📝 Alternative thinking: Connecting the dots with the data with RIA CIOs and KKR's 2025 RIA Private Markets Survey

Conversations with private markets leaders Beacon Pointe's Michael Dow, Cary Street Partners' Matt Rubin, and KKR's Matt Magill

Are private markets still alternative?

A recent conversation with CIOs Michael Dow of Beacon Pointe, Matt Rubin of Cary Street Partners, and KKR’s Managing Director and Head of RIA & Bank Trust, Global Wealth Solutions Matt Magill endeavored to do two things. First, hear the nuanced perspectives of two CIOs who are actively allocating to private markets, and KKR, a leading global investment firm that aims to be a solutions provider to RIAs seeking exposure to private markets. Second, bring to life KKR’s 2025 RIA Private Markets Survey.

Both Beacon Pointe’s Dow and Cary Street’s Rubin echoed the perspective that private markets are “foundational” to how private clients should approach how they aim to achieve their investment goals and are “key building blocks and core to portfolios today.”

While Dow and Rubin expressed both a desire and need for clients and advisors to allocate to private markets, they are aware that their respective firms are likely on the far end of the adoption curve when it comes to private markets.

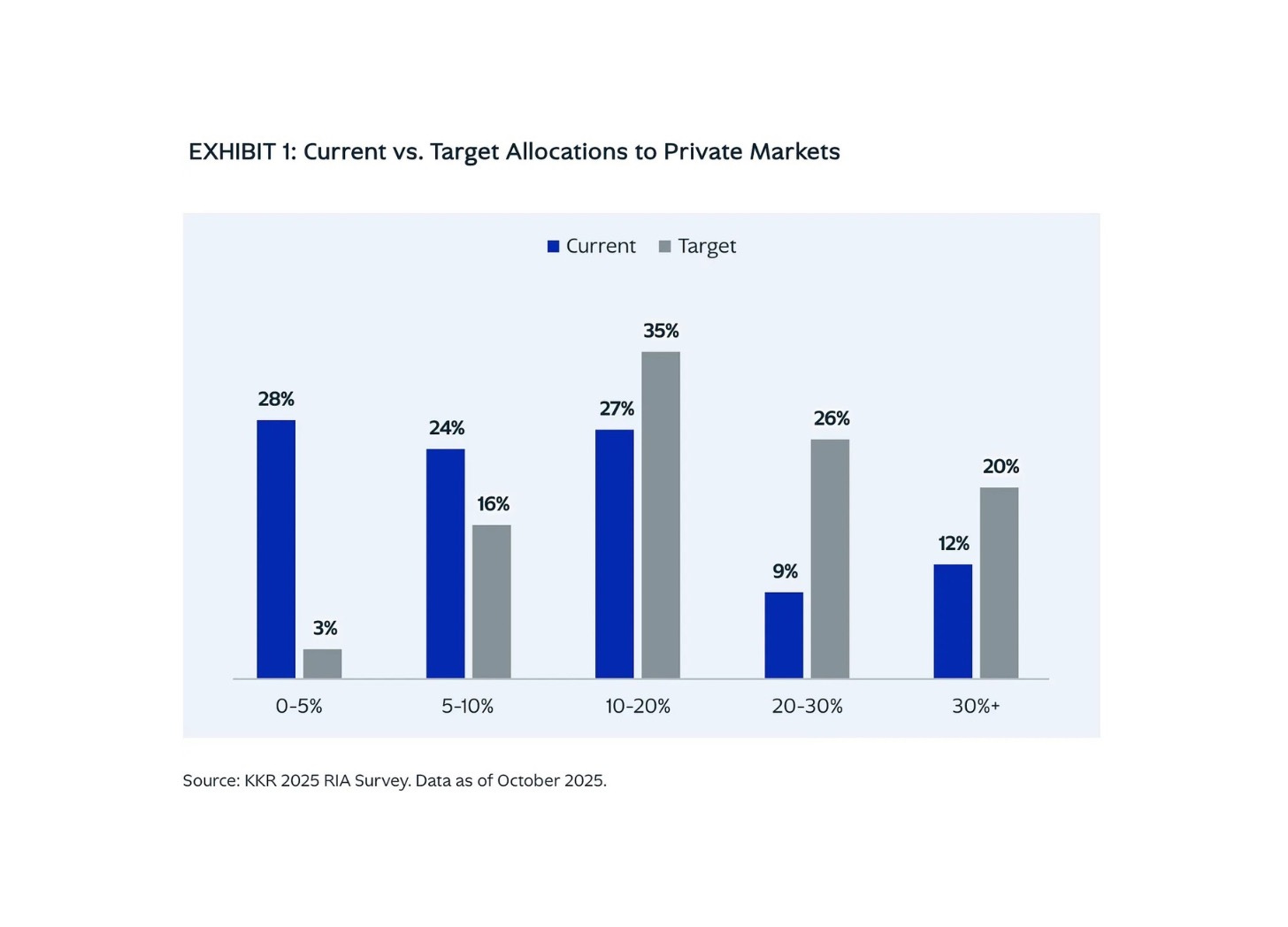

The reality is that many advisors are structurally underallocated to private markets. Dow noted that many institutional investors reside closer to 35-40% allocated to private markets.

Over 52% of RIAs surveyed by KKR have allocations of 10% or less to private markets, as the below chart from KKR’s survey illustrates.

That figure is also below the target allocation that both Dow and Rubin recommend for many advisors: 15-20%.

From interest to implementation

KKR’s survey indicates that advisors are interested in increasing their allocations to private markets.

How do advisors go from interest to implementation?

The what, how, and where of implementing private markets in client portfolios has now moved to the forefront of the discourse between advisors and investment firms.

It’s also a question that Dow, Rubin, and Magill have all spent meaningful time on.

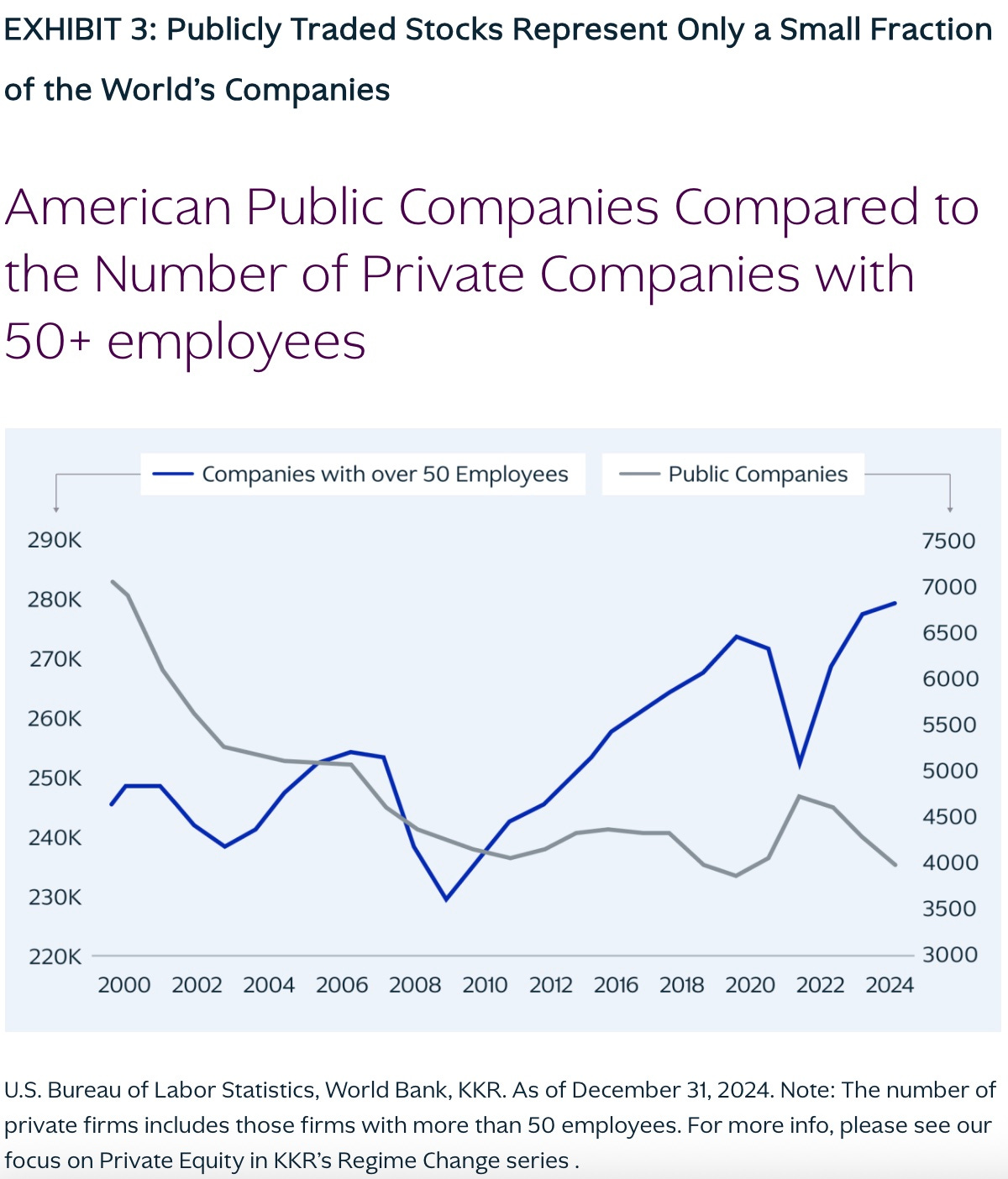

KKR’s Magill noted that concentration in public markets results in investors missing out on much of the investable universe if they are unable to allocate to private markets. The majority of that investable universe is largely private, as the below chart from a KKR report illustrates.

Both access to private markets and new structures for investors, Magill noted, have enabled advisors to scale private markets across client books by reducing investment minimums, increasing operational efficiency, and offering better access.

How advisors access private markets was a major part of the conversation.

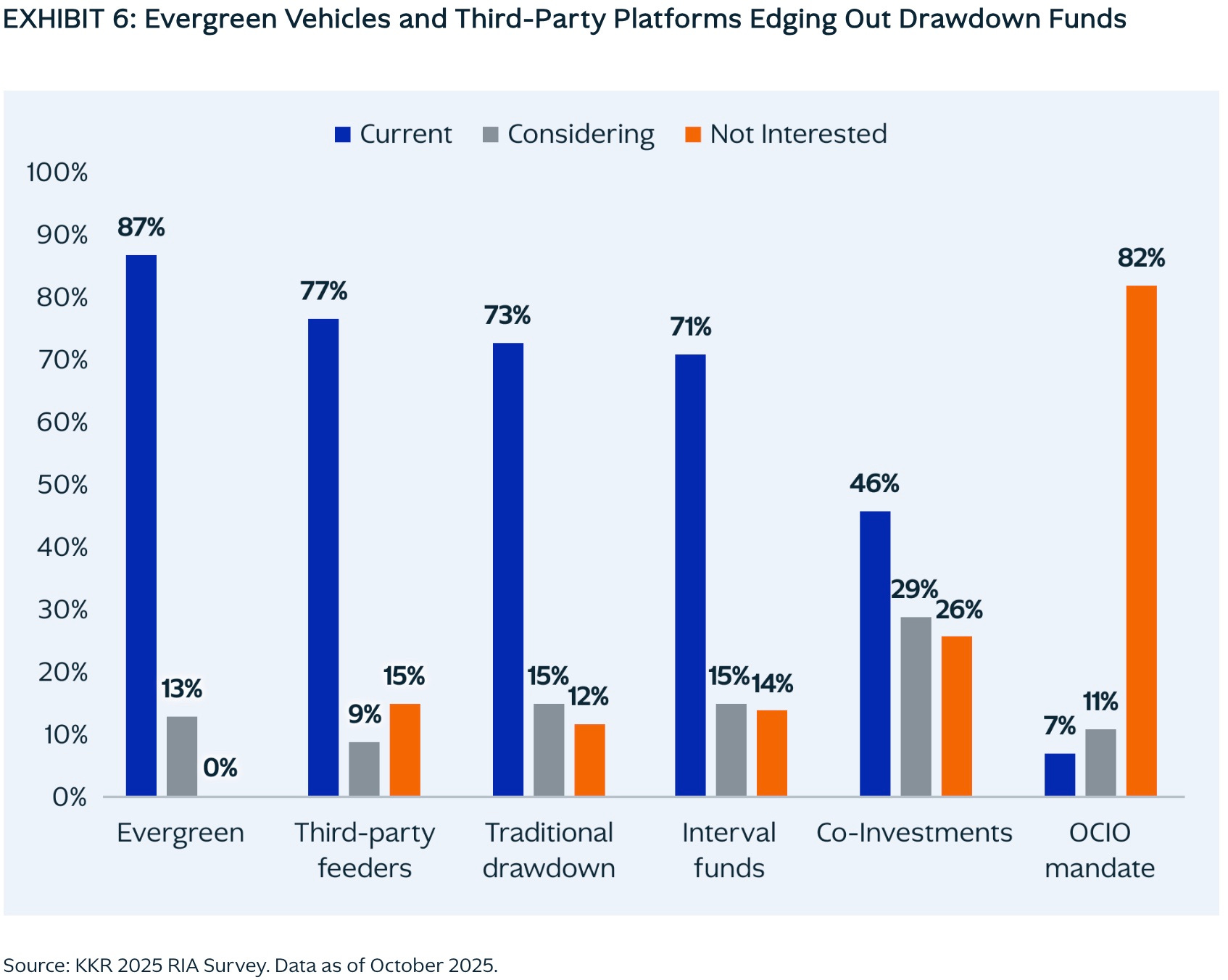

The data from KKR’s survey bears out that access is unlocking increased wealth channel participation in private markets.

Most advisors surveyed by KKR currently access private markets through evergreen vehicles.

It’s notable that no advisors reported that they were “not interested” in evergreen vehicles.

Advisor interest in evergreens dovetails with Magill’s comments about a focus on operational efficiency.

Both Rubin and Dow echoed this sentiment while also making it clear that both advisors and clients must understand the mechanics and purpose of evergreen structures. Rubin said that the “biggest value of an evergreen vehicle is the client experience and ease of use.” Dow called evergreen funds an “easy button.”

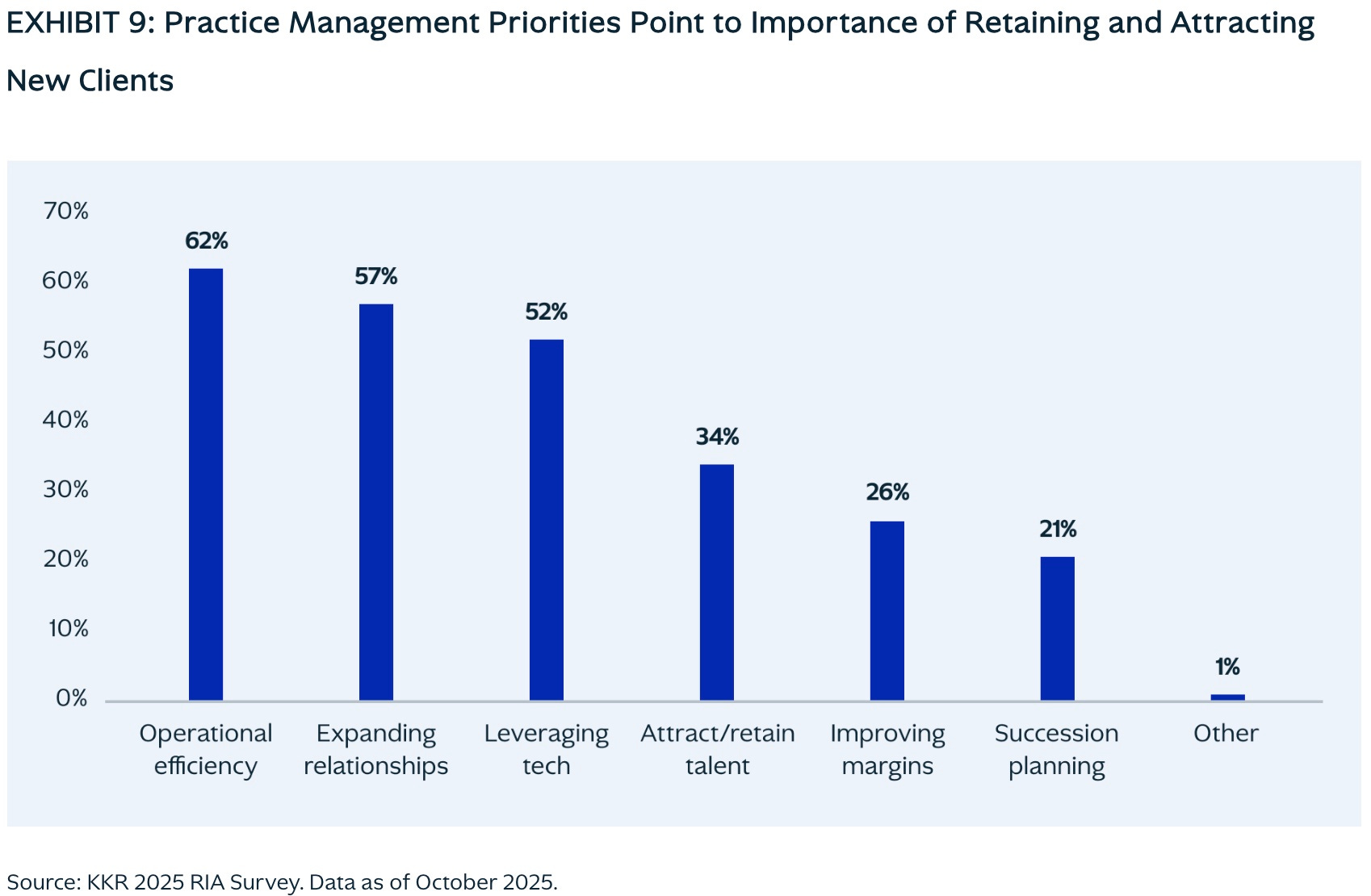

Magill, Rubin, and Dow’s comments are supported by the survey data. Advisors rank operational efficiency as their main priority for retaining and attracting new clients. Evergreens appear to play a role here for advisors.

Despite advisors’ interest in evergreen vehicles, KKR’s survey data also suggests that the perceived demise of both feeder funds and drawdown funds is greatly exaggerated.

A number of advisors surveyed employ both third-party feeders and traditional drawdown funds in a big way. A handful of advisors who don’t use third-party feeders or drawdowns are currently considering them.

What’s emerging isn’t a replacement dynamic so much as a refinement of how advisors are deploying different structures. Many RIAs are increasingly utilizing both evergreen and drawdown vehicles in complementary ways. An advisor might utilize drawdown funds for Qualified Purchaser clients while leveraging evergreen more broadly across Accredited Investor client bases. Other advisors are using evergreen funds as a core private markets allocation and layering in drawdown funds as satellite exposures to access more niche or strategy-specific opportunities.

The rise of evergreen structures doesn’t appear to signal the downfall of the drawdown. Instead, it suggests that advisors are becoming more deliberate about matching structure to client segment and portfolio role.

Another interesting datapoint from the survey is the lack of interest from advisors in leveraging an OCIO mandate.

As centralization of the CIO function within large wealth management platform moves into the mainstream, it appears that advisors and wealth management platforms are not looking to outsource their investment decisions. If anything, large wealth management platforms are bringing OCIOs in-house, as evidenced by the acquisitions of NEPC by Hightower, the mergers of Agility and Verus Investments with Cerity, and the acquisition of Hall Capital by Pathstone.

This sentiment aligns with Rubin’s view that wealth management platforms and CIOs should preserve the “entrepreneurial spirit of the advisor” by not taking away the advisor’s ability to decide how they want to deliver solutions to clients.

Both Dow and Rubin noted that scaled RIA platforms have the benefit of providing a broader toolkit to advisors, enabling advisors to marry up what the CIO chooses to put on platform and what the advisor believes is best for the client.

Rubin called it the “cafeteria,” where advisors have a buffet of choices for how they want to construct a client portfolio. He added another layer of nuance to this point, noting that models will be a critical component of an advisor’s toolbox because “customization at the client level is critical.”

If wealth management platforms, CIOs, and advisors are sticking to home cooking, how are they approaching allocations to private markets?

The devil is in the details

Dow, who has a background in managing risk and taking risk as a Senior Portfolio Manager at UBS Asset Management, said that allocators should ask what they are capturing in private markets that they cannot capture in public markets.

He highlighted two private markets premiums that investors can — and should — be compensated for when done right: the “illiquidity premium” and the “complexity and information premium.”

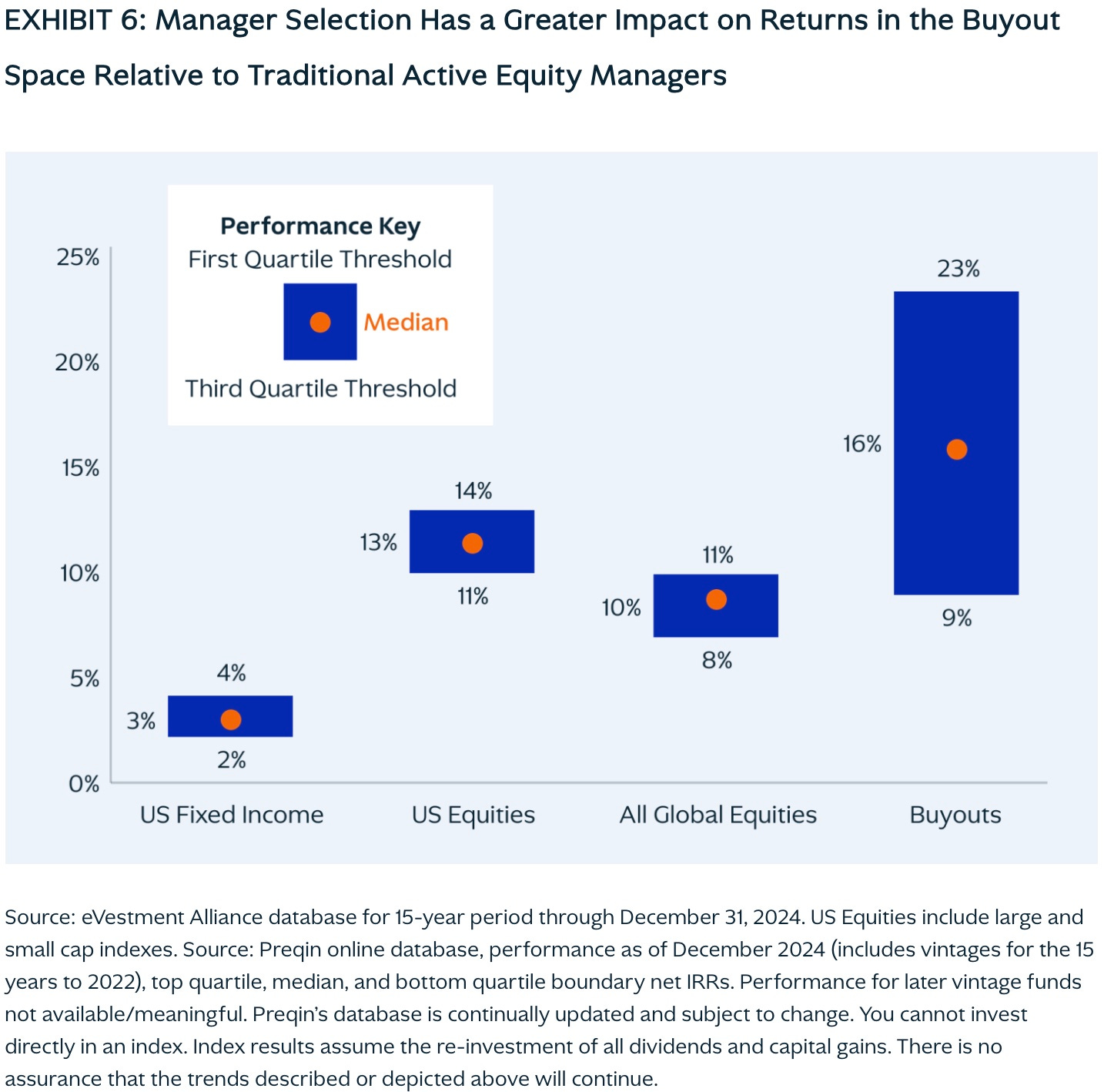

Getting paid for the illiquidity premium matters even more in private markets, particularly in corners of private markets where the penalty for picking the wrong manager is exceedingly painful.

The below chart from KKR’s December 2025 Insights paper hammers home just how imperative it is to get manager selection right in private equity. The spread between first and third quartile managers is 1400 basis points, as Magill noted. Spreads in other asset classes are significantly tighter.

Rubin, who has worked at both asset management firms and family offices, mentioned the importance of giving the advisor and client the freedom to tailor solutions to their specific needs even when there is guidance from an asset allocation framework that is “top-down from the CIO.”

Dow and Rubin may hail from different backgrounds, but they both asserted the importance of process in their investment decision making and asset allocation approach.

Trust the process

Magill talked about the importance of having a time-tested process with repeatable playbooks and identifiable patterns. Magill’s colleague Josh Weisenbeck called this “making our own luck” in a 2024 Investment Insights paper.

Dow echoed this sentiment from the perspective of a wealth manager, noting that allocators should have the same capabilities and processes as asset managers.

Another component of process is mapping strategy to structure.

In a world where LPs are looking to do more with less, scaled alternative asset managers are endeavoring to be solutions providers to the wealth management firms with which they partner.

Magill noted that KKR’s aim is to be a solutions provider, so they are agnostic as to vehicle structure that an LP chooses to employ. Magill said that perspective has driven KKR’s approach to product structure, since they’ve built both their investment engine and vehicle structure in ways that deliver “the same investments, from the same team, at the same time.”

A focus on evergreen structures by Dow, Rubin, and Magill doesn’t mean they aren’t aware of both the importance of education and the risk that allocators in the wealth channel misunderstand liquidity.

They emphasized the importance of educating advisors and end clients, with Dow and Rubin noting that the biggest challenge is helping advisors position private markets solutions within client portfolios.

They all noted the importance of educating the advisor and end clients. Both Dow and Rubin said that the biggest challenge they face is educating the advisor on how to position the use of private markets solutions in a client portfolio.

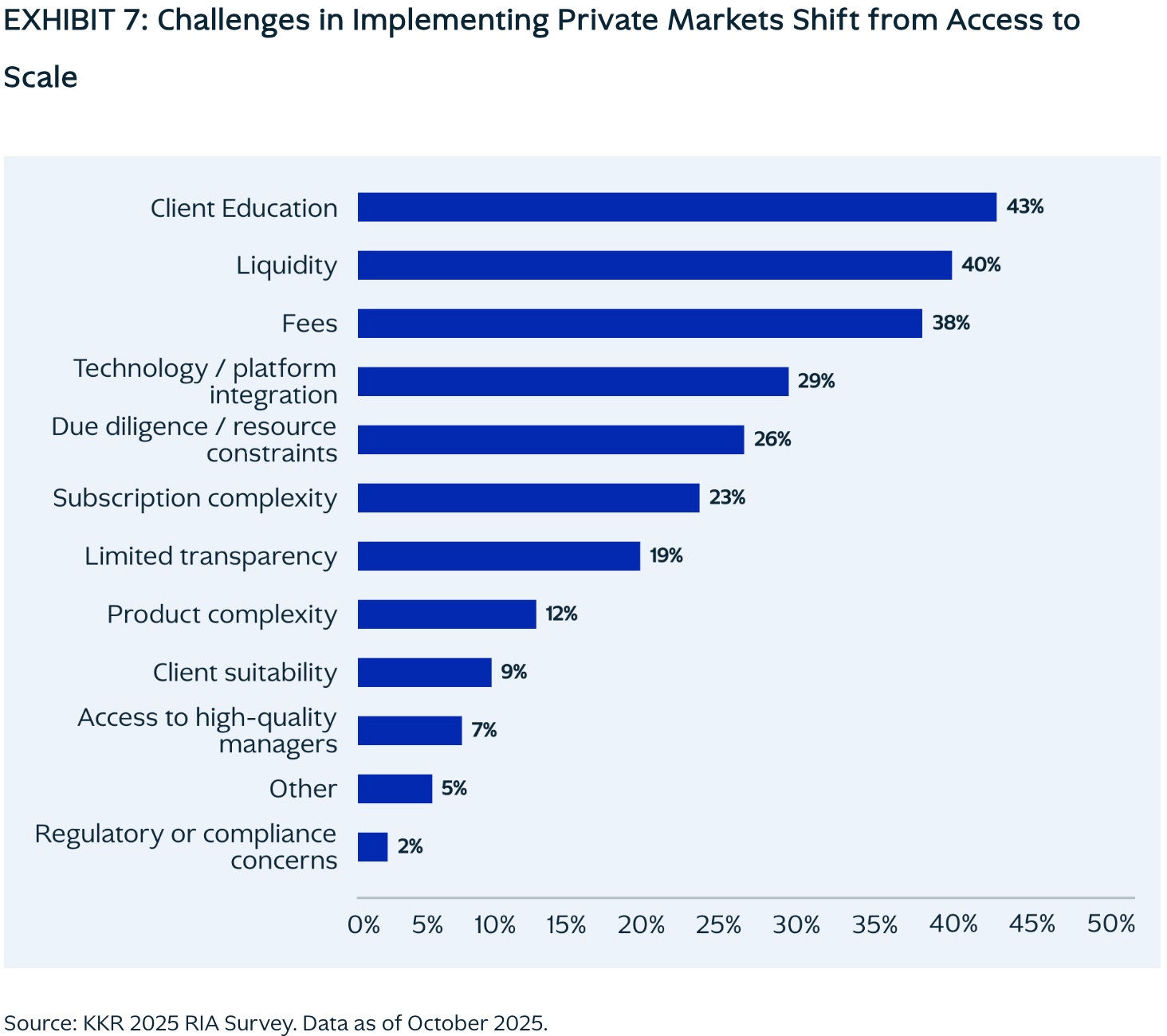

Education certainly seems to be on the minds of advisors and CIOs, as KKR’s survey data reveals that client education appears to be the main challenge in implementing private markets solutions.

What is some of the most impactful work asset managers can do to help move private markets from interest to implementation? Educate clients and advisors, Dow and Rubin noted.

Private markets solutions must be brought to the wealth channel in a thoughtful manner; it must be the right product for the right investor at the right time, delivered in the right way. Education, conversation, and data-driven insights can help advisors and clients in a thoughtful, appropriate way. The conversation with Beacon Pointe’s Dow, Cary Street’s Rubin, and KKR’s Magill is one of the puzzle pieces that can continue to bring private markets into the mainstream.

Disclaimer: Alt Goes Mainstream is an independent podcast and newsletter focused on the private markets industry. It is published for informational and educational purposes only and does not constitute investment advice, financial advice, legal advice, or any other form of professional advice. Nothing contained herein should be construed as a recommendation to buy, sell, or hold any security or investment product. Some companies, individuals, or organizations featured or mentioned in this newsletter may be current or past sponsors of Alt Goes Mainstream. Sponsorship does not influence editorial coverage, but readers should be aware that a relationship might exist. The author may hold direct or indirect investments in companies, funds, or other entities mentioned in this podcast or newsletter.

Yes — private markets are becoming implementation work, not allocation theory. You can see the shift when access stops being the constraint and process becomes the product.