here.

🎙 Hear Seyonne Kang, Partner and member of the private equity team at $134B AUM StepStone, discuss how the VC industry is dealing with today’s venture market. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear 44th Vice President of the United States and Chairman of Cerberus Global Investments Dan Quayle share his insights on geopolitics and investing. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Riley Robinette for his contribution to the newsletter.