AGM Alts Weekly | 5.28.23

AGM Alts Weekly #3: Making private markets more public, every week.

👋 Hi, I’m Michael and welcome to my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. The Alts Weekly features the AGM Index of publicly traded alternative asset managers.

Join us to understand what’s going on in alts so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Welcome

Welcome to the AGM Weekly Newsletter. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Good morning from Los Angeles, where I’m packing my bags for a two week trip to Europe to speak at SuperVenture and South Summit and meet with a number of companies, funds, and investors in private markets.

I’ll be in London, Berlin, and Madrid and I’m excited to see our founders and funds in those respective cities and meet those of you I haven’t met yet.

If you’re going to be in Berlin for SuperVenture or Madrid for South Summit, get in touch! Would love to meet.

Happy Memorial Day weekend to all my American friends and looking forward to seeing friends and family next week in Europe.

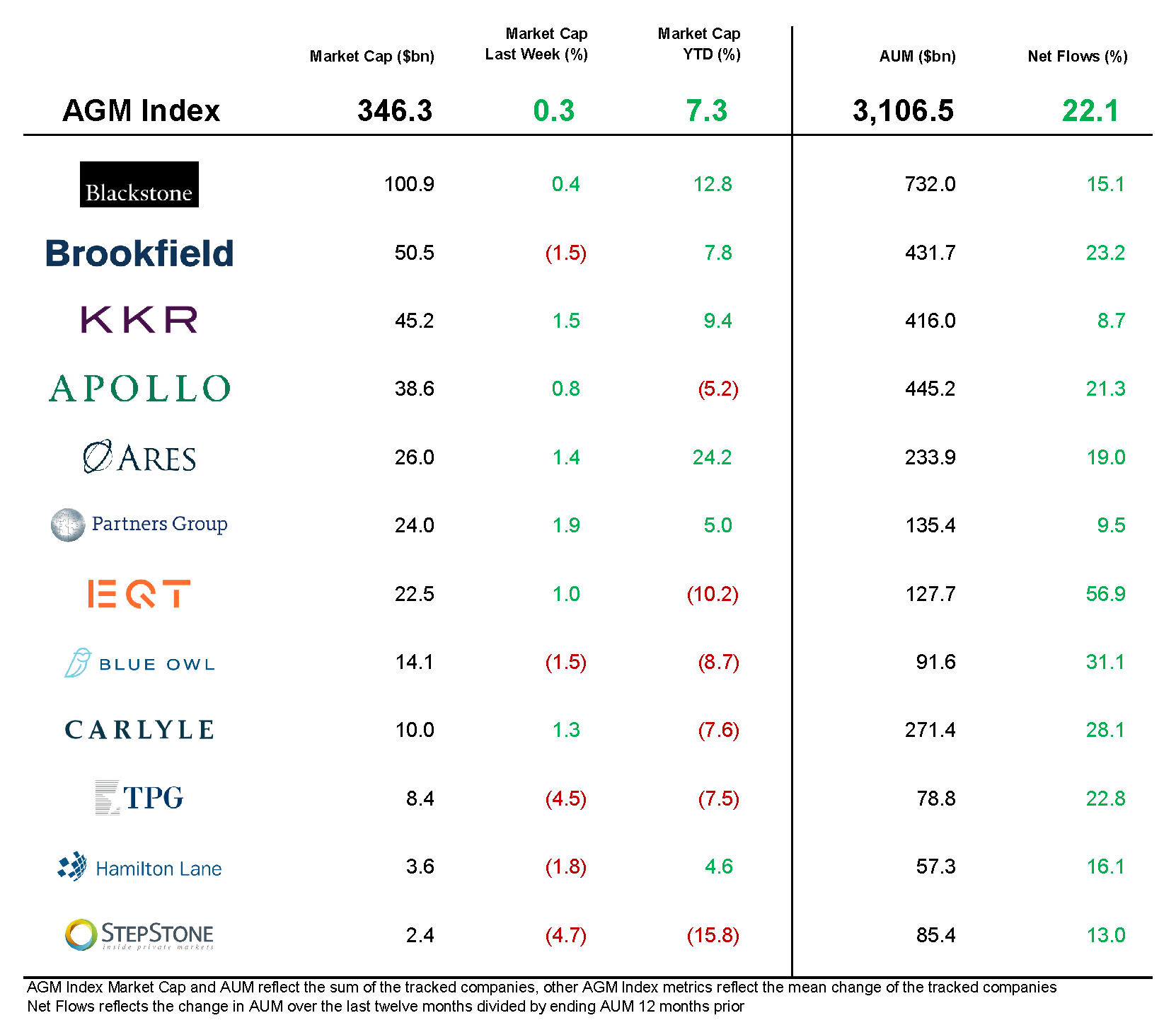

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

AGM News of the Week

Articles we are reading

📝 Private Assets Drove Endowment and Pension Returns Last Year. Now They Are a Drag | Michael Thrasher, Institutional Investor

💡Exposure to private equity and venture capital is causing public pension funds and endowments to fall short of their benchmarks, according to Markov Processes International. Public markets have rebounded this year, but gains in public markets aren’t enough to overcome markdowns on private assets. The gap between median pension and endowment performance and their benchmarks is widening. The growing allocations to private equity and venture capital that drove returns in recent years is now pushing the median pension and endowment performance below the allocators’ benchmarks. MPI estimated the median Ivy League endowment return so far for the 2023 fiscal year is 1.9 percent. Meanwhile, a global 70-30 benchmark, the standard used for endowment performance, is up 6.1 percent during the same period.

AGM’s 2/20: Pension and endowment performance in the private markets segment of their portfolio has a few major impacts for the alts space. 1/ Fund managers have to be aware that institutional investor participation in future funds may be more muted or allocators may cull existing relationships due to overexposure to private markets and poor performance. 2/ Institutional investors may need to sell portions of their private markets portfolios in order to meet their investment mandates, making secondaries an attractive corner of the alts market right now. 3/ The structural challenges noted above with institutional investors mean that private funds may be required to shift their focus to raising additional capital from the HNW and individual investor channel, which is structurally underallocated to alts. This explains why infrastructure platforms like iCapital, CAIS, Moonfare, Allocate, and others serve a need in the market for both GPs and LPs. 4/ LPs may demand more real-time and transparent reporting on private assets. This demand may create the need for innovation in fund accounting, valuation, and portfolio monitoring, gaps that the likes of LemonEdge and 73 Strings are filling.

📝 Allocators Ignored Cash for Years. They Can’t Anymore | Alicia McElhaney, Institutional Investor

💡How allocators managed their liquid holdings was a once-overlooked part of the asset allocation puzzle. But the recent collapses of Silicon Valley Bank and First Republic Bank has prompted some capital allocators to reconsider their cash management strategies. $11B AUM OCIO Global Endowment Management’s Co-Founder and Managing Partner Stephanie Lynch remarked at SALT’s iConnections Conference that “[their] smaller nonprofit organizations had put the cash management piece on the back burner.” She added that the fall of SVB “catalyzed” these organizations to consider the effect cash management can have on operations. Allocators are now having to answer questions such as how much money to keep in cash versus allocating to money market funds and whether to sell off illiquid assets to preserve liquidity.

AGM’s 2/20: The regional banking issues of late had reverberations that were felt across private markets. Not only did it force many startups and private companies to think about where they hold their cash, but it also made funds and allocators rethink their cash management strategies. Funds and allocators have had to be mindful of their banking relationships and how they think about managing their cash positions so they can balance generating returns on their cash and the ability to easily access their cash. As GEM’s Stephanie Lynch said at iConnections, she expects to see more allocators use sweep vehicles to move cash into a money market fund.

📝 Asset-Based Finance: A Fast-Growing Frontier in Private Credit | Varun Khanna, Avi Korn, Christopher Mellia, KKR

💡Private asset-based finance (ABF) has shown strong growth since the Global Financial Crisis, with the market expanding by 67% since 2006. It now represents almost half of the overall asset-backed market. The future outlook is promising, with the market projected to reach $7.7 trillion by 2027. Factors like inflation, reduced traditional lending, and banking system volatility will drive the need for private ABF.

AGM’s 2/20: As private credit comes into focus in the current market environment, certain corners of private credit look to be attractive. KKR makes a strong case for why asset-based financing should be a focus for allocators. Asset-based finance can diversify credit exposures away from corporate debt. The ABF market is also much larger in size and scale than some listed corporate credit markets. Furthermore, the asset backed nature of this type of credit instrument offers an inflation hedge since the value of collateral, generally hard assets, often rises with consumer prices. I’d expect to see private credit become a major area of focus for alternative asset managers and platforms focused on private markets given its attractive risk-reward with, in some cases, equity-like returns with more downside protection than equities. It’s also no surprise that large alternative asset managers like Blackstone, Ares, Apollo, KKR, Blue Owl and others view the current market environment as an attractive capital raising and capital deployment period.

📝 Why BlackRock Is Building Strategic Partnerships With Family Offices | Michael Thrasher, Institutional Investor

💡BlackRock is forming strategic partnerships with family offices as wealthy investors seek external help to enhance their portfolios. While some family offices are sophisticated enough to underwrite and invest directly in deals, many family offices face challenges accessing top deals and managers, high fees, liquidity constraints, and lack of transparency. “I do think what we are seeing is recognition from large single-family offices that they can really leverage their partners on the asset management side,” said Whitney Ehrlich, Head of US Family Offices at BlackRock. More families are coming to BlackRock for investment support of some kind, whether it is for help sourcing deals, due diligence, or allocations, she added. Family offices plan to increase allocations to private investments, particularly private credit.

AGM’s 2/20: Family offices are highly interested in private markets, but many often don’t have the same capabilities or in-house resources as institutional investors to invest into alternatives. Family offices can certainly leverage the capabilities of a deeply connected and well-resourced institutional partner like an asset manager such as BlackRock, their wealth manager, or their private bank, but there are still challenges with this model. Having built the family office network at iCapital, I’ve seen some of the unique challenges that asset managers and alternative investment funds might face when working with family offices. Every family office is unique in their background, mandate, expertise, and resources / staffing related to private markets. As the saying goes, “when you know one family office, you know one family office.” Asset managers and alternative investment funds would do well to educate family offices on the merits of alts rather than sell their products, work with them in a consultative manner, offer them access to co-investments or unique investments, and build trust and community amongst their family office partners. Family offices place a high value on trust, information sharing, and community so asset managers can work to build long-term relationships by investing in these initiatives and community-building efforts. As technology solutions for private markets continue to improve and enable the wealth channel to access private markets, family offices will continue to be an area of increasing importance for GPs looking to raise capital. The question will be how can GPs deal with different, less well-defined sales cycles than many may be used to with their institutional LP relationships.

📝 Some GPs look to switch fundraisers amid Credit Suisse/UBS integration | Chris Witkowsky, Buyouts Insider

💡The UBS acquisition of Credit Suisse has an impact on the placement agent world. As UBS works through integrating various parts of Credit Suisse’s business into their own platform, the bank must figure out how to deal with fundraising mandates run by Credit Suisse’s Private Funds Group, one of the larger placement agents in the market. Given the time it may take to fully integrate Credit Suisse into UBS (UBS’s CEO said on a recent earnings call that it could take up to 3-4 years to integrate), it remains to be seen how much of the team from Credit Suisse will stay on at UBS and how many of Credit Suisse PFG’s mandates will be continued by the funds in market.

AGM’s 2/20: The fundraising market has already become much more challenging for GPs given the current market environment. For funds that were working with Credit Suisse, any further delays in fundraising could prove to be another challenge in an already difficult process. Many private equity funds and hedge funds use placement agents to help them more efficiently raise funds, so funds who were working with Credit Suisse may choose to look elsewhere for a placement agent relationship. But it’s worth noting that UBS’s private wealth business, which apparently works with half the world’s billionaires in some capacity, could prove to be attractive for some funds, particularly as more funds look to the HNW channel to raise capital.

📝 How have higher rates impacted alternatives? | David Lebovitz, Global Markets Strategist, JP Morgan

💡JP Morgan Global Market Strategist David Lebovitz covers how valuations across private markets have been impacted by a change in market and economic conditions. 2022 was characterized by a shift in public markets valuations, but due to the “private market lag,” private market valuations were somewhat immune. Lebovitz notes that the fact that private market assets are not marked to market on a daily basis is a feature rather than a bug of alternatives, particularly as lower volatility lends itself well to a long-term investment view.

AGM’s 2/20: Interest rates have certainly had an impact on valuations of private market assets. But impact to valuations have been felt differently depending on the specific type of asset. Risk assets were hit hardest by rising rates, with venture capital valuations gapping down significantly, particularly at growth stage. Buyout valuations proved to be more resilient, as many of these companies had features such as profitability. Real estate has been a mixed bag, with industrial asset valuations holding strong given low vacancy rates and rising rents, while commercial (office space) has been hit hard by a shift to remote work. Private credit has been impacted by higher rates with lenders and borrowers being forced to renegotiate terms due to floating rates. Depending on the strategy, hedge fund performance has been buffeted by higher rates. The punchline here is that private market assets have been impacted in different ways by rising rates and inflation, so investors are thinking about how to rebalance their portfolios. But investors also shouldn’t miss the forest for the trees — patience and a long-term investment outlook, coupled with lower volatility in private markets assets, can help investors spot opportunities and avoid rash decisions that impact returns.

📝 Investment in Solar Power Eclipse Oil for First Time | Will Horner, Wall Street Journal

💡Investments in solar are poised to surpass spending on oil for the first time, reflecting the widening gap between renewable energy funding and stagnating fossil fuel industries. Solar is expected to receive over $1 billion per day in investment this year, outpacing investments in oil projects. Factors driving the shift include government initiatives and the emergence of a clean global energy economy. Developing nations, however, have been slower to adopt renewables due to cost constraints. The pandemic and energy security concerns have further influenced the divergence.

AGM’s 2/20: The transition to clean energy is well underway. In the US, the Inflation Reduction Act has been an overall boon for climate related investments. At the end of the day, adoption of solar comes down to dollars and cents — and the economics of solar makes sense in a lot of places. Similarly, in Europe, the Russia/Ukraine war has acutely highlighted the desire for many European countries to focus on energy security and how to live without Russian energy. As such, a number of European companies focused on metering and solar are being built to meet the needs of Europeans and the region’s focus on a transition to clean energy. Between the influx of dollars flowing into climate focused VC funds and generalist VCs shifting a focus to climate tech, I’d expect to see significant interest from investors into climate related startups, particularly companies solving financing for clean energy solutions. This space has come a long way since I was an early employee at Mosaic in 2013, where it took a long time to convince investors why they should invest into a solar financing platform, but is now backed by one of the most well-known private equity funds, Warburg Pincus. Firms that have focused on sustainability well before it was en vogue, such as Capricorn Investment Group, should benefit from their industry expertise and knowledge across private markets investment strategies as everything from venture to private credit and asset finance should be attractive as the world transitions to clean energy.

Reports we are reading

📝 Europe and Israel’s startup founder factories | Accel x Dealroom

💡Talent and innovation emerging from European and Israeli unicorns continues to gather pace as 221 of the region’s 353 VC-backed unicorns have fueled 1,171 new tech-enabled startups. More than half (54%) of this new wave of startups were founded in the same city as the unicorn they were spun out of and 59% have already secured private funding. This report explores not only the trends emerging in this new wave of startups, but also the journey from unicorn employee to tech startup founder in Europe and Israel. These founders are in a strong position to build the next generation of tech leaders due to their experiences before and during their time at the unicorn.

AGM’s 2/20: Europe is in the midst of an exciting evolution as a tech ecosystem. I’ve covered the rise of European venture (here) and it’s clear that the European venture market has come a long way in the past 10 years. And the next 10 appear poised to be even more promising. Market dynamics suggest that Europe should continue to grow into a thriving startup ecosystem for founders and funds alike, and make for a compelling opportunity for funds, particularly early-stage and emerging managers, to outperform. Europe has a number of fundamentals in its favor: leading research universities, a shared value system, engaged policymakers, embedded transport infrastructure and strong talent. This report by Accel and Dealroom provide further proof that Europe’s tech ecosystem is quite promising.

Interviews we are watching

🎥 iCapital x Alt Goes Mainstream Monthly Alts Pulse | Lawrence Calcano, iCapital & Michael Sidgmore, Broadhaven Ventures and Alt Goes Mainstream

💡Lawrence Calcano, the Chairman & CEO of iCapital, and I sat down live in iCapital’s studio in New York for the first episode of the Monthly Alts Pulse. As the leader of a platform that is responsible for the majority of individual and advisor-led investment flows into the alts space, Lawrence has his finger on the pulse of what’s happening in private markets. We make sense of the current market environment and where advisors are spending their time in private markets right now.

🎥 Bloomberg TV Wall Street Beat interview with Goldman Sachs co-head of Global Private Wealth Management Meena Lakdawala-Flynn | Bloomberg TV, Sonali Basak and Matt Miller

💡Sonali Basak and Matt Miller from Bloomberg TV sat down with the co-head of Global Private Wealth Management at Goldman Sachs, Meena Lakdawala-Flynn, to discuss how family offices are navigating the current market environment. Goldman recently released a family office survey, where they surveyed over 160 family offices, 70% of whom have over $1B in AUM. Goldman found that family offices have meaningful exposure to alts — and many (41%) are looking to increase their exposure to private equity going forward. Family offices are currently interested finding ways to generate equity-like returns with downside protection, so they are looking at private credit, secondaries, and private real estate.

🎥 Apollo’s Jim Zelter: Private Credit a Tool to Get Deals Done | Bloomberg TV

💡Apollo Co-President Jim Zelter recently came on Bloomberg TV to discuss changes in the private credit market. Zelter believes that private credit is attractive now due to its economics. Private equity sponsors can still get capital, but the cost of capital is higher — and private credit funds are the beneficiaries. Zelter expects to see fundraising for private credit funds to be popular as private credit has become a more mainstream part of investors’ alternatives allocation over the past few years and as investors look for yield with attractive downside protections.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Goodwater Capital ($4B AUM consumer tech VC) - Director, Seed Investments. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - West, Regional Director, Vice President / Senior Vice President. Click here to learn more.

🔍 Allocate (VC infrastructure investment platform) - Managing Director, Alternatives (Sales). Click here to learn more.

🔍 Republic (Multi-strategy alternative investment platform) - Chief Technology Officer. Click here to learn more.

🔍 73Strings (Valuation and portfolio monitoring for alternatives funds) - Senior Associate, Portfolio Monitoring. Click here to learn more.

🔍 bunch (SPV and investment infrastructure platform for VCs and startups) - VP Commercial. Click here to learn more.

The latest on Alt Goes Mainstream

Recent episodes and blog posts on Alt Goes Mainstream:

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, and I take the pulse of private markets on the first episode of our monthly show, the Monthly Alts Pulse. Watch here.

🎙 Hear Seyonne Kang, Partner and member of the private equity team at $134B AUM StepStone, discuss how the VC industry is dealing with today’s venture market. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear 44th Vice President of the United States and Chairman of Cerberus Global Investments Dan Quayle share his insights on geopolitics and investing. Listen here.

🎙 Hear Mark Anson, the CIO of $28B Commonfund, discuss why he thinks size discipline and sector focus lead to outperformance in VC. Listen here.

🎙 Hear Filip Dames, Founding Partner at leading European Seed VC Cherry Ventures, share why he’s so excited about the European venture ecosystem right now. Listen here.

🎙 Hear Graham Elton, Partner & Chairman of EMEA Private Equity at Bain & Company discuss how the $3.7 trillion in dry powder in private equity will get put to work. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Jack Knibb and Riley Robinette for their contributions to the newsletter.