AGM Alts Weekly | 10.15.23

AGM Alts Weekly #23: Making private markets more public, every week.

👋 Hi, I’m Michael and welcome to my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in alts so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Good afternoon from London, where I’ve been here for a week of meetings, speaking at the Mountside Ventures event, and organizing dinners co-hosted with Fidelity International Strategic Ventures and Mouro Capital.

After this past week’s events in Israel and Palestine, I feel that I must acknowledge it here before discussing anything else.

Last Saturday, the world witnessed heinous and indiscriminate actions against thousands of innocent Israeli civilians — grandparents, mothers and fathers, young adults, children, and babies kidnapped, brutalized, and murdered by Hamas terrorists. The news and images coming from the terrorist attacks by Hamas in Israel are horrifying and the loss of innocent lives of both Israelis and Palestinians is devastating.

One thing should be unequivocally clear: there is no place in the world for terrorism, anti-Semitism, or any form of hate against innocent people.

It’s hard to transition from something so harrowing and indescribably tragic to investing.

Investing does have the power to change the world.

Private markets offer the opportunity for investors — both individuals and institutions — to direct capital into initiatives that can make a difference. As investors and capital allocators, we do have the ability to effect change.

There are a number of areas where this can be the case — investing in climate solutions is one good example. The world requires urgent action — and a lot of capital — to come up with climate solutions.

Climate change has indelible impacts on our world. It’s contributes to lethal heat waves, year-round fires, destructive storms, and treacherous droughts that are killing thousands, displacing millions, and sowing the seeds of famine, disease, and war.

Solving the climate challenge is amongst the most important work of our time.

Solving the global warming challenge isn’t just a good thing to do — it’s good business. Every degree Celsius of warming costs, on average, 1.2% of GDP. And there’s a good chance that climate change will reduce global output by more than 50% by 2021, lowering per capita GDP by over 20%. For context, the Great Recession lowered global GDP by 6%.

Many investors, VCs / PE firms, corporates, and institutional investors, have begun to invest in the best companies that are building the category-defining technologies that help us get to net zero emissions and suck up trillions of tons of carbon from the sky.

Larry Fink, the CEO of $9T AUM BlackRock, is directing the world’s largest asset manager to focus on climate solutions, in large part because he sees the potential for outsized returns. He’s said that the next 1,000 unicorns ($B companies) will be companies that address climate change.

What I heard at meetings and conferences in Europe this week also reinforced the notion that capital can change an ecosystem. European tech is on the rise. Sure, the region may experience some turbulence as tech valuations continue to correct. LPs and GPs are looking for ways to create liquidity in the current environment as they grapple with a new normal. That was a recurring theme. But the long-term development of Europe’s tech scene looks promising.

Yoram Wijngaarde, the Founder and CEO of Dealroom, shared compelling data from their latest report at the Mountside Ventures event earlier this week. The combined enterprise value of European startups has grown 10x — from $335.9B to $3.4T — in the past 10 years.

Europe could very well become a leader in physical tech, leading the way in areas like climate, AI, and robotics — all categories that could have a major impact on our future.

Dealroom has found that over half the world’s top science clusters are in Europe. VC Sequoia Capital has stated that Europe has the highest concentration of AI talent. And it’s understandable why many are turning to Europe for engineering talent — they are talented, highly competent, and also cheaper than US developer talent.

Europe has a promising future ahead in tech. This didn’t happen overnight. It took patience, time, education, capital, and governmental support. Years later, the region is going from strength to strength — and there are many in the ecosystem who have dedicated meaningful time and effort to make that happen.

With its greatest ever abundance of talent, capital, and focus, Europe is primed for growth. I’m excited for the years ahead — and in particular for the positive impact that technology innovation coming out of Europe, particularly in physical tech, can have on the world.

If you want to learn more about the current state of the European tech ecosystem, you can listen, watch, or read to a few different podcasts and posts on the topic:

🎙Isomer Capital’s Joe Schorge on the evolution of the European VC ecosystem. Listen here.

🎥 a cadre of Europe’s most knowledgeable and thoughtful LPs on EUVC discussing the current investing environment in Europe, with EIF’s Head of VC Investments David Dana, KfW Capital’s Head of Investment Management Christian Roehle, and Isomer Capital’s Joe Schorge. Watch here.

🎙Cherry Ventures’ Co-Founder & Partner Filip Dames on building one of Europe’s seed funds. Listen here.

🎙bunch’s Levent Altunel and Enrico Ohnemuller on building the infrastructure to enable European angels, founders, and VCs to continue to grow the ecosystem. Listen here.

📝 my post on Alt Goes Mainstream on the continued rise of European venture. Read here.

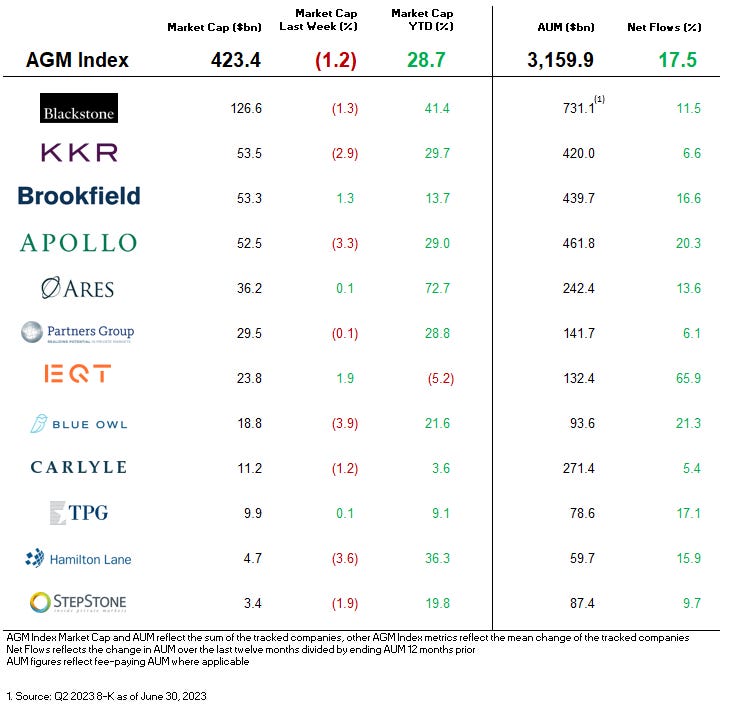

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

AGM News of the Week

Articles we are reading

📝 Industry watchdog says public pensions harbor valuation risk | Jessica Hamlin, PitchBook

💡An industry watchdog claims that public pension private equity portfolios are overexposed to valuation risk, calling into question the way that GPs value their portfolios. Equable Institute, a nonprofit that provides educational materials about public pension plans, claims that the lack of transparency into valuation practices could put LPs at risk of portfolio losses and ultimately impact payouts for public employees. Equable cites the fact that many private equity firms use different valuation methodologies to value their portfolio assets, making it challenging to have a uniform valuation framework and understanding of the true risk to a portfolio for LPs. Equable believes that US public pension plans have significantly increased the risk in their portfolios as they have increased their exposure to private, illiquid asset classes. A report from Equable estimates that pension plans’ risk associated with private investment managers’ overestimated valuations has grown from 9% in 2001 to 34.1% at the end of 2022. Part of the issue for both LPs and GPs is that GPs determine asset prices in a number of different ways. Some firms use the market approach, which values a private company using comparable public companies. Others use a discounted cashflow model to estimate a company’s revenue, expenses, and profit to project its worth over time. These methodologies are compounded by the fact that there’s often a time lag with valuation data. These factors all present challenges for how pension plans understand both their risks and ability to project pay out to plan beneficiaries. Assets valued incorrectly can have grave impacts on pension plans and their ability to meet return targets. The reported value of a pension's assets is used to determine beneficiary contribution rates, which means that an incorrect valuation of portfolio assets could have a meaningful impact on beneficiaries. 2022 witnessed some of the challenges associated with valuing private markets assets. Many pension plans were overallocated to private equity as a result of the denominator effect, when a decline in public equities shifted the balance of returns toward the private market portion of pension plans' portfolios.

💸 AGM’s 2/20: Valuation and portfolio monitoring is top of mind for GPs and LPs alike, particularly after 2022 resulted in a sharp correction in private market assets. The problem? The lag time for reporting and valuations to reset to accurately reflect current market pricing. This has been a particularly acute issue for institutional investors. The impacts of the denominator effect have meant that many institutions are overexposed to private markets, meaning that they can’t continue to allocate to private funds in the current vintage (which could be quite a strong performing vintage given market dynamics) and need to focus on liquidity and rebalancing their portfolios. This issue isn’t good for GPs either. The result is a more difficult fundraising environment for GPs, particularly if they deployed quickly in 2020 and 2021 and haven’t yet fully digested the impacts of a reset in valuations. What this does mean is that many GPs are shifting a focus to their back office to use more robust and real-time portfolio monitoring and valuation tools. We’ve seen it through the lens of our portfolio company, 73 Strings, which has seen many of the large GPs look to them for help on portfolio monitoring and valuation. I asked 73 Strings CEO Yann Magnan why he believes it’s the right time for valuation tools to move front and center in the conversation about private markets innovation. He said: “GPs are looking to use technology more to create more real-time and transparent valuation and monitoring, combined with more use of 3rd party opinion on valuations. Technology will help advance the quality and depth of valuation work, but it’s the combination of both that will take the industry to the next level.” Innovation in the post-trade segment of private markets investments could be a game-changer for the alts space. Better valuation data and monitoring tools enable GPs and LPs to have better purview into their underlying assets and into the risks at the portfolio level. There are a host of knock-on effects for a world where there’s less time lag and less backward-looking valuation data — LPs should be able to better understand their private markets exposure, making it easier for both GPs and LPs in fundraising cycles. Liquidity should also be easier to come by, as there’s more price transparency. This should also help grease the wheels for the ever-evolving secondary market. There’s still a ways to go with making post-trade more efficient and effective in private markets, but the focus is there and we are well on our way.

📝 Can private equity meet public responsibilities? | Sarah Murray, Financial Times

💡Private equity is a major engine of growth for economies globally. With companies owned by private equity in the US representing 6.5% of GDP in 2022, private equity wields meaningful economic power. Trillions of dollars have been poured into many of the biggest industries and sectors driving economic growth. Financial Times’ Sarah Murray dives into why many large private equity firms are looking to position themselves as sustainability leaders. In part, this is in response to demands from LPs. GPs too see reasons why focusing on sustainability is good for business. Ken Mehlman, Co-Head of the Global Impact Fund at KKR, affirms the assertion: “The lesson we’ve learned from the past 15 years is that an approach to ESG and sustainability that is focused on issues material to a company’s bottom line can be incredibly accretive from a value creation and value protection perspective. Detractors claim skepticism that private equity firms are serious about their sustainable business practices because “by default they’re private,” says Bruce Usher, a Columbia Business School professor and author of Investing in the Era of Climate Change. Usher does argue that the sector’s profit-driven approach can create a positive impact if efficiency and profitability of the business are aligned with initiatives that naturally create a positive impact. One area at the intersection of profit and impact that is certainly at the epicenter of private capital is clean energy. In 2022, private equity investment in renewable energy and cleantech in the US alone grew by almost 63% from 2021, with $26B in capital flowing into the space in 2022, an increase of $10B from 2021. Diversity and social equity are also major focus areas for private equity firms. GPs wield a significant amount of power — which can be used as a force for good if there’s a focus on sustainability. Firms are often in majority control positions and can leverage board representation and relationships with CEOs / management to implement sustainability strategies. Private equity firms can call on their wide purview and institutional knowledge to share portfolio company best practices. Swedish private equity group EQT, who has a considerable focus on sustainability within their portfolio, is helping its companies set science-based targets, which align with efforts to keep global warming to 1.5C above pre-industrial levels. EQT has brought on former Deloitte Partner, Bahare Haghshenas, to spearhead their sustainability implementation, metrics, and reporting as their Global Head of Sustainable Transformation. How does private equity square the circle investing into oil and gas companies? Well, Carlyle’s Global Head of Impact Megan Starr argues that the “largest decarbonization potential is in the most carbon-intensive businesses.” FT’s Murray points out that while this may be true, if the private equity sector is to convince the rest of the world that this strategy works, increased transparency will be of the essence. EQT’s Haghshenas agrees that the industry needs to “help portfolio companies move away from treating sustainability as primarily a matter of reporting and compliance.” She adds that “connecting sustainability to performance and value creation” is critical.

💸 AGM’s 2/20: Transparency appears to be a recurring theme in this week’s AGM. And for good reason. Transparency, whether it be with valuations or sustainability, will help move the industry forward. ESG is clearly top of mind for both GPs and LPs — and it could indeed help drive returns. The term “impact investing” is a loaded one within investment circles and somewhat understandably so. There have yet to be agreed upon definitions for impact measurement and reporting. And some LPs have questioned for years whether or not returns and impact can be mutually exclusive. But certain sectors represent both an opportunity for profit and meaningful impact. Climate is one of them. There’s clearly a lot of money to be made for investors as we all look to mobilize to suck CO2 out of the atmosphere and decarbonize the universe. But more importantly? The impact it can create. This is the best of both worlds and impact may have finally found the intersection point in a way where the mainstream investor, whether or not they care about impact, may in fact create a positive impact with their investments. As I mentioned above, investors have the ability to affect change with their checkbooks. It’s quite a responsibility, but investors can make an impact and make money at the same time.

📝 Fund firms launch private markets funds in race to beat alts shops chasing private wealth | Selin Bucak, Citywire Americas

💡Some of the world’s largest asset managers are very focused on providing the HNW channel with access to private markets funds. 20 of the 25 largest asset managers globally have either launched a private markets fund dedicated to individual investors or have distribution capabilities targeting the HNW client segment. JP Morgan Asset Management, UBS Asset Management, and BlackRock are among the asset managers who have launched dedicated private markets funds for HNWs over the past year. These asset managers are competing with the largest alternative asset managers, like Blackstone and KKR, who have set up private wealth distribution teams of their own to target the same client base. BlackRock, who boasts $320B in alternative assets, launched four strategies in 2023, including two European long-term investment funds (ELTIFs) and one of the first long-term asset funds (LTAFs) in the UK. Fidelity Investments recently launched its Multi-Strategy Credit vehicle as an interval fund and rolled out its first business development company, the Fidelity Private Credit Fund. Other banks and asset managers have also gotten into the game, including Goldman Sachs Asset Management and Schroders Capital. Asset managers recognize that product-market fit matters. Jacques Chappuis, Global Head of Distribution and Co-Head of Solutions and Multi-Asset Group at Morgan Stanley Investment Management remarked, “What’s critical is that we ensure that the product we’re providing has the appropriate characteristics to appeal to the specific market. One product we really don’t offer to HNW investors is private infrastructure. You look at the return profile and the lock up, very few HNW investors say that it makes sense.” Some notable firms, such as Franklin Templeton, Amundi, and DWS, are watching the trend closely and contemplating setting up their own dedicated funds. Technology platforms, such as iCapital, CAIS, and Moonfare, are also helping to move the space forward, as many asset managers have been signing partnerships with these platforms where they provide either infrastructure or distribution capabilities, or both.

💸 AGM’s 2/20: The race to work with the wealth channel is on. Initially, many private banks and traditional asset managers were looking for ways to help the wealth channel access top private equity funds. Now, they find themselves competing with many of the funds, like Blackstone and KKR, in a bid to have their own funds in the portfolios of HNW investors. The fact that traditional asset managers are getting into the game directly signals that they believe there’s enough potential growth within the alts space to turn this into a growth driver for their businesses. They also see the opportunity to create new products for a new type of investor. As both investors and product manufacturers become more knowledgeable about alts and the nuances associated with different products and strategies, I expect that we’ll see continued innovation on the product side. It remains to be seen whether or not creative product structuring will ultimately make sense for the alts space. Sure, there are regulatory constraints and apprehension about illiquidity for certain investors, but I’m not convinced that illiquid assets should be structured to become more liquid. Yes, it provides exposure to alts for these new investors in the space, but will it prove to generate superior returns relative to the fees paid? That remains in question.

📝 Reporter's notebook: Hunting for liquidity at BVCA Summit | Marie Kemplay, PitchBook

💡PitchBook’s Marie Kemplay shared her thoughts from this past week’s British Private Equity & Venture Capital Association Summit. Liquidity appears to be a sentiment echoed across conferences and meeting rooms in Europe. Unsurprisingly, unlocking liquidity for LPs is a major theme in Europe. While European LPs have experienced the growth of European private markets, and the tech sector in particular, many are still waiting for exits. Kemplay reports that many GPs and LPs are spending a lot of time thinking about the tools to create liquidity in Europe. Harriet Steel, global head of clients at private debt specialist Pemberton, predicts a continued expansion in the use of net asset value, or NAV, financing, believing it is set to become "probably one of the fastest areas of growth in private credit over the next several years." Lucia Villamor, a Partner at middle-market PE firm Endless, finds that many GPs are looking into continuation funds. While continuation funds done right can be a positive for both GPs and LPs, Villamor notes that it’s important to be cognizant of the challenges associated with continuation vehicles. She asks: "One, why are you doing this? Is your main driver really to maximize value for investors, or are you doing it to improve your DPI? And two, on pricing, if you are an LP that doesn't have the means to roll over into the new vehicle, are you effectively being forced to take in a really big discount? In most cases, continuation funds are being used in the right way, but you can run the risk of having angry LPs if not."

Other themes top of mind at the conference overlap with a number of topics discussed in this week’s newsletter. Many private equity firms cited a focus on ESG strategies — and not just for risk mitigation. Ashim Paun, Head of Sustainable Investing at Triton, cited that ESG can be seen as an opportunity to generate outsized returns. He pointed to the ability to transform the supply chain in the fertilizer business, traditionally a carbon-heavy sector, and how their investment in a company that will produce green ammonia could create new sources of revenues and drive returns.

Unlocking access to private markets was of course another theme top of mind for fund managers. Some in the space cited concerns about how opening up the asset class to more investors makes it harder for sensitive information on companies and funds to remain confidential. They cited a balance of keeping sensitive information under wraps and ensuring that access platforms are buttoned up in their approach and making sure that funds provide transparency to investors, particularly those newer to the asset class. One audience member asked a question that has been top of mind for many GPs and LPs throughout the wave of democratization: "Should more established investors be worried about their clout in the market being watered down by a wave of democratization?" Valid question, but, as I’ve said before, I believe we’ve reached the point of no return in private markets, where funds know they need to work with the wealth channel so they are less concerned with any negative impact on their reputation and LPs no longer view an asset manager’s focus on the wealth space as a signal that performance has suffered. A space that could undergo transformation is the co-investment space. Much like private equity saw institutional LPs become more active co-investors over the past 10-15 years, it appears that the co-investment space may be unlocked to more investors. Claudio Siniscalco, Founder and Managing Partner of Fiduciary Co-investment Partners, said: "Historically, I would say that there were 40 or 50 institutions that I saw again and again in every management presentation I went to over the last 20 years of doing this. I think that privileged group of co-investors is going to be disrupted.”

💸 AGM’s 2/20: Kemplay highlights a number of themes that appear to be top of mind amongst Europe amongst GPs and LPs. Liquidity is necessary to grease the wheels for continued LP participation in European venture for current vintages. This is crucially important as LPs are excited by the promise of the European tech sector, but also want to see that managers can prove they can generate distributions. Unsurprisingly, we are seeing a number of secondaries strategies launch in Europe, so we expect this to be a major area of focus for both GPs who can launch new fund strategies and for LPs who are looking for different ways to play the current environment and generate returns in private markets. Secondaries certainly could be an attractive strategy, particularly in Europe, where the VC sector saw records amounts of capital raised in 2021 and 2022 but now may be feeling the hangover from an inflated market. That does not mean, however, that there aren’t a number of quality companies that can emerge stronger on the other side. That’s exactly the question GPs and LPs are grappling with. Democratization of access is also a featured topic in Europe. We are certainly seeing more participation from the wealth channel in Europe. The BVCA participant who asked if GPs should be concerned about their reputation in the market if they move to focus on the wealth channel is asking the right question. But GPs have quite a good answer. Many of the largest GPs very well understand this trend and, not only have they grappled with the question, but have responded in full force to service the wealth channel, particularly in the US. Some of the most established GPs, such as Blackstone and Apollo, have made partnering with the wealth channel a key strategic priority. And they are far from the only ones to engage with the wealth channel. If anything, we’ll only continue to see more engagement and product innovation by these GPs specifically for the wealth channel — and that’s a net positive for the continued evolution of private markets.

📝 RIA Investor Merchant Eyes $400m-$550m Through Capital Raise, Eventual IPO | Ian Wenik, Citywire

💡Executives from Merchant Investment Management, a platform that invests into minority stakes of RIAs, indicated on a Wednesday morning call that the firm is now looking to raise between $400M and $550M, up from the $250M reported by Citywire in August. Sources reiterated that the New York City-based serial RIA acquirer is looking to add balance sheet capital instead of selling debt or equity, and will use the fresh capital to fund future M&A activity. Merchant Co-Executive Chairman Scott Prince told call participants that advisors at affiliated RIAs could present the capital raise as an opportunity for their clients. No hard timeline for the completion of the capital raise was given. Prince, the former Co-Managing Partner at alternative asset manager Skybridge Capital, serves as chairman of Merchant alongside former President of alternative asset manager Apollo Global Management Mark Spilker. Per the company website, the firm has backed 60 companies across 30 states and three countries, representing over $160B of assets in its ecosystem. Notable firms among those include LPL affiliate Private Advisor Group, hybrid RIA Concurrent Investment Advisors and boutique asset manager Morgan Dempsey Capital Management. In addition to the primary RIA investing business, Merchant also serves as an RIA lender and operates an alternative asset manager of its own. Merchant Co-Founder and Managing Partner Tim Bello added on the call that Merchant plans to eventually go public.

💸 AGM’s 2/20: Investing into RIA businesses continues to be front and center in the wealth space, so it’s no surprise that yet another wealth management investor looks to raise fresh capital to execute more investments and M&A activity in the RIA space. Given the influx of capital flowing into the space, it makes sense that firms believe that now is the time to make moves to acquire firms. The big question? Valuation. As I wrote a few weeks ago, it remains to be seen the multiples at which many of these rollups or larger firms will ultimately exit. Another interesting point from the Citywire article is that Merchant may look to raise some of the capital for its current raise from clients of Merchant backed RIAs. I expect this to be an increasingly popular trend going forward. Cresset Partners, who has been on the Alt Goes Mainstream podcast in the past (listen here), has built a model where clients are investors in their business and they have built private markets capabilities where clients have invested into as well. This is quite an interesting feature of wealth management platforms, where investment into wealth managers themselves constitutes private markets investments / alts exposure, so it will be interesting to see how this continues to evolve.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 bunch (Private markets infrastructure investment platform & SPV infrastructure) - Head of Commercial. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - Midwest, Regional Director, Senior Vice President. Click here to learn more.

🔍 Republic (Multi-strategy alternative investment platform) - Chief Technology Officer. Click here to learn more.

🔍 Isomer Capital (European VC fund of funds) - Investor, Secondaries. Click here to learn more.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

🎙 Hear Joe Schorge, Co-Founder & Managing Partner at one of Europe’s most active LPs, Isomer Capital, discuss why now is Europe’s time. Listen here.

🎥 Watch Marc Penkala, Co-Founder & Partner at Altitude, and I do a first-of-a-kind live podcast on EUVC. EUVC, the leading podcast championing European venture and fund syndicate platform, brought together one of their portfolio GPs, Marc Penkala of Altitude, and me for a VC / LP pitch session. Watch here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, and I take the pulse of private markets on the fourth episode of our monthly show, the Monthly Alts Pulse. Watch here.

🎙 Hear the incredible story of “tech’s most unlikely venture capitalist,” Pejman Nozad, Co-Founder & Founding Managing Partner of Pear VC, on how they’ve built a seed investing powerhouse. Listen here.

🎙 Hear sustainable investments pioneer Bill Orum, Partner of $9B AUM OCIO Capricorn Investment Group, discuss how Capricorn has proven that doing well and doing good don’t have to be mutually exclusive. Listen here.

🎙 Hear wealth management industry titan Haig Ariyan, CEO of Arax Investment Partners, share his thoughts on the private equity opportunity in wealth management and why the intersection of wealth and alts is one of the biggest trends in private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with a macro lens from John’s background as a leading macro hedge fund manager at Passport Capital and on micro VC from Ken’s background backing some of the top emerging VCs at Industry Ventures. Listen here.

🎙 Hear $40B AUM Cresset Co-Founder & Co-Chairman Avy Stein and Director of Private Capital Jordan Stein live from the Allocate Beyond Summit discuss how private markets are changing wealth management. Listen here.

🎙 Hear Alto CEO Eric Satz discuss how anyone can invest in alternatives through their IRA. Listen here.

📝 Read how 73 Strings CEO & Co-Founder Yann Magnan and team are leveraging AI to build a modern and holistic monitoring and valuation platform for private markets in The AGM Q&A. Read here.

🎙 Hear $18B AUM Savant Wealth’s award-winning CIO Phil Huber talk about how LPs can build a strategy for investing in private markets. Listen here.

🎙 Hear Avlok Kohli, AngelList’s CEO, talk about how they are building the company of companies that is powering private markets. Listen here.

🎙 Hear Seyonne Kang, Partner and member of the private equity team at $134B AUM StepStone, discuss how the VC industry is dealing with today’s venture market. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, approaches alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Michael Rutter and Nick Owens for their contributions to the newsletter.