AGM Alts Weekly | 11.16.25: Know thy moat

AGM Alts Weekly #129: Making private markets more public, every week.

“Alt Goes Mainstream is category of one.” Global Head of Marketing & Communications, $X00B AUM alternative asset manager.

“When it comes to the intersection of alternative investments and wealth management, Michael just gets it.” CIO, $18B AUM RIA.

Presented by

Opportunities in Asset-Based Lending

Asset-based lending is one of private credit’s most dynamic growth areas, providing exposure to tangible assets and consistent cash flows across real estate, equipment finance, and consumer & SME lending.

By financing the businesses and assets that support the real economy, collateral-backed strategies can help investors pursue yield, diversification, and resilience amid shifting market conditions.

Good morning from Washington, D.C.

Moats are far from a new topic in business.

They have been studied at length.

They have been analyzed by many, including by some of the foremost experts in investing and behavioral finance such as Head of Consilient Research at Morgan Stanley Investment Management’s Counterpoint Global, Michael Mauboussin, as he did in this 2024 paper.

They have been used as a framework for investing by the world’s legendary investors, like Warren Buffett, who said of moats: “We think of every business as an economic castle. And castles are subject to marauders. And in capitalism, with any castle . . . you have to expect . . . that millions of people out there . . . are thinking about ways to take your castle away. Then the question is, “What kind of moat do you have around that castle that protects it?”

Morningstar even has an “Economic Moat Rating” that its research team awards to companies to assess its durable competitive advantage and “predict its ability to fend off competitors and generate high returns over time.”

Morningstar identifies five key features of moats:

Switching costs are obstacles that keep customers from changing between products, like from one company’s product to a competitor’s.

Network effects occur when the value of a good or service increases for both new and existing users as more people use it.

Intangible assets are things such as patents, government licenses, and brand identity that keep a company ahead and competitors at bay.

A company with a cost advantage can produce goods or services at a lower cost, allowing it to undercut its competitors or achieve higher profitability.

Efficient scale benefits companies operating in a market that only supports one or a few competitors, limiting rivalry.

The topic of moats seemed to come up in conversations and presentations all week.

Building “economic castles” on the ground and in the sky

Speaking of castles, to one of the private markets industry’s leading investors, perhaps moats can be seen through the lens of “sovereignty and dominion.”

Vista Equity Partners Founder, Chairman, and CEO Robert F. Smith discussed on a recent Alt Goes Mainstream podcast the importance of an enterprise software company having “sovereignty and dominion over workflows and datasets.”

Without that “sovereignty and dominion over workflows and datasets,” Smith said that an enterprise software company “doesn’t have a right to exist.”

Smith went on to dissect why “sovereignty” and “dominion” are critical to a company’s success.

Enterprise software companies can certainly possess moats, particularly if they provide essential workflows for the companies they serve. These workflows can, at times, become so mission-critical to a company that the switching costs become too high for the company to consider, which can create a meaningful competitive advantage.

It’s not just enterprise software where investors see moats as their castles in the sky (or cloud, if you’re an enterprise software investor).

Stonepeak Chairman, CEO, and Co-Founder Mike Dorrell discussed on a recent Alt Goes Mainstream podcast why infrastructure assets possess “huge economic moats.”

Dorrell said that the “essentiality and natural monopoly characteristics” of infrastructure assets means that they can often exert pricing power.

When discussing the characteristics of infrastructure assets, Dorrell noted that two of Warren Buffett’s biggest holdings are infrastructure assets:

Dorrell: And I often like to cite the example that if you look at Buffett’s portfolio, his two biggest holdings are infrastructure assets. I think his biggest holding is BNSF Railways and his second biggest holding is his utility company. I think he calls it Berkshire Energy. He owns mostly electric utilities all around the US. And what he looks for in his assets, [he] is very open about this. He wants a big economic moat around his businesses. Coca-Cola, through its brand, provides a big economic moat. Apple iPhones through, I guess its brand or its superior tech, but I think moreso its brand, provides a huge economic moat. And so infrastructure, not through branding, but through its own essentiality and its natural monopoly type characteristics, they have huge economic moats around these businesses and, I think, because of that, these pension funds have just had good experiences with them.

There’s a predictability and a reliability to the cash flows that is higher than I’d call a typically competitive business. Now, because of that, you’ve got to pay a higher price for them. There’s a trade-off … there’s nothing free in life. And so we’re not getting the 20-25% returns that private equity is seeking. But there’s something about an asset that maybe delivers a 13% return, but delivers it year in, year out for a long, long, long time.

And, back to Buffet, one of his most famous investments would be his Coca-Cola investment. He put something like $1.3 billion into Coca-Cola back in 1989 or 1990 or something like that. And, between $10 billion worth of dividends and the share price today, which is $25 billion worth of share price value, he’s returned $35 billion on that initial $1.3 billion investment. Sounds amazing. It is amazing. But his actual annualized return on that is about 13%. It’s just gone over a long, long, long, long time. And so I think that the institutional market likes the fact that they can have this reliable returning asset class that will go for a long, long, long time. The most similar thing I can think of is perhaps a long-term bond, but the issue with a long-term bond is that by 30-year bond, particularly the interest rates that we’ve been at, historically, the last decade, you worry a lot about inflation because for obvious reasons, inflation is going to erode away the real value of your long-term bond. So the fact that infrastructure is often very well correlated or passes through inflation, you actually get this long-term compounding, but you’re doing that long-term compounding in real terms. You’re protecting yourself against the impacts of inflation. That’s a pretty unique set of characteristics.

“It’s a love story, baby, just say, ‘Yes’” (Taylor Swift)

Another feature of moats that Dorrell references? Brand.

Brand has been top of mind for many alternative asset managers. And for good reason.

As alts continue to go mainstream and open up access to more investors, brand is an increasingly important feature for alternative asset managers themselves to possess.

As I wrote in the AGM Alts Weekly 6.1.25: Brand Equity, alternative asset managers are not just thinking about the moats of the businesses they invest in, but about the moats of their very own business:

Core to the question of the business evolution of alternative asset managers is who do they want to be as a business. As these firms look to work with the wealth channel that question has also become “what brand do they want to be?”

In this new era of private markets, many firms have taken a maniacal focus to their brand — and brand building — in this new era of private markets, as I discussed in the 8.25.24 AGM Alts Weekly on the topic of “build [brand] with Blackstone.”

Brand equity is one of the most valuable moats that an alternative asset manager can possess.

Trust and credibility are core to an LP, whether institutional or individual, deciding to invest with an alternative asset manager in what will amount to a multi-year, and often, multi-decade partnership.

As the wealth channel comes into focus for many of the industry’s largest investment platforms, a focus on building a brand that resonates with the consumer is critical.

Consumer brands can capture culture.

And capturing culture results in brand equity that can be hard to replicate, just as the iconic Jordan Brand Jumpman logo has done for PSG, the French soccer club.

This sentiment shift in how alternative asset managers market their own brand can perhaps help to explain why Blackstone President & COO Jon Gray is working to “put a little bit of a human face to finance,” as a recent Bloomberg article highlights or why the likes of Blackstone and Apollo have created holiday videos, as I wrote about in the 12.17.23 AGM Alts Weekly:

But taking a step back, Blackstone and Apollo are trying to humanize private markets in their own distinct ways. Why? Because both Blackstone and Apollo have a deep understanding that a meaningful portion of the next wave of growth for their respective firms comes from the wealth channel, where the end client is the individual investor. Blackstone and Apollo are not B2C companies, but they do own many companies that sell directly to consumers, and they certainly know that their end customer in the wealth channel is the individual consumer.

As Gray noted in this past week’s Bloomberg article, Blackstone is looking to some of the world’s most well-recognized brands for inspiration — and for how to create consumer love:

But for Gray, the vision runs deeper than any one market. When discussing Blackstone’s evolution, he invokes some of the country’s most renowned household names. Walmart. Amazon. McDonald’s.

“It’s no different from the example of Walmart or Amazon or any successful company in any business,” Gray, 55, said from the firm’s Manhattan headquarters. “They serve one market and they say, ‘Hey, people like it, how can I do it for more?’”

Know thyself

As alternative asset managers market to more investors, they are more frequently having to answer the question “who are you?”

That certainly can help to explain why alternative asset managers are making such a concerted effort to help the wealth advisor and individual investor know who they are — in and outside of the office.

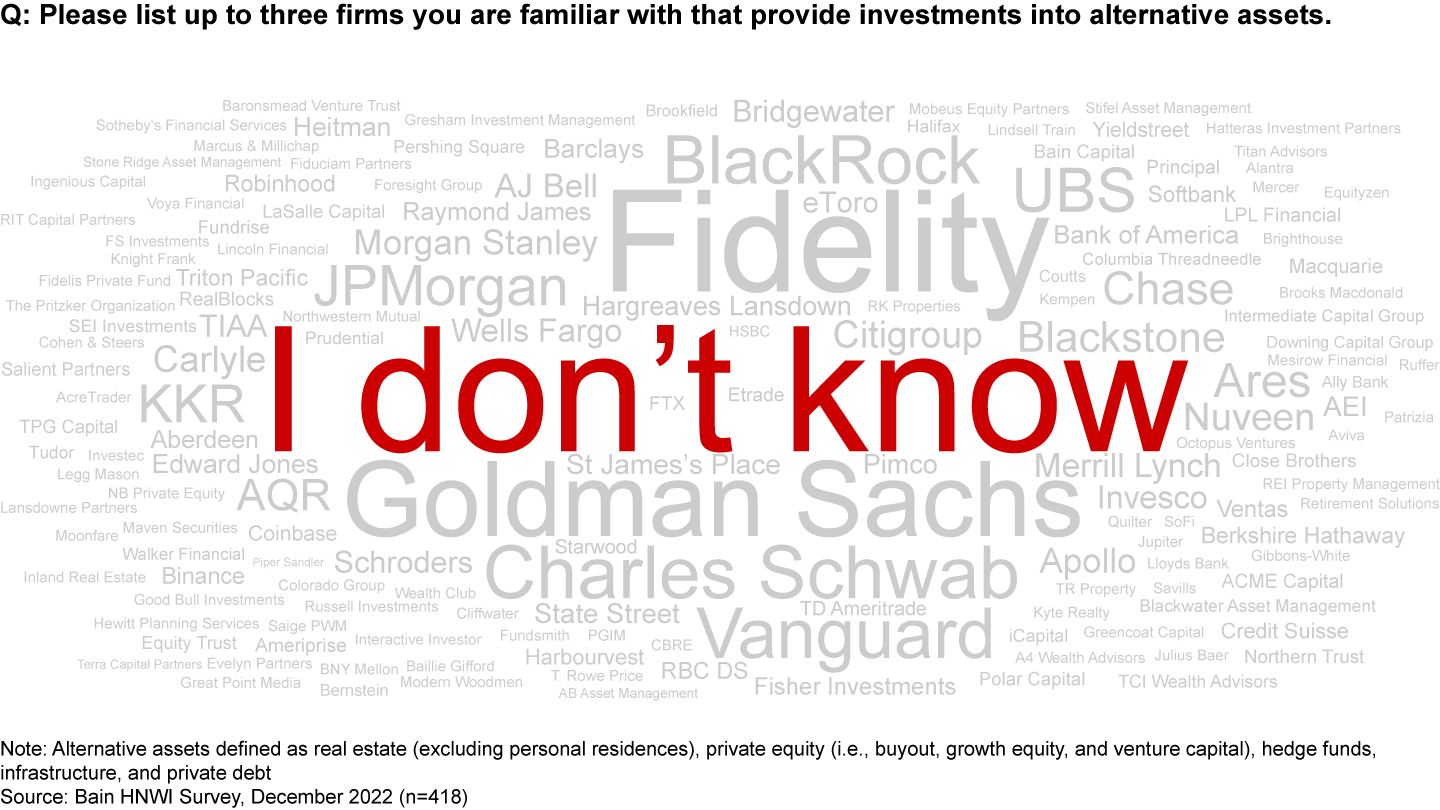

As I wrote in the 2.9.25 AGM Alts Weekly: “I don’t know,” many investors don’t yet know who does what in private markets.

Sharing a seminal picture from a 2022 Bain & Company survey that has surely been seared into the minds of CMOs across the asset management, I wrote:

If there’s a picture that’s worth a thousand words about just how early the wealth channel is in its adoption of private markets, this one is it. The opportunity to create a brand — or enhance an established brand, particularly for traditional asset managers — is there for the taking.

But building a brand in private markets doesn’t just require an understanding of how to answer the question “who are you” to prospective LPs.

Building a brand also requires asset managers to look inward and ask themselves who they are.

As I wrote in the 6.22.25 AGM Alts Weekly, the firms that know who they are will know who to be.

Hg Senior Partner and Executive Chairman Nic Humphries articulated this point well in a recent Alt Goes Mainstream podcast:

Humphries: It’s Patek Philippe. It’s Ferrari. It’s Hermes. In each of those industries, there are plenty of people who make cars that have a lot more capital than Ferrari. There are plenty of people who make watches that have a lot more capital than Patek Philippe. Plenty of people that make handbags that have a lot more capital and other things than Hermes.

And what those firms have done is chosen to specialize and to be super, super, super highly skilled at the things they chose to do — and to do that on a global branded scale. They are not just selling Ferraris in Italy. They sell Ferraris globally. They sell Hermes handbags globally. So they’ve chosen to be global scale businesses but doing a small number of things incredibly well.

And that’s exactly what we’re doing. We’re not just in investing. We’re in tech investing. We’re not just in tech investing. We’re in software investing. We’re not just in software investing. We’re in B2B back office software investing. We’re not just in B2B back office software investing. We’re in B2B back office software investing that is SaaS, that is going to generative AI, and in due course is only going to be focused on five or six or seven core clusters. So even within this thing called software, we’re already in a segment of a segment. That segment, by the way, is hundreds of billions. So we can still build a very scaled business globally by being in that one segment.

Humphries’ explanation of Hg’s business offers an example of a firm that knows exactly who they are.

From funds to firms … to moats

But the evolution of alternative asset managers going from funds to firms raises a number of questions about the future of their respective businesses.

Brand

How can brand continue to be a moat as the industry moves to become more inclusive to more investors?

For the majority of the industry’s history, private markets was the domain of institutional investors. The scarcity value and hard-to-access nature of private markets did come with a benefit from a brand perspective: the scarcity of the category gave it a luxury image.

How can alternative asset managers continue to preserve its scarcity factor and luxury image with institutional investors and UHNW investors while simultaneously opening up access to more investors?

Switching costs

The very structure of private markets funds creates high switching costs. Drawdown funds in many strategies and asset classes are 7- to 12-year relationships due to the closed-end structures of these funds. That creates a high switching cost for investors looking to get their capital back before the conclusion of the fund’s life.

Furthermore, LP relationships tend to be quite sticky. When managers have performed well for their LPs, those LPs tend to continue to entrust them with capital across multiple fund vintages, often creating multi-decade relationships.

With the advent of evergreen funds — and a growing secondaries market — do switching costs become lower? While evergreen funds are not as liquid as they might appear, they aren’t necessarily a 10-year fund commitment either.

Perhaps evergreen funds, despite their structural ability for investors to redeem portions of their investment, will be very sticky pools of capital for asset managers. And perhaps switching costs will be higher the greater the NAV growth, which will render brand-building even more important because wealth channel investors might invest in less funds, not more funds.

So how will alternative asset managers approach switching costs associated with their business?

Many of the industry’s largest firms are making permanent or perpetual capital a major focus of their activities. For firms that can enter into the 401(k) space, that could offer quite long-dated relationships with investors.

Some firms, such as Apollo and KKR, have focused on expanding their footprint in insurance by owning life insurance companies. Others have continued to grow their BDC and evergreen capabilities.

KKR has built out its balance sheet, ramping up its investments into a newly created Strategic Holdings unit that KKR Co-CEO Joe Bae has described as a Berkshire Hathaway-like vehicle: “What we’re trying to build in Strategic Holdings is in some ways a mini Berkshire Hathaway.”

Cost advantage

As Morningstar describes above, a company with a cost advantage can offer goods or services at a lower cost.

Will an alternative asset manager, or, more likely, a traditional asset manager aim to price its products lower than other competitors to take market share?

Historically, private markets products have tended to possess higher fees than traditional asset management products. This feature has tended to be the case with evergreen structures, in addition to drawdown closed-end funds. Will this phenomenon persist, or will fee compression take hold in private markets as it has done in public markets?

Without naming names, is private markets about to undergo a wave of “Vanguardization?”

Scale

Scale matters in virtually every industry. Alternative asset management is no exception.

Blackstone is the poster child for scale being a competitive advantage, so much so that Morningstar considers it to be a “wide moat company” (Morningstar describes a “wide moat company” as a company where they expect the competitive advantage to last more than 20 years).

Blackstone was right to bet on scale. Former Blackstone CFO Laurence Tosi noted in an Alt Goes Mainstream podcast a few years ago, when recounting a quote from Co-Founder and CEO Steve Schwarzman, that Schwarzman said “scale is [our] niche.” Tosi went on to share that Schwarzman also said that “the golden rule [of] the more scale that we had, the more resources we would have at Blackstone to invest in creating alpha.”

Thus far, scale has proven to be a major moat in private markets. This moat should continue to persist — and likely widen — as firms look to grow their brand and presence within the wealth channel. Building a business suited for the wealth channel requires scale across a number of vectors: a big enough balance sheet to invest in the products and invest in the team, the ability to properly invest in and staff up a team that can cover the wealth channel from pre- to post-investment, and the ability (and desire) to spend on marketing to build a brand.

These features of scale don’t mean that specialists can’t win. Hg’s Nic Humphries clearly outlines where and how a firm like Hg, a scaled specialist in software, operates in a large enough market to have the right to win as a specialist. But specialists must be very unique, otherwise scale will be the way to build a moat in private markets.

But, most importantly, “know thyself” and “know thy moat.”

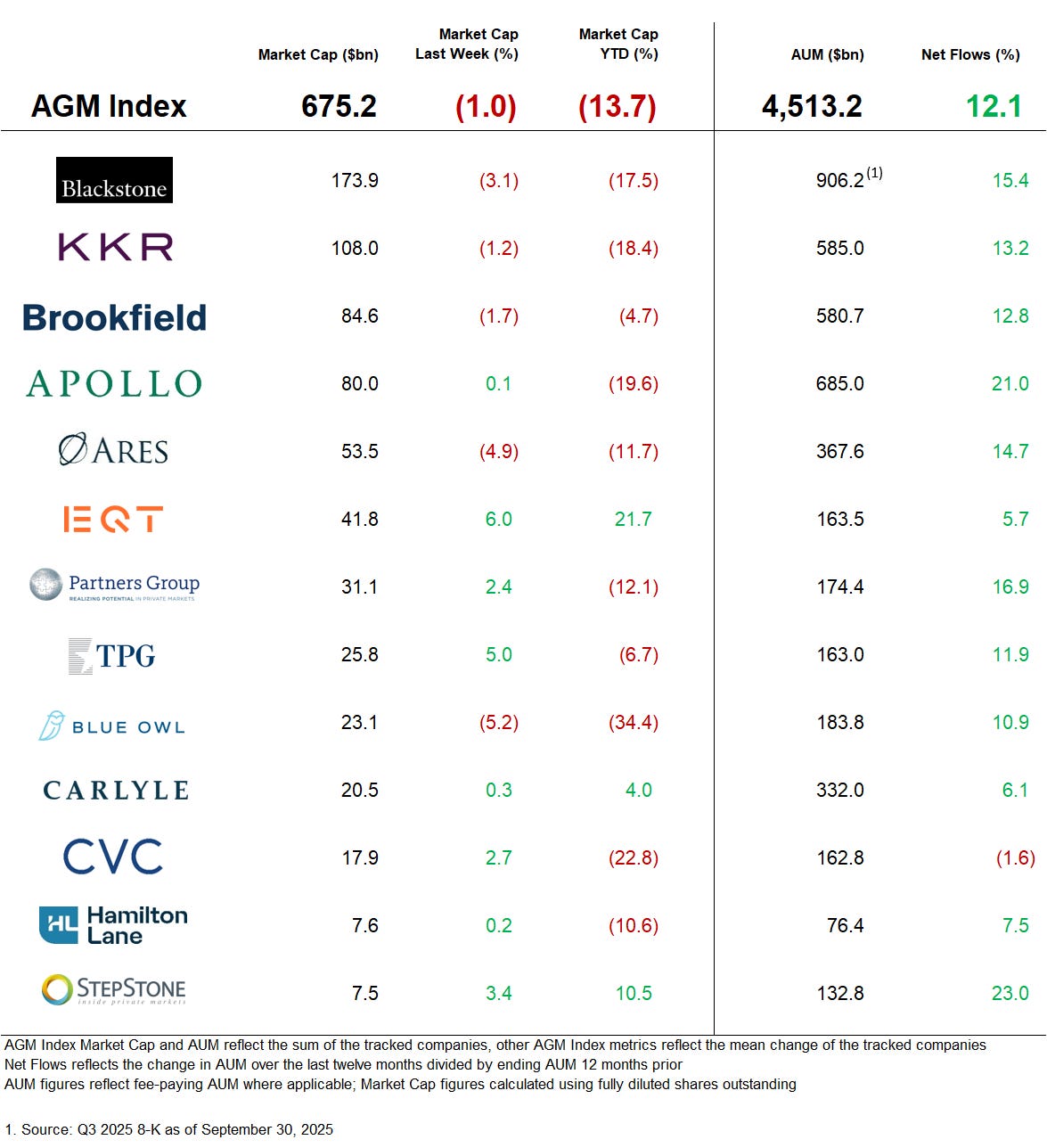

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know, and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Blackstone (Alternative asset manager) - Private Wealth Solutions - Content Marketing, Vice President - Tokyo. Click here to learn more.

🔍 KKR (Alternative asset manager) - Head of AI Product Management. Click here to learn more.

🔍 Apollo Global Management (Alternative asset manager) - Market Intelligence Director. Click here to learn more.

🔍 Ares (Alternative asset manager) - Vice President, Product Management & Client Services, Wealth Management Solutions, APAC. Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Market Leader, Private Wealth, Senior Associate. Click here to learn more.

🔍 Franklin Templeton (Asset manager) - Portfolio Manager, Private Markets. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - Private Markets, Due Diligence Manager - Senior Vice President. Click here to learn more.

🔍 Goldman Sachs Alternatives (Alternative asset manager) - Asset and Wealth Management, Client Solutions Group, Retail Alternatives Specialist, New York - Vice President. Click here to learn more.

🔍 Partners Group (Alternative asset manager) - Investment Leader, Private Equity, Services vertical. Click here to learn more.

🔍 Ultimus Fund Solutions (Fund administrator) - SVP, Business Development. Click here to learn more.

🔍 Allocate (Private markets infrastructure investment platform) - Managing Director / Senior Director, Investments & Research. Click here to learn more.

🔍 SageSpring Wealth Partners (Wealth manager) - Team Financial Advisor. Click here to learn more.

🔍 MSCI (Data services) - Vice President, Program Management - Private Assets. Click here to learn more.

🤝 Interested in partnering with Alt Goes Mainstream? 🤝

Alt Goes Mainstream is a community of engaged experts and executives in private markets.

Fill out this form using the link below to explore partnership opportunities.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

🎥 Watch Vista Equity Partners’ Founder, Chairman, and CEO Robert F. Smith discuss who will benefit from AI and how he built a $100B enterprise software scaled specialist firm. Watch here.

🎥 Watch Nomura Capital Management’s CEO Robert Stark discuss how they have built a private credit firm within a global bank. Watch here.

📝 Read The AGM Op-Ed with Blue Owl Senior MD and Head of Digital Infrastructure Matt A’Hearn on building the backbone of the digital economy. Read here.

🎥 Watch PGIM’s Global Head of Alternative Investments Dominick Carlino discuss the evolution of distributing alternative investments to the wealth channel. Watch here.

🎥 Watch Blue Owl’s Senior MD and Head of Digital Infrastructure Matt A’Hearn share why he believes there’s a generational opportunity in financing digital infrastructure. Watch here.

🎬 Watch AGM Originals The DNA - Season 1 with conversations with EQT’s Conni Jonsson, Jean Salata, Lennart Blecher, Geraldine O’Keeffe, Peter Beske Nielsen, Peter Aliprantis, Hari Gopalakrishnan, William Vettorato, and Ken Wong about the firm’s DNA and its different investing capabilities. Watch here.

🎥 Watch PGIM’s Head of Multi-Asset and Quantitative Solutions Phil Waldeck discuss the intersection of insurance and asset management. Watch here.

🎥 Watch Stonepeak Chairman, Co-Founder, CEO Mike Dorrell share his story as a pioneer in infrastructure investing. Watch here.

🎥 Watch Hg Partner and Head of Value Creation Chris Kindt discuss AI’s transformative role in value creation for private equity. Watch here.

🎥 In Permira Part 2, watch Permira Co-Chairmen & Co-CEOs Brian Ruder and Dipan Patel discuss how the collaborative leadership model in action has helped the firm scale to an €80B alternative asset manager. Watch here.

🎥 Watch Evercore ISI’s Senior MD & Senior Research Analyst Glenn Schorr and me unpack the past few months in private markets on the latest episode of Going Public. Watch here.

🎥 Watch Permira Co-Chairman & Co-CEO Dipan Patel discuss how to scale an €80B alternative asset manager. Watch here.

🎥 Watch Morningstar CEO Kunal Kapoor cover the most pressing topics in private markets today, including the convergence of public and private, liquidity vs illiquidity, investor education, the importance of transparency, and the why, what, and how behind evergreen funds. Watch here.

🎥 Watch The Compound and Friends (TCAF) Co-Hosts and Ritholtz Wealth Management Partners Downtown Josh Brown and Michael Batnick and I go back and forth about private markets on TCAF Episode 207. Watch here.

🎥 Watch Stonepeak Co-President Luke Taylor discuss what it takes to be a great infrastructure investor. Watch here.

🎥 Watch Arcesium MD and Head of Client and Partner Development David Nable discuss how to architect private markets technology infrastructure for the future. Watch here.

🎥 Watch Juniper Square CEO and Co-Founder Alex Robinson on balancing AI with the human element in fund administration. Watch here.

📝 Read the latest AGM Op-Ed — “Retail and the City #2” with former Pantheon Partner Susan Long McAndrews on five takeaways from the Executive Order that could see private assets in 401(k) plans. Read here.

🎥 Watch Hg Senior Partner and Executive Chairman Nic Humphries discuss how Hg has grown into a $100B scaled specialist and how one of the industry’s leading private equity technology and services investors is “navigating investing at an inflection point in history.” Watch here.

🎥 Watch EQT Partner, Head of Private Wealth Americas Peter Aliprantis live from Miami on how EQT is bringing global local. Watch here.

📝 Read The AGM Op-Ed with Arcesium SVP, Business Development - Private Markets Jean Robert on why asset managers need to rethink reporting as a strategic advantage. Read here.

🎥 Watch SageSpring Private Wealth CEO Winston Justice share how he went from protecting star quarterbacks as an NFL tackle to protecting families’ wealth. Watch here.

🎥 Watch Blue Owl Co-President and Global Head of Real Assets Marc Zahr share the story of how he built Oak Street from $17M in AUM in 2009 to what is now Blue Owl’s $67.1B AUM Real Assets business in a live Alt Goes Mainstream podcast at Future Proof Citywide. Watch here.

📝 Read The AGM Op-Ed with former Pantheon Partner Susan Long McAndrews on why everything we need to know might be in Sacramento (where CalPERS is located). Read here.

🎥 Watch Hg’s Partner and Head of Hg Wealth Martina Sanow discuss how Hg has unlocked opportunities for the wealth channel to invest in Europe’s largest portfolio of software and services businesses. Watch here.

🎥 Watch Goldman Sachs’ Partner and Global Co-Head of the Petershill Group at Goldman Sachs Robert Hamilton Kelly discuss the evolution of the GP stakes industry and how Goldman has become a market leading GP stakes investor. Watch here.

🎥 Watch Blue Owl’s MD, Head of Alternative Credit Ivan Zinn unpack private credit and why ABF has become a prominent part of the private credit ecosystem. Watch here.

📝 Read The AGM Op-Ed with Blue Owl Head of Alternative Credit Ivan Zinn on why “asset-based finance today mirrors the evolution of corporate direct lending from over a decade ago.” Read here.

🎥 Watch Lincoln Financial’s EVP and CIO Jayson Bronchetti discuss the role of insurance companies in private markets as he discusses how he manages a portfolio of $300B in assets. Watch here.

🎥 Watch Krilogy’s Partner and CIO John McArthur discuss how an RIA can chart a growth path by building out its private markets capabilities. Watch here.

🎥 Watch New Mountain Capital’s Founder & Chief Executive Officer Steve Klinsky discuss how $55B AUM New Mountain has built a business that builds businesses. Watch here.

🎥 Watch Arcesium’s Private Markets Head Cesar Estrada discuss data silos and technology integrations in private markets. Watch here.

🎥 Watch GeoWealth President & COO Jack Hannah and iCapital SVP, Partnerships Michael Doniger discuss the ground-breaking BlackRock, iCapital, and GeoWealth unified managed account partnership live from iCapital Connect. Watch here.

🎥 Watch Goldman Sachs’ Managing Director, Global Head of Alternatives, Third Party Wealth Kyle Kniffen discuss how they are “standing on the shoulders of Goldman Sachs to be a complete partner” for the wealth channel. Watch here.

🎥 Watch Fortress Investment Group Managing Director & Co-Head of Private Wealth Solutions Adam Bobker discuss how Fortress has built a wealth solutions business from a whiteboard, leaning on the firm’s pioneering history of innovation. Watch here.

🎥 Watch Constellation Wealth Capital President & Managing Partner Karl Heckenberg on why there will be a $1T independent wealth management firm. Watch here.

🎥 Watch BlackRock Managing Director, Co-Head of US Wealth Business, Senior Sponsor for Retirement Business Jaime Magyera and iCapital Chairman & CEO Lawrence Calcano discuss the ground-breaking BlackRock, iCapital, and GeoWealth unified managed account partnership live from iCapital Connect. Watch here.

🎥 Watch EQT Partner & Head of Private Wealth Americas Peter Aliprantis discuss how the firm is bringing EQT’s success to the US wealth market. Watch here.

🎥 Watch KKR Partner & Co-CEO of KKR Private Equity Conglomerate LLC (K-PEC) Alisa Wood discuss how the firm has innovated in private markets, why KKR came up with the Conglomerate structure, and how evergreens can play a role in investors’ portfolios. Watch here.

🎥 Watch Cantilever Group’s Co-Founder and Managing Partner Todd Owens in a live podcast from BTG Pactual’s NYC office share why GP stakes can be the best of all worlds. Watch here.

📝 Read The AGM Op-Ed with Arcesium Private Markets Head Cesar Estrada on the rise of asset-based finance and why it’s the next growth engine for private credit. Read here.

🎥 Watch BlackRock’s Head of the Americas Client Business Joe DeVico, Head of Product for US Wealth & Head of Alts to Wealth Jon Diorio, and Partners Group's Co-Head of Private Wealth Rob Collins discuss their landmark private markets model portfolio partnership that could be the industry’s “iPhone Moment.” Watch here.

🎥 Watch Brookfield Oaktree Wealth Solutions CEO John Sweeney discuss how to build a high-performing wealth solutions team and why the word “solutions” matters when working with the wealth channel. Watch here.

🎥 Watch Cerity Partners’ Partner & Chief Client Officer Tom Cohn and Partner Amita Schultes talk about how and why they have combined a leading OCIO with a $100B AUM wealth management practice. Watch here.

🎥 Watch Marc Lipschultz, Co-CEO of Blue Owl, talk about how they have aimed to skate where the puck is going as Blue Owl has grown its AUM to $265B in nine years. Watch here.

📝 Read The AGM Q&A with Blue Owl Co-CEO Marc Lipschultz, where he highlights some of the trends that have propelled alternative asset management into the mainstream: scale, a focus on private credit, and a focus on private wealth. Read here.

🎙 Listen to Stephanie Drescher, Partner & Chief Client & Product Development Officer of Apollo, discuss what is safe and what is risky as she dives into both the convergence between public and private and the nuances of asset allocation. Listen here.

🎥 Watch Mike Tiedemann, CEO of $72B AUM AlTi Global share why being a global wealth manager can be a differentiator. Watch here.

🎥 Watch Joan Solotar, Global Head of Private Wealth Solutions at Blackstone share why it’s not even early innings, but that it’s “spring training” for private markets adoption by the wealth channel. Watch here.

🎥 Watch Venkat Subramaniam, Co-Founder of DealsPlus on building a single source of truth for private markets. Watch here.

🎥 Watch Yann Magnan, Co-Founder & CEO of 73 Strings discuss the opportunity for AI to automate private markets. Watch here.

🎥 Watch Hamilton Lane Managing Director, Co-Head US Private Wealth Solutions Stephanie Davis and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the third episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch KKR Managing Director, Head of Americas, Global Wealth Solutions (GWS) Doug Krupa and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the second episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch Vista Equity Partners Managing Director, Global Head of Private Wealth Solutions Dan Parant and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the first episode of the Investing with an Evergreen Lens Series. Watch here.

📝 Read about a year in the book of alts — a compilation of the 1,000+ pages written in weekly newsletters on Alt Goes Mainstream in 2024. Read here.

📝 Read about the launch of the AGM Studio, a collaboration between Alt Goes Mainstream and Broadhaven Ventures to incubate, invest in, and help scale companies and funds in private markets. Read here.

🎙 Hear Balderton Capital General Partner and former Goldman Sachs Partner Rana Yared discuss why Europe can build global companies out of the region. Listen here.

🎥 Watch Stepstone Private Wealth CEO Bob Long discuss StepStone Private Wealth’s edge and nuances with their evergreen structures in the first episode of “What’s Your Edge.” Watch here.

🎥 Watch Co-Founder & Managing Partner of Cantilever Group and former Goldman Sachs and Broadhaven Capital Partners Partner Todd Owens discuss the middle market opportunity in GP stakes investing. Watch here.

🎙 Hear me discuss why and how alts are going mainstream on The Compound’s Animal Spirits podcast with Ritholtz Wealth’s Michael Batnick and Ben Carlson. Listen here.

🎙 Hear Manulife’s Global Head of Private Markets Anne Valentine Andrews share how to approach building a private markets investment platform at an industry behemoth and the merits of infrastructure investing. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, on the AGM podcast discuss driving efficiency across the entire value chain to transform private markets. Watch here.

🎙 Hear VC legend New Enterprise Associates’ Chairman Emeritus and Former Managing General Partner Peter Barris discuss how he transitioned from operator to VC and transformed NEA into a venture juggernaut in the process. Listen here.

🎙 Hear Blue Owl’s Global Private Wealth President & CEO Sean Connor share insights and lessons learned from working with the wealth channel. Listen here.

📝 Read about the evolution of GP stakes, why alternative asset management business models are better than SaaS, and our partnership with Todd Owens and David Ballard at Cantilever, a mid-market GP stakes firm anchored by BTG Pactual. Read here.

🎙 Hear how Chris Long, Chairman, CEO, and Co-Founder of Palmer Square Capital Management has built a $29B credit investment firm and a winning NWSL soccer franchise, the KC Current. Listen here.

🎙 Hear stories from building market-defining companies Blackstone, Airbnb, and private markets from Laurence Tosi, former CFO of Blackstone and Airbnb and Managing Partner & Founder of $7.6B investment firm WestCap. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear Blackstone CTO John Stecher discuss how technology is transforming private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with both a macro and VC lens. Listen here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, discusses how they approach alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me and Alt Goes Mainstream on LinkedIn (and AGM’s LinkedIn page), Twitter (@michaelsidgmore), and YouTube to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Ryan McCormack, Nick Owens, and Michael Rutter for their contributions to the AGM Index section of the newsletter.