AGM Alts Weekly | 1.21.24

AGM Alts Weekly | 1.21.24

AGM Alts Weekly #35: Making private markets more public, every week.

👋 Hi, I’m Michael. Welcome to my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in alts so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Good afternoon from London.

This week was about connecting the dots in alts. Across London and in Geneva for the Aperture alts event, I met and talked with founders and funders, fintechs and financiers, technologists and industry titans, operators and chief investment officers. They might all have different perspectives and vantage points, but much of what they said shared common threads.

Three key words emerged from conversations throughout the week:

Holistic.

Utility.

Standardization.

It feels like we are witnessing the rapid evolution of an industry before our eyes — and the landscape appears to be coming together. Technology innovation is developing at a pace where it’s starting to create step-function change in what can be done for GPs and LPs alike. Years of hard work by individual companies are coming to fruition, and their development is leading to collaboration that is breaking down siloes.

The industry’s largest firms, like BlackRock and Blackstone, amongst many others, have figured out how to bring together the best of “fin” and “tech” to use their size and scale to build (BlackRock’s Aladdin), invest (BlackRock and Blackstone’s investments in iCapital, 73 Strings, LemonEdge, Canoe), or acquire (BlackRock’s acquisitions of eFront and GIP) that connect the dots between AUM and technology — and everything in between.

The year of traditional in alternatives

At the Aperture event, I spoke about 2024 being the year of traditional in alternatives.

What do I mean by this?

Traditional assets within private markets — the likes of private equity, private credit, real estate, and venture capital — will feature. These traditional alternative assets will drive the increased inflows into alts. Traditional firms within alts — the Blackstones, BlackRocks, Apollos, KKRs, Carlyles, etc. — will continue to grow in size and scale. They will do so in large part because of the merging of traditional and progressive within private markets. New-fangled innovation with technology across the lifecycle of an alternative investment is enabling traditional alternative asset managers to grow. The willingness of many of these new innovative technology firms within private markets to accept and leverage the participation and partnership capabilities of traditional alternative asset managers will continue to be one of the defining features of private markets.

Some newsworthy events from this week highlight what’s to come for private markets:

Holistic: iCapital’s recently announced partnership with Morningstar that will enable the 170,000+ advisors who use Morningstar’s Advisor Workstation to access alternative investment research and tools to evaluate alternative investments alongside traditional investments via a holistic view of a portfolio. The concept of providing advisors and clients with a holistic view of their investment portfolios so that they can make better decisions on where and how to add alternatives into an entire portfolio has come to the forefront of discussions amongst GPs, LPs, and the technology platforms like iCapital that support the industry.

Both large alternative asset managers and wealth managers recognize that the industry has moved away from the conceptual framework of the 60/40 portfolio construction. Many alternative asset managers and wealth managers are now approaching portfolio construction and asset allocation in what I describe as buckets and spectrums rather than pieces of a pie (see last week’s newsletter for more on this topic). The equities bucket now includes public equity and private equity (or venture capital). Allocations to different strategies are thought about across the spectrum of liquidity and illiquidity. A partnership between the likes of iCapital and Morningstar should help to move the industry forward by providing advisors with the analytics toolkit and diverse spectrum of product access that will enable advisors and clients to have a holistic view of their investment portfolio.

Utility: The evolution of alts market structure appears to be mirroring that of market structure evolutions in other asset classes like public equities and fixed income. Tradeweb is a prime example of why the fixed income and derivatives markets required a multi-dealer, rather than single-dealer, solution to help push these markets forward. Industry participants were reticent to work with a single-dealer platform developed or backed by a single competitor. However, when a consortium of dealers came together to create a collective solution, it brought others to the table. It was the creation of an industry utility that involved the participation of many of the world’s largest dealers (banks) that helped create the success of what is now a $20B market cap company due to the standardization of certain tasks that a number of market participants can benefit from.

Private markets are undergoing a similar evolutionary arc. There are a lot of workflows and pools of data, particularly in the post-investment segment of private markets, that require standardization across the stakeholders within the industry. Rather than each firm endeavor to create their own solution to deal with these workflows, it makes sense for them to collaborate via partnership on a single, independent platform that’s at least partially owned by a number of industry stakeholders. The growing participation of private wealth has helped move the industry forward in this regard. A number of aspects of the workflows required to enable a wealth client to invest into an alternatives fund are better off standardized, such as KYC, investor reporting, the creation of feeder funds or other “roll-up” vehicles, amongst others. It’s no surprise that some of the most successful companies in private markets, like iCapital, have caught the eye of the industry’s largest stakeholders, who have decided to become a part of creating the utility and connective tissue in iCapital by investing or partnering. I anticipate that many of the industry’s largest companies and investment outcomes will be companies that find ways to partner with industry stakeholders as investors, just like Tradweb, Markit (now part of S&P Global), MarketAxess, and others did. Companies that create the connective tissue between industry participants will become incredibly valuable — and essential — companies for alts market infrastructure.

Standardization: One of the most exciting areas of alts market infrastructure is in the post-investment segment of the lifecycle of an investment. This area is one where data standardization can feature as a major leverage point that takes private markets to the next level. A number of companies focused on collecting and standardizing data are becoming increasingly important to both GPs and LPs. As I touched on above, it’s no surprise that many of the world’s largest alternative asset managers are investing in the likes of 73 Strings (Blackstone and Fidelity International), Canoe (Blackstone, Hamilton Lane, Carlyle, Fidelity), Chronograph (Carlyle), LemonEdge (Blackstone), and BlackRock acquiring eFront. These companies are but a few examples of the importance of extracting and analyzing private markets investment data so that both GPs and LPs can make better decisions. This week, Canoe announced a partnership with General Atlantic-backed fund administrator Gen II Fund Services, which has $1T of assets under administration. The work these firms are doing to create more transparency, efficiency, and standardization of investment data within private markets is something that many of these large GPs and LPs require if private markets is to continue to evolve.

A new chapter for private markets

The pace at which technology firms are partnering with the industry’s largest alternative asset managers or other major industry stakeholders across both traditional markets (like we just witnessed with iCapital and Morningstar’s partnership) or between alternatives firms (like we saw with BlackRock’s acquisition of eFront) appears to have reached a new level. There’s still plenty of work to be done and a number of critical solutions to be built that will push the market structure evolution within private markets further, but this week’s conversations left me with the impression that we’ve entered a new phase in private markets. The foundational infrastructure has been built. The rails have been laid. The spigot has been opened, particularly for the wealth channel.

2024 is shaping up to be the year where private markets enter a new chapter, and we’ll look back on 2024 as the year where private markets began to be viewed as mainstream and “traditional,” in large part due to the continued evolution of alts market infrastructure innovation and the merging of traditional private markets firms and progressive technology solutions.

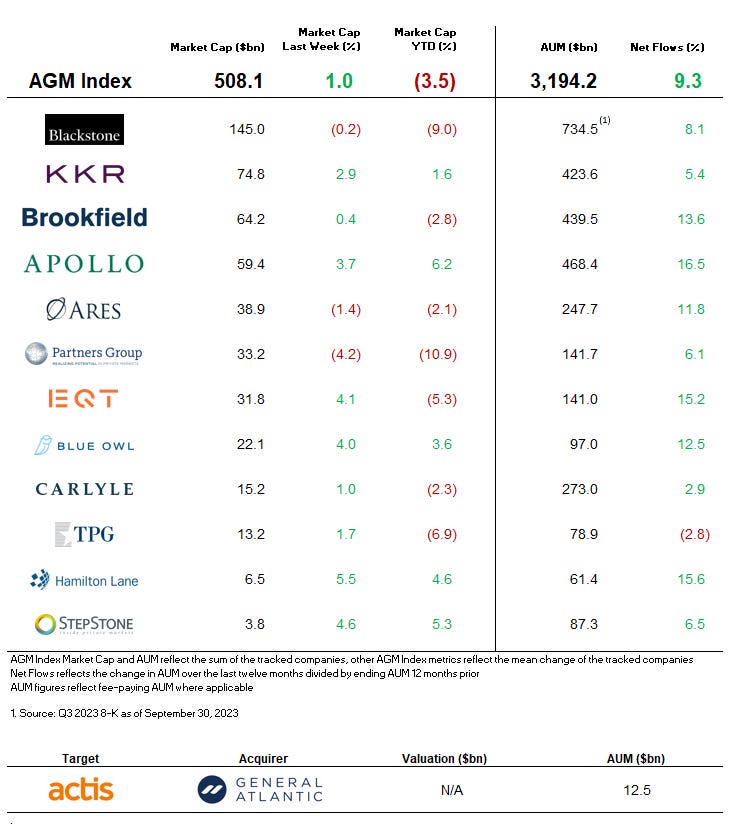

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

AGM News of the Week

Articles we are reading

📝 On BlackRock’s expansion into everything | Jessica Hamlin, PitchBook

💡PitchBook’s Jessica Hamlin delves into the details of why BlackRock isn’t the only asset manager who is expanding into everything. BlackRock’s recent $12.5B acquisition of Global Infrastructure Partners, a $100B AUM fund manager specializing in energy, transport, digital, water, and waste sectors, highlights the trend that asset managers are looking to expand horizontally across investment strategies and sectors. In September, CVC Capital Partners acquired infrastructure manager DIF Capital Partners, increasing its AUM to $192B. In December, Investcorp acquired Corsair Capital’s $4.8B infrastructure business. Hamlin asks the prescient question: why do asset managers want to scoop up infrastructure playbooks? The straightforward answer is one of returns. The strategy’s recent outperformance relative to other private market asset classes, particularly during periods of market volatility. At the end of 2022 and into the first quarter of 2023, real assets, Hamlin notes, generated stronger returns on average than PE, VC, real estate, private debt, funds-of-funds, or secondaries. According to PitchBook’s most recent Global Fund Performance Report, real assets was the only strategy that didn’t post a one-year horizon IRR that was lower than its five- or 10-year average in Q1 2023. Infrastructure also appears poised to be an investable opportunity due to two major forces impacting the economy over the next 20 years: the carbon transition and digital transformation. These changes will require the build-out of new infrastructure. Therefore, it hasn’t been surprising to see PE and infrastructure investments comprise around 90% of all M&A in the digital infrastructure segment. Hamlin also highlights that the asset management industry is witnessing a wave of consolidation as specialist managers face challenges competing for LP allocations versus one-stop shop multi-strategy asset managers.

💸 AGM’s 2/20: Hamlin highlights a number of trends that are defining the rapidly shifting landscape of private markets, notably, the focus that large, multi-strategy asset managers like BlackRock, General Atlantic, CVC, Investcorp, and others have on infrastructure. It’s no secret or surprise that infrastructure is at the forefront of investors’ minds, particularly as the world requires a rapid and expensive transition to decarbonization. There’s another important rationale here for why these managers are looking to expand across strategies: the quest to be a one-stop shop for private markets. The journey to becoming a multi-stage manager means growing AUM on the path to enhanced enterprise value creation and the higher valuation multiples afforded to multi-strategy managers. This trend is in part driven by the wealth channel, and private banks in particular. From an allocation perspective, it’s easier for private banks and the wealth channel to evaluate a firm or a brand and have a single-firm relationship across investment products than it is for wealth platforms — either private banks or large independent RIAs — to evaluate managers on a name-by-name basis. Managers who outperform will still continue to be of high interest to allocators, but it will be easier for many allocators to look at a platform that’s a one-stop shop and allocate across their different strategies where it fits into client portfolios. It was also not lost on me that a large number of private banks highlighted infrastructure as an attractive area of investment for HNWs in 2024. This should only serve to increase the interest from multi-strategy managers in infrastructure as they look to work with the wealth channel in a big way.

📝 PE Hub: Private Equity Will Separate Into Winners and Losers | Hartley Rogers, Hamilton Lane interviewed by Mary Kathleen Flynn, PE Hub

💡PE Hub’s Mary Kathleen Flynn interviewed Hamilton Lane’s Executive Co-Chairman Hartley Rogers in an illuminating interview that covered the merits of private equity and outperformance, exit strategies, and the outlook for deal activity in 2024.

Some quotes from Rogers stood out:

Rogers on private equity outperformance

Private equity has outperformed the public markets almost every year on a public market equivalence basis, and it also outperformed on a rolling 10-year basis much of the time.

We have data to show the public market equivalence performance of private equity compared to public market benchmark in each vintage year (private market metrics applied to public market) as well as time-weighted returns (public market metrics applied to private markets).

In brief, that data historically shows there is substantial outperformance of the private markets over time. During the dotcom and GFC eras, public market declines continued well past three quarters, and they have rebounded sharply over the last two quarters.

Rogers on when private equity outperformance occurs

This has more to do with the volatility in the public markets than the private markets themselves. When public markets are strong, private equity’s outperformance is lower. In any other environment, it’s higher. This is because private equity tends to be conservative in its valuation practices. If the public markets are going up, private market GPs don’t want to create false expectations – since what comes up can come down – so they want to make sure there’s conservatism and a cushion in what they’re presenting as valuations.

So, the data shows private market valuations don’t increase as quickly as public market valuations during those times. Conversely, private market valuations don’t come down as much as public market valuations when there’s a big falloff, as what happened in early 2022. When the Fed started raising interest rates, everybody was very focused on private market valuations and they didn’t go as fast or as far as the public markets.

Rogers on the outlook for deal activity

Stability and predictability are important for deal activity. We’re likely in for lower deal activity for another nine to 12 months because of this general instability. On the other hand, as time goes on, people will get used to the new normal in terms of pricing, and sellers will get comfortable with accepting values that are lower than what those businesses would have commanded years ago. So it’s really about getting used to the new normal.

💸 AGM’s 2/20: Rogers highlights a number of important features of private markets — outperformance relative to public markets over prolonged periods. When investors can go long duration, as Nimble & Passport Capital’s John Burbank said on an earlier Alt Goes Mainstream podcast, investors can benefit from the longer hold periods and reduction in volatility that private markets can provide. Sure, the devil is in the details — or the asset level allocation decision — but generally speaking, private markets benefit from both patience and time. Valuation practices and methodologies also provide private equity with the opportunity to limit precipitous drops (or increases) in value of private market holdings because valuations don’t change as often as they can in public markets. While there’s now more transparency and real-time data coming to valuation work in private markets thanks to technological innovation in the space, private markets will likely maintain a period of lag time that should help private markets investors stay patient. After all, illiquidity can, at times, be a feature rather than a bug.

📝 VCs need to start investing, says EIF boss | Zosia Wanat and Amy Lewin, Sifted

💡Sifted’s Zosia Wanat and Amy Lewin sat down with EIF’s Director of Equity Investment, Uli Grabenwarter, where he noted that many European VCs are sitting on dry powder and will need to start investing soon. Grabenwarter, who runs the biggest backer of European VCs in the EIF, believes that he expects more deals to get done in the second half of 2024. European startups raised €57.1B in 2023, a precipitous drop from the €105.1B raised in 2022, according to PitchBook data. The records of dry powder that VCs are sitting on will have to melt in 2024. Grabenwarter noted that “[funds] can only sit on raised funds for so long because … you need to show investors that you actually have investment activity going. And if you wait too long, you’re going to run against the investment period.” The EIF is a highly active LP in the European market. They allocate, on average €3B per year into the European venture market, contributing around 15-17% of the region’s total VC funding last year. Grabenwarter laid out the types of funds the EIF is looking for: “We have … significantly moved away from generalist, plain vanilla investment strategies and [are] focusing more and more on thematic, strategically oriented investment strategies that address policy objectives.” Sustainability and defense are at the top of the list for the EIF. The EIF has backed a number of climate tech funds, including a €50M commitment to World Fund, €50M to Circular Plastics’s fund, and €35M to Ocean 14. A sustainability focus appears to help funds if they are looking for funding from the EIF. Emerging managers have also been an area of focus for the EIF. Funds in their first three fund generations made up 56% of EIF’s top-performing funds last year — and Grabenwarter stated that his team constantly evaluates whether they are taking enough risk when it comes to backing emerging managers.

💸 AGM’s 2/20: Sifted’s interview with EIF chief Grabenwarter was illuminating on a number of levels. His comments highlight some of the issues and topics that are top of mind for LPs when evaluating or partnering with GPs. Grabenwarter’s comments on European VCs needing to deploy record amounts of dry powder bring into focus an inherent conflict as funds come closer to the end of their investment period. When GPs are sitting on dry powder and not deploying capital, LPs are being charged management fees for capital sitting idle if they are charged on committed rather than deployed capital, which puts a drag on IRR. However, if VCs decide to deploy as the clock runs out on the investment period, VCs may end up investing into less than ideal investments in an effort to deploy the capital before the investment period ends. The other challenge with large amounts of dry powder sitting on the sidelines means that, when investors decide to deploy, they may be fighting for allocations into the same companies, which could increase the entry price that VCs pay. It was interesting, but not surprising, to hear Grabenwarter say that emerging managers have been a major driver of outperformance for EIF. I’d expect this to continue as fund size in VC can often be a function of outperformance.

Reports we are reading

📝 Allocate’s 2024 VC Industry Outlook | Samir Kaji, Hana Yang, & ~100 fund managers & LPs, Allocate

💡Allocate published their 2024 VC Industry Outlook, polling nearly 100 fund managers and LPs to share their views on what they expect to see in 2024. There’s a fantastic set of predictions from a number of thoughtful industry practitioners and insiders.

A number of topics were canvassed, including:

Fundraising climate for VC funds.

Limited Partner trends.

Trends in AI.

Fundraising outlook for companies.

Markdowns and impact of a valuation reset.

Opportunities and reasons for optimism.

Early-stage trends.

M&A and IPO thoughts.

My thoughts centered around how the wealth channel will approach VC in 2024, which could shape up to be a strong vintage due to a number of market dynamics and industry forces.

2024 will be the year that the wealth channel allocates to venture capital in a meaningful way. While there is still more work to be done to educate the wealth channel about the merits of private markets, and venture in particular, the fact that 2024 is shaping up to be an attractive vintage from a valuation perspective coupled with the technology innovation from investment platforms such as Allocate that enable more investors to access alts will pave the way for more dollars to be allocated to venture. Similar to how the most well-known brands in private equity and private credit have been the biggest beneficiaries of the wealth channel's growing presence in private markets, the larger, brand name VC funds will benefit most from increased interest from this LP constituent.

Some other thoughts stood out:

Brett Wilson, General Partner at Swift Ventures

Venture capital and startup-building has been too loosey-goosey for too long. 2024 will see a return to good governance and accountability — funds and startups that don’t do what they say will struggle to raise capital.

Oren Zeev, Founding Partner at Zeev Ventures

During 2024 there will be an increasing number of “the emperor has no clothes” unicorns. Some of these unicorns will go out of business, others will have to reach profitability but without any meaningful growth or exit prospects will turn into zombies. This will not end in 2024 as I believe it will continue in 2025. At the same time, there will be some unicorns who will show real resilience and will grow into 2021 values.

Rick Zullo, Co-Founder & General Partner at Equal Ventures

I believe 2024 will be the year where firms with capital will see a sharp divergence away from those that don’t. While larger firms are chasing momentum rounds with valuations detached from fundamentals in AI, there will be a LOT of great companies with PMF, proven unit economics and strong growth, just not strong enough to get most of the multi-billion AUM funds excited. orat valuations that need to be reset. With reserves depleted for most insiders, outsiders will need to come in and find great companies at reasonable multiples that will likely drive some amazing long-term returns. For those with capital, this will be a great opportunity to gain greater share of a company at a reasonable price. Those who don’t could become victim to structured round dynamics that wipe out previously lofty mark-ups. With several prominent unicorns crashing down to earth, emerging managers that were riliant on some of these later stage companies to drive their fund multiples are likely to see those returns deflate and might see it become even more difficult to raise LP capital.

Chris Douvos, Managing Director at Ahoy Capital

Amid a tepid exit market and a punishing fundraising environment for both companies and GPs, partnerships will start to feel stress and at least one well-known firm will suffer a public breakup while many others will be beset by the quiet quitting / retiring on the job / calling in rich of senior partners.

Ed Sim, Founder & Managing Partner at Boldstart

We have a bubble in Inception Rounds as every investor no matter how big or small continues the chase to fund two founders and an idea with unlimited check sizes — this will not end well as you can surmise. I predict by YE multi-stage firms (>$1B funds) who are responsible for driving up round sizes and pricing finally pull back as they recognize that it’s F&^%$8ing hard to invest at inception. Expect the pullback to start second half of 2024 and expect to see median cash raised and valuation for these rounds to finally stabilize in 2024 vs. increasing from 2023. For other rounds, expect a slight recovery in pricing from 2023 lows and an even larger one if Jerome Powell reduces interest rates.

Tomasz Tunguz, General Partner at Theory Ventures

Companies & startups in particular begin to report meaningful improvements in productivity from AI, reducing their headcount growth, but growing revenue just as much as projected. ARR per employee increases 10%, twice the decade long average.

Michael Kim, Founder at Cendana Capital

In 2024, active LPs investing in Seed funds will focus more on Pre-Seed funds — Pre-Seed is the new Seed. Also, as Institutional LPs review their commitments to the large platform VC firms, they will realize that the early stage VC exposure is a lot less than what they expected, given how these platform VC firms typically allocate between their earlier and later stage funds. I think institutional LPs will seek new relationships to increase early stage VC exposure.

John Avirett, Partner at StepStone

In 2024 I expect to see more consolidation with an accelerated number of private-to-private mergers of VC-backed companies.

Adam Draper, Founder & Managing Director, Boost VC

Great year for value creation. Slow year for value capture. VR will be hot.

Chad Byers, Co-Founder & General Partner at Susa Ventures

2024 is the year that Capital Light startups become an entire movement. It’s the space between a bootstrapped company ($0 raised) and a ‘capital factory’ company ($10s/$100s of millions raised). A Capital Light startup consumes sub $10M in VC dollars to get off the ground, and then grows as sustainably as possible. More founders will choose this path and investors will be excited to back them. Returns over the next decade will come from moonshots that require huge amounts of capital, but produce big enough outcomes to justify it, and Capital Light companies that can generate great multiples on invested capital with sub-IPO outcomes.

You can find the entirety of the 2024 predictions from participants in this link here.

Videos we are watching

🎥 Peak private markets? | William Ford (General Atlantic), Blythe Masters (Motive Partners), Jo Taylor (Ontario Teachers’ Pension Plan), Nicolas Aguzin (Hong Kong Exchanges & Clearing), moderated by Bloomberg’s Jonathan Ferro at World Economic Forum

💡A number of leaders across private markets and financial services came together at the World Economic Forum to discuss the continued transformation in private markets. Or, as panelist Blythe Masters of Motive Partners said on stage, private markets are in the midst of an “evolution of product, policy, and providers.” Private markets have expanded remarkably in recent years, growing from $4.5T of AUM in 2015 to over $13.4T in 2022. The panel, which included the interesting vantage points of one of the world’s largest asset allocators (Ontario Teachers’), one of the industry’s alternative asset managers (General Atlantic), one of the more active VC / PE funds in private markets (Motive Partners), and one of the world’s biggest exchanges (Hong Kong Exchanges & Clearing) shared insightful commentary about how private markets will continue to evolve, with policy and product innovation featuring in their thoughts.

A few comments and themes stood out:

General Atlantic’s Bill Ford noted the outperformance of private markets relative to public markets as a major driver for why many investors have focused on alternatives. He also noted that the wealth channel has grown to 15% of their $96B AUM, highlighting that portfolios are 60/40 no longer, in large part because rates were so low for a prolonged period. Ford also acknowledged the growing importance of decarbonization, particularly in the “Global South,” which was a significant driver behind their recent acquisition of $12.5B AUM Actis, which has a big presence in emerging markets with their infrastructure and climate-focused investments.

Motive’s Blythe Masters shared a balanced perspective on why and how the retail / wealth channel should have access to private markets and why policy needs to continue to evolve to unlock private markets to individuals, citing the potential positive impact of alternatives on a portfolio for the individual investor and saver but also stressing that it would be dangerous to “unconditionally open up private markets” without any regulation. Masters also made a very interesting point about what could come next for private markets: the Amazon of private markets, the fully end-to-end e-commerce and logistics experience equivalent for alts, has yet to be built in its entirety.

OTPP’s Jo Taylor noted how they have built out a deep, experienced team that invests 80% of their capital themselves rather than through managers, which is an increasingly common trend amongst the largest and most sophisticated pension plans and sovereign wealth funds. He also said they are being thoughtful about their allocation to private equity, highlighting that returns have come down from where they were in the past.

Hong Kong Exchanges & Clearing’s Nicolas Aguzin acknowledged that public markets certainly face a different reality as private markets continue to grow, but also that there’s a merging of public and private markets. HKEX, as well as other exchanges, are all looking for ways to work more closely with private companies, which Aguzin noted as being an important area of focus for them.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know, and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Apollo (Alternative asset manager) - Distribution & Wealth Services Associate. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - Alternative Investment Fund Origination - Vice President / Senior Vice President. Click here to learn more.

🔍 Vega (Digital wealth manager with a focus on alternative investments) - Senior Software Engineer (Backend / Frontend). Click here to learn more.

🔍 Isomer Capital (European VC fund of funds) - Investor, Secondaries. Click here to learn more.

🔍 Northzone (Global early-stage VC) - Investment Team, Stockholm office. Click here to learn more.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

🎙 Hear Fred Destin, the founder of Stride VC, discuss how to build trust in a competitive, chaotic world. Listen here.

🎙 Hear why Chris Douvos, the founder of Ahoy Capital, believes there’s always room for a Bugatti in a market full of Fords and Toyotas as he dives into the micro and emerging VC landscape. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, and I take the pulse of private markets on the sixth episode of our monthly show, the Monthly Alts Pulse. We discuss what will make the industry move forward in 2024. Watch here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, and I take the pulse of private markets on the fifth episode of our monthly show, the Monthly Alts Pulse. We discuss the rising interest of alts around the world. Watch here.

🎙 Hear how Shannon Saccocia, the CIO of $67B AUM Neuberger Berman Private Wealth, thinks about the changing role of alternatives in client portfolios. Listen here.

🎥 Watch the replay of the fireside chat at Future Proof decoding the rise of alts with some of the most influential players in private markets: Stephanie Drescher, Partner, Chief Client & Product Development Officer, and member of the Leadership Team at Apollo, and Shannon Saccocia, the CIO at Neuberger Berman Private Wealth. Watch here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear Chase Griffin, a QB at UCLA and the NIL Male Athlete of the Year, share thoughts on how private equity and the NIL are changing the game for collegiate and professional sports. Listen here.

🎙 Hear Jamie Rhode, Principal at family office Verdis Investment Management, on how to drive the most meaningful returns in early-stage venture as a LP. Listen here.

🎙 Hear Maelle Gavet, CEO of Techstars, take the pulse of seed and how Techstars has created an actively-managed index of innovation. Listen here.

🎥 Watch a roundtable on the European institutional LP vantage point on the current fundraising environment for VCs in Europe. EUVC, a top podcast championing European venture and fund syndicate platform, brought together leading institutional LPs in the European ecosystem, David Dana, Head of VC Investments at EIF, Joe Schorge, Co-Founder & Managing Partner at Isomer Capital, Christian Roehle, Head of Investment Management at KfW Capital, and me to discuss how GPs in Europe can navigate a difficult fundraising environment. Watch here.

🎙 Hear Joe Schorge, Co-Founder & Managing Partner at one of Europe’s most active LPs, Isomer Capital, discuss why now is Europe’s time. Listen here.

🎥 Watch Marc Penkala, Co-Founder & Partner at Altitude, and I do a first-of-a-kind live podcast on EUVC. EUVC, the leading podcast championing European venture and fund syndicate platform, brought together one of their portfolio GPs, Marc Penkala of Altitude, and me for a VC / LP pitch session. Watch here.

🎙 Hear the incredible story of “tech’s most unlikely venture capitalist,” Pejman Nozad, Co-Founder & Founding Managing Partner of Pear VC, on how they’ve built a seed investing powerhouse. Listen here.

🎙 Hear sustainable investments pioneer Bill Orum, Partner of $9B AUM OCIO Capricorn Investment Group, discuss how Capricorn has proven that doing well and doing good doesn’t have to be mutually exclusive. Listen here.

🎙 Hear wealth management industry titan Haig Ariyan, CEO of Arax Investment Partners, share his thoughts on the private equity opportunity in wealth management and why the intersection of wealth and alts is one of the biggest trends in private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with a macro lens from John’s background as a leading macro hedge fund manager at Passport Capital and on micro VC from Ken’s background backing some of the top emerging VCs at Industry Ventures. Listen here.

🎙 Hear $40B AUM Cresset Co-Founder & Co-Chairman Avy Stein and Director of Private Capital Jordan Stein live from the Allocate Beyond Summit discuss how private markets are changing wealth management. Listen here.

📝 Read how 73 Strings CEO & Co-Founder Yann Magnan and team are leveraging AI to build a modern and holistic monitoring and valuation platform for private markets in The AGM Q&A. Read here.

🎙 Hear Bain & Company’s Partner & Chairman of EMEA Private Equity Graham Elton discuss the evolution of private equity and how large private equity firms have evolved as businesses. Listen here.

🎙 Hear $18B AUM Savant Wealth’s award-winning CIO Phil Huber talk about how LPs can build a strategy for investing in private markets. Listen here.

🎙 Hear Avlok Kohli, AngelList’s CEO, talk about how they are building the company of companies that is powering private markets. Listen here.

🎙 Hear Seyonne Kang, Partner and member of the private equity team at $134B AUM StepStone, discuss how the VC industry is dealing with today’s venture market. Listen here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, discusses how they approach alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Michael Rutter and Nick Owens for their contributions to the newsletter.

Thanks for your newsletter! it’s financial inspiring, insightful, educational! can I talk about it on my Linkedin?