AGM Alts Weekly | 11.12.23

AGM Alts Weekly #27: Making private markets more public, every week.

👋 Hi, I’m Michael and welcome to my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in alts so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Good morning from Washington DC. I’ve just returned from a busy week in NYC where I moderated a panel on the VC market outlook for 2024 at SuperVenture with Rajeev Dham of Sapphire Ventures, Andras Forgacs of Starlight Ventures, and Thomas Schneider of Isomer Capital.

I’m about to head to Europe to speak on the topic of GP stakes at SuperInvestor in Zurich and meet with founders, VCs, and allocators in London and Berlin. If you’re in Zurich for SuperInvestor or in London and Berlin, please do reach out.

The topic on the menu for this week is how private equity continues to court the wealth channel — and what this means for the future of alternative asset managers and investors.

Allison McNeely, Dawn Lim, and Loukia Gyftopoulou of Bloomberg wrote a fantastic article, Private Equity Courts a Growing Class of Mini-Millionaires, earlier this week.

The Bloomberg story starts at upscale Greek restaurant Avra Estiatorio (one of my Midtown favorites and excellent food, btw), where Ares hosted an event designed to educate the HNW channel on why they should include alts in their portfolios. Props to Ares for a top-quartile restaurant choice.

The trend of private equity firms looking to raise capital from the high net worth channel marches on as firms look to grow their AUM.

Ares is far from the only firm looking to court the wealth channel with events and educational content. And for good reason.

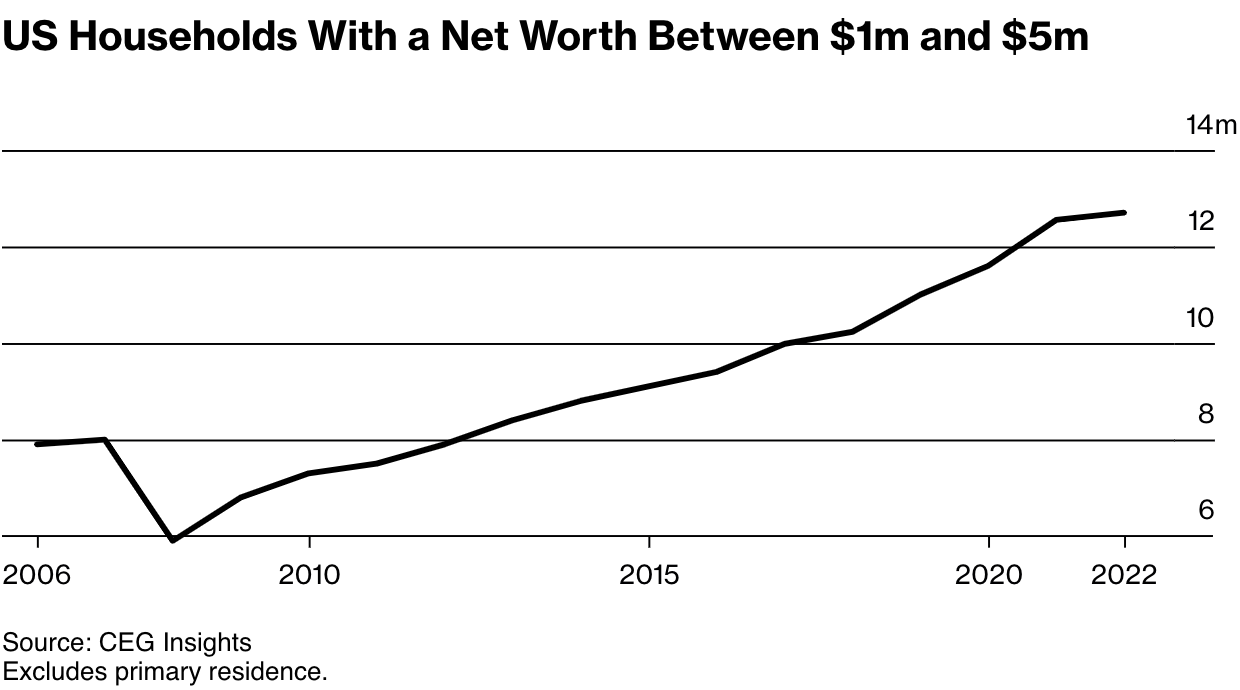

When it comes to private equity firms eyeing a growing population of wealthy individuals, the trend is their friend. The segment of US households with $1-5M of investable wealth jumped 60% to 12.7 million households in the 15 years to 2022, according to researcher CEG Insights.

This HNW cohort’s combined wealth is currently around $100T, representing a huge opportunity for private equity firms to grow AUM from a net new investor group. This segment, with $1-5M of investable assets, is severely underallocated to alternatives compared to institutional investors. According to a Bain analysis, HNW investors in this segment have only allocated about 1% of their net worth to private investments.

Firms across the industry are organizing conferences, events, educational opportunities, and steak dinners to boost their profile among individual investors.

Some, like Apollo and Blackstone, have created learning platforms — “Apollo Academy” and “Blackstone University'' — to educate advisors and HNW investors.

Wealth advisors have certainly been receiving plenty of attention. “Not a week goes by that we don’t hear a pitch from a major player,” said Jeff Nauta, Co-Founder of Henrickson Nauta Wealth Advisors in Michigan.

A slight increase in allocation from the HNW channel to alternatives means tens of billions more AUM for alternative investment providers.

It’s not, however, a trivial task to work with the wealth channel for a number of structural reasons. The Bloomberg article highlights how selling into the wealth channel can be very different than it is with institutional investors — sales cycles with the wealth channel can be less defined and more idiosyncratic than with the institutional investor channel, and individual’s need for liquidity, coupled by the fact that they are taxable investors, can make the illiquid nature of private equity more challenging from an investment planning standpoint of a number of years. HNW investors don’t always have the same institutional knowledge of alternative investments, and advisers say that at times they have to remind clients that private equity can lock up their money for years.

A number of firms are investing heavily in providing educational resources to the wealth channel in an effort to build long-term relationships with these investors. Many large firms believe that they can become the provider of choice for the wealth channel, which is reflected in how they are structuring their teams and investment strategies and funds to be productized for wealth. Raj Dhanda, Ares’ Global Head of Wealth Management, highlighted the importance of breadth and depth for an investment platform that’s looking to work with the wealth channel. “The winners are going to be the firms that can offer solutions across asset classes,” he said. “So they can be the most efficient and have the most investment integrity.”

A number of questions arise from this development.

For GPs, selling into the wealth channel must be a concerted effort and investment. The key? Education, education, education. This goes for both HNW individuals and their advisors. The sale is multi-layered — first educating potential investors on alternatives and the merits of private markets, then educating them on specific investment strategies, then on why their particular firm is the best way for clients to invest into alts. The time of the sales cycle is less defined than that of institutional investors, where investment committee processes are well-understood by GPs. It would appear that this investment of time, capital, and resources makes sense given how underallocated HNW individuals are to private markets and how much the wealth channel is growing in size and scale, particularly at the $1-5M net worth segment in the US.

But this commitment isn’t trivial for GPs. Firms need to have enough resources to both educate and sell into the wealth channel. Hiring in this space isn’t the most straightforward of processes. Finding distribution professionals who are both well-versed in the nuances of private markets and how alternatives products fit into a broader investment portfolio AND have deep relationships in the wealth channel is not an easy task.

Large firms, such as Blackstone, Apollo, Ares, KKR, Brookfield, Carlyle, BlackRock, et al. have the resources and ability to hire teams across product structuring, distribution, and operations that can solve for these challenges.

But what about firms that are slightly or much smaller in size than the largest players? How will they engage with the wealth channel? Clearly, these firms have an opportunity to work with HNW investors, but the question becomes how they do so.

There are also interesting questions for HNW individuals and wealth advisors allocating to private markets. Should they work with a number of firms, and considering working with smaller firms, some of whom may generate stronger returns in certain private markets strategies, or should they go to firms that provide a one-stop shop for alts so they can streamline their relationships, decision-making, and time spent evaluating different funds?

The answer from the GP perspective is clear. As Ares’ Raj Dhanda said, the largest firms will offer a one-stop shop solution for investors. While I’m not convinced that this is the best outcome for all investors, I do believe that this is likely how the alts space will evolve from a capital raising perspective, and it’s one reason why I think we’ll continue to see the big get bigger and private markets will start to look like the more traditional asset manager world, where investors can shop for everything across asset classes at the alts supermarket that is Blackstone or Apollo or Ares or KKR or Carlyle or Blue Owl, etc.

I want to be clear — I believe that while the largest firms aren’t necessarily the right fit for all investors, they will provide a number of products to investors that will be a good fit for many. The largest firms are also in the best position from a resources perspective to structure products for the HNW channel, particularly in the semi-liquid fund space, so they will become the default option for many who are looking for initial exposure to private markets — and that’s generally a positive development for private markets.

What I would be very excited to see are ways for the smaller funds to engage with the wealth channel even though they may not have the resources of the largest players. There are a number of technology and infrastructure platforms that are built to do this — and that will aid the continued evolution of private markets and enable investors to have more choice and agency over their allocation to different funds and strategies in private markets, which should only serve to make private markets more robust and advanced.

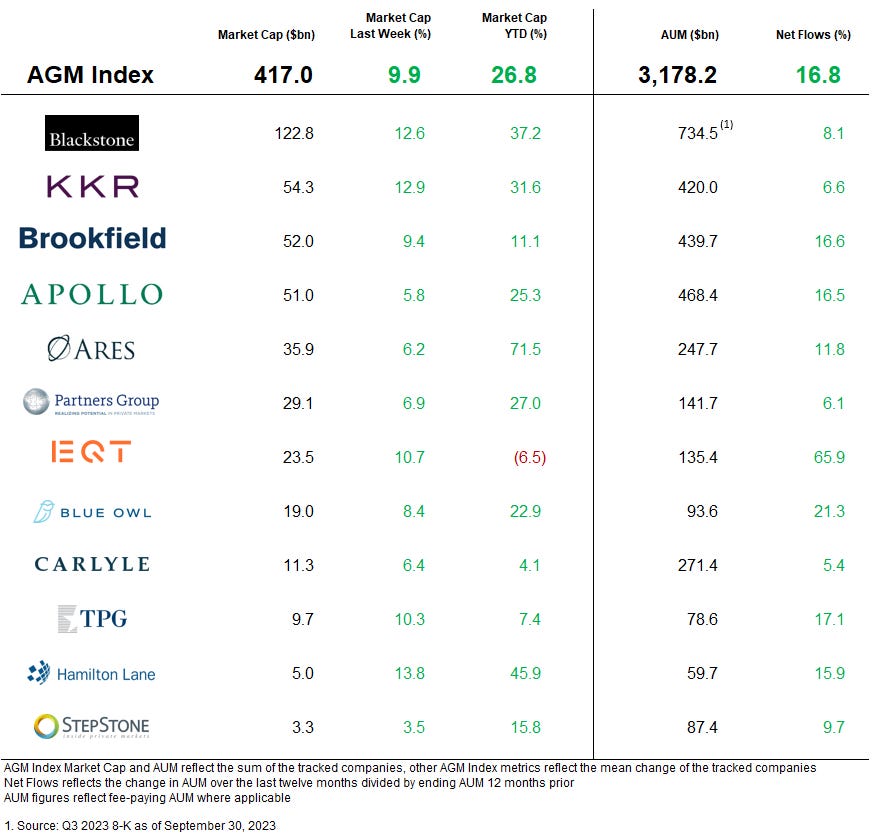

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

AGM News of the Week

Articles we are reading

📝 Exclusive: Prominent solo VC Elad Gil raises over $1B for third fund | Rosie Bradbury, PitchBook

💡One of the most closely watched and best-funded VC investors in Silicon Valley, Elad Gil, has secured over $1B for his third fund. Cosmic — Aleph 3 has received commitments of almost $1.1B from 54 investors, exceeding its $820M target. The new fund is 77% larger than its 2021 predecessor, which closed on $620M. Gil’s ability to secure new capital as quickly as he has is remarkable, given how severe the VC downturn has been in 2023 and the fact that he was still fundraising for his second vehicle in 2021. Solo VCs have risen to prominence in the past few years due to their ability to beat larger firms to lead hot deals. They’re able to move faster without traditional partnership structures and offer better terms and prices than competing investors. Harvard University’s endowment is amongst the institutional LPs in his fund and Gil says he’s invested in over 30 unicorns at the early stage. Among these are a seed investment in Pinterest and Series A stakes in AirBnB and Stripe. Crucially, Gil has had exits for his investors. He invested in the Series D round for Instacart, which listed publicly in September, and in Figma, which Adobe agreed to buy for $20B in September 2022. Though other prominent solo VCs have yet to raise new funds since the startup downturn began last year, they have generally punched above their weight class in the last few years. Some have led or co-led mega-rounds of $100M or more. Gil’s comments on his investment focus, which are published on his online blog, have included a growing interest in the scope of future applications for generative AI technology. In an interview with TechCrunch in May, Gil described the release of Chat GPT-3 as a "sea change" for generative AI technology. He suggested in a blog post in August that "we are in the (very) early days of AI," and that mass enterprise adoption of generative AI models remains far away. In March, he backed Character.ai, which develops an AI-powered chatbot, in a $150M round at a $1B valuation.

💸 AGM’s 2/20: The rise of the solo GP in venture, a VC fund managed by a single partner, appeared to lose steam over the past year. Before diving into this monster fundraise by solo GP Elad Gil, let’s dive into the history of the solo GP space. The solo GP movement, called out by VC Nikhil Basu Trivedi (who ended up launching his new fund, Footwork Ventures, with another Partner, Mike Smith), in 2020, appeared to be popular amongst LPs who were looking for exposure to a class of super angels who could eventually build larger fund franchises. The past 10-12 years of venture has been a case study in the rise of emerging managers, many of whom have turned successful angel investing track records into institutional VC funds backed by top LPs across endowments, pensions, family offices, and fund of funds. Notable examples of angels turned brand name and hard-to-access VC franchises include Chris Sacca (Lowercase and now Lowercarbon), Aydin Senkut (Felicis Ventures), Jeff Clavier (Uncork Capital), Mike Maples (Floodgate), Roger Ehrenberg (IA Ventures), Semil Shah (Haystack). Others, like Manu Kumar (K9) and Steve Anderson (Baseline), amongst others, have decided to stay solo. These initial success stories served as proof points for a new wave of solo GPs to gain credibility amongst the LP community. Solo VCs like Oren Zeev (Zeev Ventures), Lachy Groom, Josh Buckley (Buckley Ventures), Harry Stebbings (20VC) have all gone on to raise large, $100M+ AUM funds from institutional LPs. Some of these funds have gone on to raise large pools of capital and produce strong returns. But the past year, which has been a difficult fundraising environment for all funds, has hit the solo GP movement particularly hard. That’s why the news of Elad Gil, a respected operator and investor in Silicon Valley circles for a number of years, raising a $1B fund is massive news for the solo GP space. His new fund is 77% larger than his prior, $620M fund, raised in 2021.

There are a number of questions about the solo GP model. Can they compete with larger VC funds and platforms, many of whom have large teams to both source and help portfolio companies? Proponents of the solo GP movement point to the fact that team risk is the biggest risk, particularly for first or second-time funds. At times, LPs argue, discord or lack of alignment amongst partners, contributes to poor investments or firm blowups. Proponents would also point to the fact that brand often lies with the investor rather than the firm. Many founders want to work with a specific individual who has created a brand or a track record as a founder / operator or investor that enables the solo GP to win a deal. Solo GPs would also argue that they have the ability to make quick, decisive investment decisions devoid of the encumbrance of firm politics that can sometimes hamstring firms’ decision-making to the detriment of investment performance.

Thanks to investment infrastructure tools built by the likes of AngelList, Carta, bunch, and others, it’s never been easier for investors to launch and run a VC fund. Net-net, that’s a positive for GPs, LPs, and founders. Infrastructure should remove the barriers to launching a fund. It will enable an increasing number of talented investors or operators to be able to leverage their expertise, access, networks, communities, and skillsets to invest in companies. But, I do believe that the past few years of private markets excess took the solo GP movement too far. For some GPs and LPs, the solo GP movement meant running a fund on the side. Many founders and operators leveraged advancements in investment infrastructure to do a fund on the side of their main job. They sold their access and network as the ways that they would drive outsized returns. I believe that LPs are more attuned than they were over the past few years to the difficulties of running a fund and the level of professionalism that it takes to be a fund manager. Access alone will rarely carry the day for fund managers to generate successful returns. Thoughtful portfolio construction, the ability to manage a portfolio, and thinking through proper liquidity options at the right time all require full focus and knowledge.

Do I think that the solo GP movement won’t continue? No. Why? I view venture investing through the lens of the find-pick-win-help framework. If a solo GP, particularly at early-stage, can do any of these, particularly find and pick, in a uniquely advantaged way, then there’s no reason why they can’t succeed in the way that a fund with multiple partners can. The question LPs should be asking is what are they solving for when deciding to work with a solo GP fund, or any fund, for that matter. Is it access? Is it co-invests? It can be any or a number of different reasons. LPs just need to know what game they are playing — and it could be the solo GP game if that helps drive returns.

📝 The Deal Between CPP Investments and Ardian May Signal an Opening of the Secondary Market | Alicia McElhaney, Institutional Investor

💡Is the secondaries market beginning to show signs of life? Ardian’s recent acquisition of a $2.1B secondaries portfolio from CPP Investments indicates that the market for stakes in private equity funds could be heating up. “The market has definitely improved on multiple fronts in the last three to six months,” said Dushy Sivanithy, Head of Secondaries at CPP Investments. “The bid-ask spread in 2022 was very high, as a result, transaction volumes were very low. You’ve seen that narrow over the course of 2023. You’ve seen a material increase in sellers.” Analysis of the secondary market from Jefferies paints a similar picture: average pricing for transactions was 84% of the NAV of the fund, a 6% increase from the second half of 2022. At the same time, fundraising has increased dry powder to ~$220B.

Sivanithy and CPP Investments have watched the secondary market evolve over the past few months. CPP Investments oversees C$576B ($416.9B) in total capital, C$147.5B ($106.8B) of which is in private equity holdings. They have a secondaries team that is an active buyer in the market. CPP highlighted two recent acquisitions in their second quarter results: a purchase of a $100M commitment to Oak Hill Capital Partners V and a $50M investment in ServiceTitan via both equity financing and a secondary transaction. The firm is an active seller, too. Over the past five years, CPP Investments has signed seven secondary deals.

Sivanithy said that their activity in the secondary market helped them determine the right time to consummate this secondary sale with Ardian. “It allowed us to spot a good window to take a portfolio to the market for sale when we saw improving pricing,” he said. “There were a number of buyers that were keen to look at a portfolio at scale.” CPP Investments chose to take advantage of this opening and moved quickly, using the $2.1B sale as “a portfolio management tool … We’re trying to right-size certain exposures. It’s a chance to remove some legacy exposures,” Sivanithy said. Sivanithy expects the secondaries market to loosen up further in the months to come. More investors are coming to market now, particularly pension plans that have overallocated to private equity. They are now looking to offload some of their longest-held assets to free up liquidity for new allocations.

💸 AGM’s 2/20: Secondaries have been popular in fundraising over the past year as many investors view the current market as an opportunity to buy portfolios of assets or single assets from GPs and LPs who are looking for liquidity. That interest has driven a record amount of dry powder raised in the secondaries market over the past two years. But deals weren’t getting done in 2022 at both conpany and fund levels due to a wide bid-ask spread between buyer and seller. That’s begun to change in 2023 as spreads have tightened. The CPP $2.1B sale to Ardian could be a signal that the market is ready to transact. Certainly, many GPs and LPs are looking for liquidity, but there are questions as to whether or not it’s the right time in the cycle to transact or if spreads will continue to shrink as we enter 2024.

It will be interesting to watch the secondary market continue to unfold in the coming year amidst a backdrop of a turbulent geopolitical environment, a looming election year in the US, and the possibility of lower rates. Investors are seeking liquidity, but there’s also questions as to whether or not it would be counterproductive for investors to sell off positions at steeper discounts than they may receive in the next year or two. As a number of AGM podcast guests, including John Burbank and Ken Wallace of Nimble Partners and Jamie Rhode of Verdis, have highlighted — duration is one of the most important features investors can have in private markets. Certainly, there are times and cases where it makes sense for investors to look to the secondary market. But, in many cases, the inability to go long duration can negatively impact returns over the long run.

📝 Private equity fortunes diverge as KKR prospers while Carlyle cuts jobs | Antoine Gara, FT

💡Quarterly earnings calls for two of the world’s biggest private equity groups — KKR and Carlyle — paint the picture of firms heading in different directions. This week’s results underscored how the two firms, which were roughly the same size a decade ago, have had diverging paths. KKR has increased its fundraising expectations, while Carlyle’s underwhelming fundraising results this year are resulting in a cost-cutting effort. The FT reports that KKR is building its investment operations in infrastructure and property and plans to launch new flagship corporate buyout funds in the US and Asia. KKR also continues to do more deals, even with the rise in rates. Carlyle, however, noted that its fundraising results this year have not met expectations. Carlyle’s Chief Executive Officer Harvey Schwartz said that the firm is focused on reducing costs, adding “Overall, we have not been pleased with fundraising in 2023.” Carlyle raised $6.3B across their fund in the third quarter, an 11% decline from the quarter prior. It closed its most recent flagship buyout fund with $14.8B, 20% less than a predecessor fund and far smaller than the $27B former CEO Kewsong Lee had targeted before his sudden exit last year. By contrast, KKR increased its fundraising in Q3, raising more than $14B. The two firms have been on diverging paths, partly due to thoughtful succession planning by KKR and a challenging leadership transition at Carlyle. KKR has had no significant internal disputes since elevating Joseph Bae and Scott Nuttall as co-CEOs in October 2021, cementing a succession from founders Henry Kravis and George Roberts. Carlyle’s succession plan paints a different story — its three billionaire founders, David Rubenstein, William Conway and Daniel D’Aniello named Lee and Glenn Youngkin as co-heads in 2017, but Youngkin departed three years later amid conflict with Lee. Lee’s resignation last year left Carlyle without a permanent leader until it hired former Goldman Sachs executive Schwartz in February. “There is a lot of work to do,” said Schwartz, offering a pessimistic outlook for dealmaking activity. “[My] own opinion is that lower activity levels and reduced confidence will likely persist for a bit longer.” Carlyle has reduced expenses by cutting investment jobs in areas where it has struggled with fundraising or sees low growth prospects. It shut its US consumer, media, and retail private equity group in September, and has reduced its workforce across its US buyout investment team. The company reported a $40M drop in expenses on an annualized basis during the quarter, ~85% of which came from pay. Schwartz believes that Carlyle’s fundraising efforts would improve in the fourth quarter as it targeted buyouts in Japan and real estate, among other strategies. He has been focused on growing Carlyle’s credit and insurance-related investment assets, debt and equity underwriting operations, and funds designed for wealthy individuals. He said cost-cutting would not come at the expense of the group’s long-term growth. Carlyle’s earnings did beat analysts’ expectations, in large part due to falling expenses.

💸 AGM’s 2/20: As we discussed last week, fundraising results and fee-related earnings (FREs) will play a major role in driving stock performance for private equity behemoths. Carlyle’s fundraising results over the past year reflect a challenging fundraising environment, which has required them to cut costs and jobs in certain areas. This development brings up an interesting question for diversified alternative asset managers. A diversified, multi-strategy firm that can provide a number of different investment solutions to investors as a one-stop shop should, in theory, be able to weather various market environments and fundraising cycles. But what happens when a disappointing fundraising performance eats into a firm’s ability to manage expenses and drive fee-related revenues? Does a firm shrink its menu of strategies and funds to reduce expenses? Doing so makes a multi-strategy firm less diversified, which is supposed to be its selling point to both potential allocators and stockholders. That appears to be the choice Carlyle had to make. They shuttered their US consumer, media, and retail private equity group to reduce expenses while focusing on growth areas, such as funds for the wealth channel. I wouldn’t bet against Carlyle — or any of the larger alternative asset managers for that matter. They have the size, scale, and brand to continue to build out their respective platforms, and the wealth channel will play an important role in helping to grow many of these firms’ platforms.

(Some) fundraising news

📝 Focus Financial Partners, fintech founders invest in alts platform Arch | Andrew Foerch, Citywire

💡Arch, a fintech company that aggregates private investment data and documents for advisors and their clients, announced it has raised $20M in a Series A funding round. Venture capital firm Menlo Ventures led the round. Contributions from notable parties include those from Focus Financial Partners, Merchant Investment Management Chairs Mark Spilker and Scott Prince, Altruist Founder Jason Wenk, and Vanilla Founder and wealth management veteran Steve Lockshin. Citi Ventures, Carta Ventures, and Spilker- and Prince-backed GPS Investment Partners, as well as existing Arch backers, Craft Ventures and Quiet Capital participated as well.

💸 AGM’s 2/20: Data aggregation is a hair-on-fire problem in the alts space. The ability for advisors and investors to track and manage all of their private investments, including held-away assets, in one place enables investors to have more transparency into their holdings — and crucially, plan for future capital calls and liquidity needs. Firms like Arch or AltExchange that allow investors and advisors to turn data into action will be critical for taking alts to the next stage. Congrats Ryan and the Arch team on an important milestone for your business.

📝 Crowdcube doubles down on secondaries with Semper acquisition | Kai Nicol-Schwarz, Sifted

💡UK equity crowdfunding platform Crowdcube has acquired secondary markets investing platform Semper as it looks to add secondaries offerings to their investors. The deal will see Semper integrated into the Crowdcube brand and Semper founders Mathias Pastor and Balthazar de Lavergne will join Crowdcube to lead their secondary business. Since launching 2013, UK-based Crowdcube has run crowdfunding campaigns for the likes of Monzo, Revolut, and Qonto, and raised a total of £1B for more than 1,300 businesses. Semper counts Frst Capital, Kima Ventures, FJ Labs, and Nordstar amongst its investors, who all participated in a €3m seed round at the end of 2021.

💸 AGM’s 2/20: Crowdcube’s acquisition of Semper highlights a few trends in the alts space. One, secondaries are popular amongst investors, and not just institutional investors. Crowdcube will now have the ability to offer secondaries to its retail investor base. Over the past 18 months, Crowdcube has processed £20M in secondary share sales. Two, we are seeing crowdfunding platforms, particularly those in Europe, expand geographically. Given Semper’s French ties, this will further expand Crowdcube’s reach beyond the UK and into Europe at a time when EU regulation is favorable to equity crowdfunding platforms. With relatively new regulation enabling UK crowdfunding platforms to passport their services across Europe, the battle for the European crowdfunding crown wages on. Republic, which acquired Seedrs in December 2021, was recently granted a license under the new EU regulation for equity crowdfunding providers, meaning that the platform that has done over £2.6B in volume since 2012 can now offer investments across Europe to individual investors. Congrats to Mathias (an AGM podcast guest), Balthazar, and the team at Semper on your acquisition by Crowdcube.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 bunch (Private markets infrastructure investment platform & SPV infrastructure) - Head of Commercial. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - Midwest, Regional Director, Senior Vice President. Click here to learn more.

🔍 Republic (Multi-strategy alternative investment platform) - Chief Technology Officer. Click here to learn more.

🔍 Allocate (Private markets infrastructure investment platform) - Client Associate, Relationship Management (Remote). Click here to learn more.

🔍 Isomer Capital (European VC fund of funds) - Investor, Secondaries. Click here to learn more.

🔍 Northzone (Global early-stage VC) - Investment Team, Stockholm office. Click here to learn more.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

🎙 Hear Chase Griffin, a QB at UCLA and the NIL Male Athlete of the Year, share thoughts on how private equity and the NIL are changing the game for collegiate and professional sports. Listen here.

🎙 Hear Jamie Rhode, Principal at family office Verdis Investment Management, on how to drive the most meaningful returns in early-stage venture as a LP. Listen here.

🎙 Hear Maelle Gavet, CEO of Techstars, take the pulse of seed and how Techstars has created an actively-managed index of innovation. Listen here.

🎥 Watch a roundtable on the European institutional LP vantage point on the current fundraising environment for VCs in Europe. EUVC, a top podcast championing European venture and fund syndicate platform, brought together leading institutional LPs in the European ecosystem, David Dana, Head of VC Investments at EIF, Joe Schorge, Co-Founder & Managing Partner at Isomer Capital, Christian Roehle, Head of Investment Management at KfW Capital, and me to discuss how GPs in Europe can navigate a difficult fundraising environment. Watch here.

🎙 Hear Joe Schorge, Co-Founder & Managing Partner at one of Europe’s most active LPs, Isomer Capital, discuss why now is Europe’s time. Listen here.

🎥 Watch Marc Penkala, Co-Founder & Partner at Altitude, and I do a first-of-a-kind live podcast on EUVC. EUVC, the leading podcast championing European venture and fund syndicate platform, brought together one of their portfolio GPs, Marc Penkala of Altitude, and me for a VC / LP pitch session. Watch here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, and I take the pulse of private markets on the fourth episode of our monthly show, the Monthly Alts Pulse. Watch here.

🎙 Hear the incredible story of “tech’s most unlikely venture capitalist,” Pejman Nozad, Co-Founder & Founding Managing Partner of Pear VC, on how they’ve built a seed investing powerhouse. Listen here.

🎙 Hear sustainable investments pioneer Bill Orum, Partner of $9B AUM OCIO Capricorn Investment Group, discuss how Capricorn has proven that doing well and doing good don’t have to be mutually exclusive. Listen here.

🎙 Hear wealth management industry titan Haig Ariyan, CEO of Arax Investment Partners, share his thoughts on the private equity opportunity in wealth management and why the intersection of wealth and alts is one of the biggest trends in private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with a macro lens from John’s background as a leading macro hedge fund manager at Passport Capital and on micro VC from Ken’s background backing some of the top emerging VCs at Industry Ventures. Listen here.

🎙 Hear $40B AUM Cresset Co-Founder & Co-Chairman Avy Stein and Director of Private Capital Jordan Stein live from the Allocate Beyond Summit discuss how private markets are changing wealth management. Listen here.

📝 Read how 73 Strings CEO & Co-Founder Yann Magnan and team are leveraging AI to build a modern and holistic monitoring and valuation platform for private markets in The AGM Q&A. Read here.

🎙 Hear $18B AUM Savant Wealth’s award-winning CIO Phil Huber talk about how LPs can build a strategy for investing in private markets. Listen here.

🎙 Hear Avlok Kohli, AngelList’s CEO, talk about how they are building the company of companies that is powering private markets. Listen here.

🎙 Hear Seyonne Kang, Partner and member of the private equity team at $134B AUM StepStone, discuss how the VC industry is dealing with today’s venture market. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, approaches alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Michael Rutter and Nick Owens for their contributions to the newsletter.