AGM Alts Weekly | 2.2.25: Postcard from Europe

AGM Alts Weekly #88: Making private markets more public, every week.

👋 Hi, I’m Michael.

Welcome to AGM, the meeting place for private markets.

I’m excited to share my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in private markets so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Presented by

LemonEdge is a leading fund, partnership, and portfolio accounting solution for private markets investment firms with backing from Blackstone Innovations Investments, amongst others. LemonEdge helps GPs, VCs, Family Offices and Fund Administrators transform their back-office operations, through making the complex, simple.

LemonEdge helps firms manage equity, real estate and infrastructure across closed-ended, open-ended and hybrid structures of any variety, with all management fee, waterfalls or other typical Excel based calculations all embedded in LemonEdge. Scale your operations with high efficiency and deliver exceptional LP / GP service.

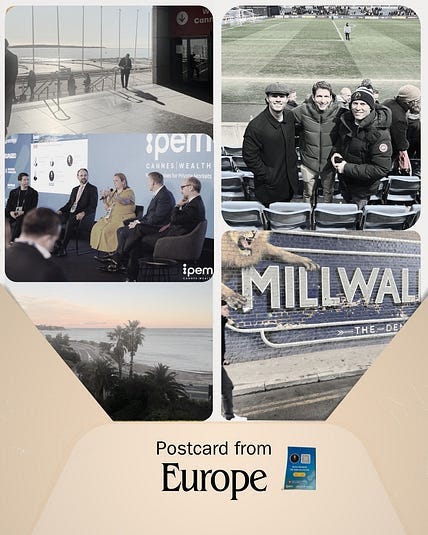

Good afternoon from London, where I have just returned from Cannes. I moderated a panel at IPEM Wealth in Cannes on “How fund managers are adapting to seize the wealth opportunity” with Alisa Wood from KKR, Peter Beske Nielsen from EQT, Erwan Paugam from Ardian, and Jose Luis Gonzalez Pastor from Neuberger Berman.

We had a fascinating discussion that covered many of the hot-button themes GPs and LPs are grappling with as the industry starts to work with wealth in a big way. More on that below.

Following last week’s newsletter, I want to say a word about the Washington Commanders football team. The season ended with a tough loss, but there’s a lot to be excited about. Commanders Owner and 26North Founder Josh Harris captured it here in his thank you letter to the team.

Speaking of games, I went to a football (the European kind) match this weekend in London. Evercore’s Glenn Schorr and Blackstone’s Brian Schorr were over from New York, and we made the trip into the lion’s den to see a Millwall-QPR match in South London at The (infamous) Den.

As much as I like the big clubs and going to the modern stadiums, there’s nothing comparable to visiting a smaller ground like The Den that’s embedded in the fabric of the community. And Millwall is unique for its rather infamous reputation, which surely explains why their supporters were chanting, “no one likes us, and we don’t care.”

The “Golden Age for private markets”

The mood at IPEM Private Wealth in Cannes about private markets, on the other hand, was quite the opposite of “no one likes us, and we don’t care.”

It certainly seems that many GPs like the wealth channel and very much care about it. And for good reason. KKR Partner Alisa Wood said in a Bloomberg interview at IPEM Wealth that it’s the “golden age for private markets.”

The $190T of wealth residing in the hands of individuals that Alisa cited in her interview has put the wealth channel at the forefront of capital raising for the GP community.

The wealth channel should care too, in Alisa’s view. She mentioned that “You need to close that return gap and I think we are entering what will be the golden age of private markets.”

The challenges with adoption of private markets by the wealth channel have been countless. But between product innovation, education, and a focus on building teams to serve the wealth channel, much progress has been made.

From idea to implementation

That was very much the theme of the conversation with Alisa (KKR), Peter (EQT), Erwan (Ardian), and Jose Luis (Neuberger Berman). Each of the panelists cited the importance of providing wealth channel investors with a high-quality investor experience.

Erwan’s analogy that compared working with the wealth channel to the airline industry illuminates some aspects of how alternative asset managers are approaching their engagement with private wealth. Paraphrasing Erwan’s words, “everyone is going to the same place, but like with the airline industry, it might be a slightly different experience” highlights some of the nuances of working with the wealth channel. Different investors require specific product structures to end up in a similar place to institutional allocators.

Interestingly, the live survey during our panel highlighted that the audience, predominantly wealth managers, private banks, and alternative asset managers, supported the notion that new product structures and product innovation are top of mind for allocators. That feature ranked above another critical component of working with the wealth channel: education.

The survey results, although probably too small to be representative of the entire industry, are likely still notable enough to give rise to an interesting observation. Education has been a heavy focus for alternative asset managers and private banks / wealth managers alike. If new product structures and product innovation are now the top priority, does that mean the industry has moved from education as table stakes and ideas to implementation?

No doubt education is still critically important, but comments made by the panelists and a recent report from Citywire’s Selin Bucak about €3B raised in European evergreen (ELTIF) structures suggest that implementation, particularly with evergreen structures, is in full force.

Speaking of implementation, evergreen structures appear to be the product of choice for the wealth channel. EQT’s Peter Nielsen remarked that it’s imperative to make it easy for the wealth channel to invest in private markets, which requires a maniacal focus on the operational aspects of delivering a high-quality investor experience to the end investor.

Creating the right investor experience isn’t easy, particularly with new product structures. I asked Alisa, who co-leads KKR’s two private equity open-ended, perpetual vehicles as Co-CEO of KKR Private Equity Conglomerate LLC (K-PEC) and as a member of the investment committee for the KKR Private Markets Equity Fund, if evergreen funds require a different skillset to manage pre- and post-investment processes, such as deal sourcing, underwriting, and portfolio management.

She made a fascinating observation about managing evergreen funds, remarking that there’s a portfolio management component that “probably looks more like a hedge fund than a private equity fund.”

Effective management of an evergreen fund and engaging wealth channel investors often requires another critical feature that is reserved for a select set of firms: scale.

Scale matters. That includes everything from the ability to deploy capital and win deals across strategies like private equity, private credit, infrastructure, and real estate to having the team to handle the operational lift required to manage evergreen structures.

The topic of scale brings to bear another interesting theme that came up in discussions at IPEM: is it inevitable that the largest firms will win the wealth channel?

Undoubtedly, scale is critical to winning in the wealth channel. Brand matters, too. It resonates in the wealth channel, and for good reason. This feature applies to both the largest alternative asset managers, perhaps one benefit of being a publicly traded company, as well as for traditional asset managers who already possess a deep footprint and history of working with the wealth channel. Neuberger Berman’s Jose Luis echoed this sentiment when asked about the benefits of being a traditional asset manager and building out a more expansive footprint in private markets.

While brand and scale certainly play a role in achieving success in the wealth channel, brand and scale alone are not enough to win. Firms that lack the size and scale of the industry’s biggest players have ways to win, too.

Inherently entrepreneurial

Building a wealth business is building a business.

If the sale of private markets products is like an enterprise software sale, as Bain & Company highlighted in a fantastic report on the topic, then building a wealth business is like starting a startup.

This rings particularly true for firms that are smaller in size than the industry’s largest firms. Those starting a wealth channel business must commit to building a business that fits their firm’s ethos, culture, competency, and edge. That requires buy-in and focus from senior leadership, resources to grow and scale the business, time to figure out product innovation and structuring, a recalibration of marketing and branding, and a focus from the entire firm from front- to back-office on a possible reorientation of how to serve clients.

But not all approaches can be the same. Alisa made the point on the panel and in her interview on Bloomberg that the challenge for the wealth channel navigating private markets is less the how and more “how do you find the who.” She went on to note that “there are thousands and thousands of managers, in the US alone there are more private equity funds than there are McDonald’s.”

This sea of choice for LPs requires alternative asset managers to work hard to stand out, particularly with the wealth channel.

Resources matter, especially when larger firms have the resources to hire marketing teams that can consistently produce content.

But it doesn’t mean that smaller firms, and scaled specialists in particular, can’t compete.

There are tools and tactics that any alternative asset manager can apply to win the wealth channel. After all, if private markets adds another $15T of AUM by 2030, as Preqin predicts, then there will not only be absolute winners (likely the largest firms) but also relative winners too.

Here are some tactics for alternative asset managers to win the game on the field.

Own the relationship with the client

“Going direct” is an increasingly important tool in the toolbox for companies as they are looking to engage with their customers. Consumers seem to be yearning for authenticity. Speaking directly to consumers on either social media, as Blackstone President & COO Jon Gray has brilliantly done with his running videos, or with podcasts have become key ingredients of marketing in authentic ways.

The benefit? A firm doesn’t need to have a massive marketing team or budget to cook up an authentic video to post on LinkedIn.

The content must stay true to the firm and executive’s personality and ethos. That is what should play a role in determining the what and the how of social media marketing activity.

As private markets firms evolve into consumer brands, they can also leverage tactics that connect their work and investing activities with real world examples.

Manulife’s Global Head of Private Markets Anne Valentine Andrews discussed this concept on her Alt Goes Mainstream podcast, highlighting how they connect real assets with real money. Anne said on the podcast that one of her favorite aspects of the job is doing site visits to Manulife’s infrastructure investments with clients.

This type of marketing tactic works well with consumer or infrastructure focused investments, so that gives an edge to firms that invest in areas like infrastructure (airports or solar farms, for example) or sports teams (a Premier League football club or F1, for example). This is one reason why I expect many of the largest alternative asset managers to build out sports-specific investment funds. In addition to sports being an attractive investment proposition, sports can serve as a way to help consumers better understand and make sense of the alternative asset managers’ brand if they can connect the fund’s ownership to their favorite sports team or league.

Social media efforts and podcast episodes not only serve to humanize the people at these firms. Alternative asset managers can also do well to market the “so what” of their work by connecting their investing activities to real life examples of their investments that help consumers understand why their investments are so critical to commerce, transportation, healthcare, computing power, or another category.

Don’t just rely on the algorithm

Social media can provide a low cost and leveraged way for firms to amplify their brand and work to consumers in the wealth channel.

However, anyone posting on LinkedIn or any social platform has to live and die by the algorithm: they have no choice but to rely on the algorithm to reach their audience.

There’s a solution: own the email.

Firms are increasingly coming up with ways to deliver insights directly into consumers’ inboxes.

Apollo’s The Daily Spark with their Chief Economist Dr. Torsten Slok is an example of this brilliance. The Daily Spark provides short, digestible, useful content via email to subscribers.

This also achieves another goal: this steady drumbeat of educational content provides a daily subliminal reminder about Apollo to subscribers and amplifies their brand as a thought leader that shares useful, actionable content.

White papers have often served as a way to capture the email address. I expect this tactic to continue, but I anticipate that firms will do more to try to create content that establishes a direct relationship with their desired clientbase.

I am aware that marketers are concerned about inbox overload — and that consumers will want to limit the number of emails and subscriptions that they receive on a daily basis. But if firms have something to say and educational value to provide, then consumers will want to hear from alternative asset managers.

Become a content production factory

Part of building a brand is owning the production of content.

Many of the largest alternative asset managers often say that they will win the wealth channel because working with wealth requires ample boots on the ground to educate and build relationships of trust. That’s certainly true, but “boots on the ground” can extend into the digital realm if we think of it as the digital footprint. Firms lacking the human resources to holistically cover the wealth channel can gain leverage by being everywhere, all the time, digitally.

Firms of all sizes can figure out how to become content production factories, albeit in different ways.

iCapital’s strategic decision to build a studio in their office is an example of this brilliance. Their studio manufactures content on a daily basis that is delivered to the wealth channel. By bringing this production in-house, iCapital can own the end-to-end process of content creation and production rather than rely on outside resources, giving them the flexibility and autonomy to move at a pace that fits their culture and ethos.

Perhaps this point also makes sense of a recent job posting by Blackstone: Senior Video Producer in their Marketing department.

Making private more public

If going direct is the new feature of media and marketing, does that mean every company is a media company?

Firms must become accustomed to being more public — or at least entertain the idea of being more public about their brand and their work, whether they like it or not. That’s not an easy feat, particularly for an industry that has historically been private for years.

This cultural change will require buy-in and support from the most senior levels of the firm to be successful — and it is increasingly becoming a core part of the strategy to win the wealth channel rather than a nice-to-have.

Winning in wealth

Where does this seismic shift in marketing leave alternative asset managers in their quest to win the wealth channel?

Another question that came to mind after conversations I had at IPEM is if a firm that hasn’t taken in outside capital from a GP stakes fund or has gone public will be able to succeed in the wealth channel.

Do privately owned firms have enough capital and firepower to rival firms that have the war chest to hire marketing and distribution professionals and spend capital on digital marketing?

The chart from Blue Owl’s 2024 GP Strategic Capital Outlook on assets raised by strategy highlights that brand and scale will likely matter more in certain strategies than others.

Strategies like Infrastructure and Natural Resources will see the Top 10 managers raise the lion’s share of assets.

But scaled specialists — like Stonepeak in Infrastructure, which has over $72B AUM, or Vista, with over $100B AUM, Hg Capital, with over $75B AUM, and Permira, with €80B AUM, in software and growth, have the ability to carve out a niche in marketing and branding that should enable them to win in the wealth channel (note: Stonepeak and Vista have taken GP stakes from Blue Owl’s GP Strategic Capital, while Hg and Permira have not).

These firms can create unique product structures, either by how they structure evergreen funds or how they seed these funds with a specific LP base, that can enable them to achieve success in capital raising.

I’d also expect these types of firms to figure out how to partner with other firms that have no competitive overlap to create “best-of-breed” model portfolios.

Getting in the models will be critical to success in winning the wealth channel, so if firms can establish alliances to build a bespoke model portfolio in private markets for the wealth channel, then they could fit the pieces of the puzzle together to become a relative winner in a complex and fragmented wealth market.

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

Post of the Week

Marketing done social. Blackstone’s President & COO Jon Gray shared “their version of a post-game interview” on LinkedIn live from the “room where it happens” about their most recent earnings call, which was one of their best quarters in history. Gray mentioned private wealth, private credit, and infrastructure as growing areas of the firm.

AGM News of the Week

Articles we are reading

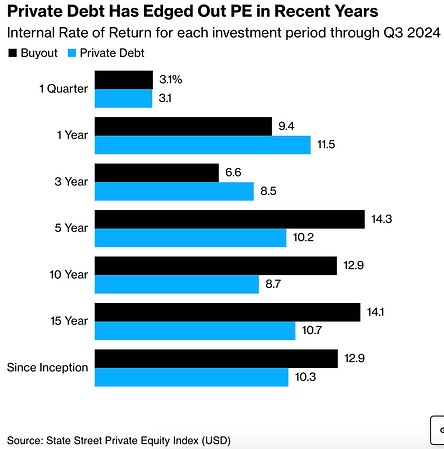

📝 Private Equity Returns Overtake Private Credit in Rebalancing | Kat Hidalgo, Bloomberg

💡Bloomberg’s Kat Hidalgo reports that private equity returns bested private credit returns in the third quarter, according to data from State Street. Could this shift be a signal that LPs will shift their interest from private credit to private equity now that private equity is outperforming private credit?

Private equity funds returned 3.09% in the period ended Sept. 30, a tick above the 3.06% return for private credit. Private equity returns were driven by an uptick in buyout activity, lower interest rates, and narrower spreads on private debt due to increased competition for deals. State Street’s Head of Product Implementation and Alternative Investment Research Nan Zhang noted that private equity should continue its outperformance if “inflation is kept under control.” Lower rate cuts would almost certainly have an impact on private credit deals that are tied to floating interest rates, resulting in lower absolute returns in private credit.

There are early signs of a pickup of interest in private equity. According to iCapital, investors have already started allocating more to private equity strategies than private credit over the past quarter.

The industry’s largest private credit players have still been able to raise funds, but funds have to separate themselves from the pack. At a DealCatalyst direct lending conference in London this past Monday, Corinthia Global Management Head of European Investments Mark Wilton said that firms have to “differentiate [themselves].” LPs appear to share that sentiment. “Private credit is overcrowded,” said Paul Karger, Managing Partner at $7.9B AUM multi-family office TwinFocus Capital Partners. “I never want to be in the consensus trade. Things never work out like the promoters of an asset class are initially underwriting.”

Many private credit firms have faced challenges raising funds as of late, particularly in the interval fund space. Meketa Capital’s CEO Michael Bell noted this in a recent interview, saying, “Private credit in the interval funds space is very crowded. If you’re just another fund in private credit it’s really hard to stand out.”

💸 AGM’s 2/20: Private credit has been one of the fastest growing segments of private markets — and for good reason. The need to finance both sponsor-backed and non-sponsor-backed companies require capital, particularly as banks have faced increasing regulatory headwinds. The ability to generate attractive returns, and in some cases, private equity-like returns for private credit-like risk, made private credit an appealing area of the market for many allocators. That is still true today in certain cases, but the prospect of lower rates has certainly dampened enthusiasm for private credit for certain investors at the expense of allocating to private equity instead.

Private credit has done well for investors as of late. State Street’s Private Equity Index highlights private credit’s outperformance on an IRR basis over the past year and past three years. However, over a longer time horizon, private equity has outperformed private credit.

It’s worth noting on the above data that manager selection is critical, whether it be private equity or private credit. But over the long run, private equity has tended to outperform, albeit with a different level of risk and cadence of cashflows and distributions than private credit. There’s no single right answer to asset allocation — and investors should probably have exposure to both private equity and private credit over multiple cycles as they provide somewhat different risk and return profiles. Still, it is notable for the private equity industry that it appears that investors seem to be more favorable on private equity now that firms, as we discussed when highlighting EQT last week, are beginning to see streams of distributions come back from private equity investments.

📝 Investors offloaded record volume of private equity stakes in 2024 | Ivan Levingston and Alexandra Heal, Financial Times

💡Financial Times’ Ivan Levingston and Alexandra Heal report that the secondary market saw record amounts of private equity investments changing hands in the secondary markets. An analysis by Jefferies found that $162B in volume was transacted last year, which was a 45% increase from the prior year and over 20% higher than the previous peak in 2021. The secondary market has become a critical source of LPs that have been searching for liquidity, with the LP-led secondary market hitting $87B in volume. This figure is a 36% increase over the previous record that was set in 2021. Interestingly, the discount for selling stakes narrowed to 6% below NAV for buyout fund stakes, down from a 9% spread the year prior. Jefferies said that this increase in pricing could be a signal that private equity managers could achieve liquidity as IPO and exit activity picks up.

Private credit secondaries also saw a tightening of spreads between discount and NAV, going from 77% of NAV to 91% of NAV. Real estate and venture capital pricing did not see the same tightening of discounts to NAV, with real estate at 72% of NAV and venture at 75% of NAV. GP-led secondaries also saw an increase, with 2024 representing a 44% increase over the prior year’s transaction volume at $75B of assets. The majority of GP-led secondaries came in the form of continuation vehicles, where managers sold assets from one of their funds into a newer fund managed by the same firm.

💸 AGM’s 2/20: Secondaries have become a critical part of the growing private markets ecosystem as liquidity has become top of mind for both LPs and GPs alike. The data from 2024 secondary markets reflect the desire for LPs to find ways to seek liquidity, with 2024 closing out as a record-setting year for secondaries.

The growth in the secondaries market highlights an important trend: active management of a portfolio has become an even more critical function for both GPs and LPs. Figuring out when and where to achieve liquidity and rebalance a portfolio in private markets has always been part of the business, but interestingly, the advent of evergreen structures puts even more pressure on the portfolio management function of closed-end fund vehicles because now investors have more options for where and how to allocate their capital in private markets. One of the selling point of evergreen structures is that LPs don’t need to rely on (or wait for) distributions in their private equity portfolio to re-invest into the next vintage. The time lag between distribution and re-investment can reduce IRRs, argue those in favor of evergreen structures. Evergreens make it easier for LPs to manage their cashflow plans over the long-term for their investing activities in private markets, making it a simpler option for many allocators to private markets, particularly those that are newer to the space and want to be invested immediately.

Evergreen funds, in some cases, can become a buyer of secondaries from private equity funds. This can make for a natural exit event for private equity firms. This development for private markets also means that managers responsible for closed-end funds might have to be cognizant of more active portfolio management to generate DPI for investors that can otherwise choose to allocate to evergreen structures. Both evergreen structures and closed-end vehicles have a role to play for investors in private markets, but the growth of the secondaries market brings rise to some interesting questions going forward.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know, and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Blackstone (Alternative asset manager) - Senior Video Producer, SVP - Marketing. Click here to learn more.

🔍 Apollo (Alternative asset manager) - Senior Public Investor Relations Professional. Click here to learn more.

🔍 Ares (Alternative asset manager) - Vice President, Product Management & Client Services, Wealth Management Solutions, APAC. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - Head of Business Development, Family Offices - Senior Vice President / Managing Director. Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Private Wealth Strategy Senior Lead - Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Private Wealth, Head of RIA Channel Marketing, Principal - Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Private Wealth, Alternative Credit Product Marketing, Vice President - Click here to learn more.

🔍 Brookfield (Alternative asset manager) - VP, Private Markets Products. Click hear to learn more.

🔍 BlackRock (Asset manager) - Aladdin Wealth Tech - Vice President, Implementation Manager. Click hear to learn more.

🔍 Hamilton Lane (Alternative asset manager) - Vice President, Data Intelligence. Click here to learn more.

🔍 Hightower - Crest Capital Advisors (Wealth manager) - Private Wealth Associate - Crest Capital Advisors. Click here to learn more.

🔍 Dynasty Financial Partners (Wealth management platform) - Alternative Investment Specialist. Click here to learn more.

🔍 Edward Jones (Wealth manager) - Director, Alternative Investment Strategy. Click here to learn more.

🤝 Interested in partnering with Alt Goes Mainstream? 🤝

Alt Goes Mainstream is a community of engaged experts and executives in private markets.

Fill out this form using the link below to explore partnership opportunities.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

🎥 Watch Keith Jones, Senior Managing Director, Global Head of Alternative Investments Product at Nuveen live from Nuveen’s nPowered conference on structuring products for success for the wealth channel. Watch here.

🎥 Watch Jeff Carlin, Senior Managing Director, Head of Global Wealth Advisory Services at Nuveen live from Nuveen’s nPowered conference on why “it’s all about the end client.” Watch here.

🎥 Watch Venkat Subramaniam, Co-Founder of DealsPlus on building a single source of truth for private markets. Watch here.

🎥 Watch Yann Magnan, Co-Founder & CEO of 73 Strings discuss the opportunity for AI to automate private markets. Watch here.

🎥 Watch Lawrence Calcano, Chairman & CEO of iCapital on episode 14 of the latest Monthly Alts Pulse as we discuss whether or not private markets has moved from access as table stakes to customization and differentiation. Watch here.

🎥 Watch Hamilton Lane Managing Director, Co-Head US Private Wealth Solutions Stephanie Davis and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the third episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch KKR Managing Director, Head of Americas, Global Wealth Solutions (GWS) Doug Krupa and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the second episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch Vista Equity Partners Managing Director, Global Head of Private Wealth Solutions Dan Parant and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the first episode of the Investing with an Evergreen Lens Series. Watch here.

📝 Read about a year in the book of alts — a compilation of the 1,000+ pages written in weekly newsletters on Alt Goes Mainstream in 2024. Read here.

🎥 Watch the second episode of Going Public on Alt Goes Mainstream with Evercore ISI Senior MD and Senior Research Analyst Glenn Schorr as we discuss trends and business models for the publicly traded alternative asset managers. Watch here.

📝 Read about the launch of the AGM Studio, a collaboration between Alt Goes Mainstream and Broadhaven Ventures to incubate, invest in, and help scale companies and funds in private markets. Read here.

🎙 Hear Balderton Capital General Partner and former Goldman Sachs Partner Rana Yared discuss why Europe can build global companies out of the region. Listen here.

🎙 Hear Churchill Asset Management by Nuveen’s MD, Senior Investment Strategist & Co-Head of the Chicago Office Alona Gornick discuss the evolution of private credit, the power of permanent capital, and the importance of the product specialist. Listen here.

🎥 Watch Stepstone Private Wealth CEO Bob Long discuss StepStone Private Wealth’s edge and nuances with their evergreen structures in the first episode of “What’s Your Edge.” Watch here.

🎙 Hear $5B AUM Ritholtz Wealth Management’s Director of Institutional Asset Management Ben Carlson bring a wealth of common sense to asset allocation and private markets. Listen here.

🎙 Hear Blue Owl, Inc. Board Member and Blue Owl GP Strategic Capital Senior Managing Director Sean Ward on how $57.8B AUM Blue Owl GP Strategic Capital has pioneered GP staking and transformed GP stakes into an industry. Listen here.

🎥 Watch HGGC Partner, Chairman, Co-Founder & Former NFL Hall of Fame Quarterback Steve Young and True North Advisors CEO & Co-Founder Scott Wood discuss how “the score takes care of itself” on the field and in investing / wealth management. Watch here.

🎥 Watch Eileen Duff, Managing Partner & Chief Client Success Officer at iCapital on episode 12 of the latest Monthly Alts Pulse as we discuss the future of AI and automation in private markets. Watch here.

🎥 Watch Co-Founder & Managing Partner of Cantilever Group and former Goldman Sachs and Broadhaven Capital Partners Partner Todd Owens discuss the middle market opportunity in GP stakes investing. Watch here.

🎙 Hear Intapp’s President, Industries, and Co-Founder of DealCloud by Intapp Ben Harrison discuss how data and automation are transforming private markets. Listen here.

🎙 Hear how a $1.59T AUM asset manager is approaching private markets with T. Rowe Price’s Global Head of Product Cheri Belski in a special live episode of the Alt Goes Mainstream podcast at a Pangea x AGM Breakfast in London. Listen here.

🎙 Hear Bernstein Private Wealth Management’s CIO Alex Chaloff discuss how a $125B wealth manager navigates private markets. Listen here.

🎙 Hear me discuss why and how alts are going mainstream on The Compound’s Animal Spirits podcast with Ritholtz Wealth’s Michael Batnick and Ben Carlson. Listen here.

🎙 Hear Mercer Investments’ US Financial Intermediaries Leader Gregg Sommer and CAIS’ MD and Head of Investments Neil Blundell on following the fast river of alts. Listen here.

🎙 Hear Manulife’s Global Head of Private Markets Anne Valentine Andrews share how to approach building a private markets investment platform at an industry behemoth and the merits of infrastructure investing. Listen here.

🎙 Hear Partners Group’s Co-Head of Private Wealth, Head of the New York Office, Member of the Global Executive Board Rob Collins share the how and why of one of the most exciting trends in private markets: evergreen funds. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, on the AGM podcast discuss driving efficiency across the entire value chain to transform private markets. Watch here.

🎙 Hear VC legend New Enterprise Associates’ Chairman Emeritus and Former Managing General Partner Peter Barris discuss how he transitioned from operator to VC and transformed NEA into a venture juggernaut in the process. Listen here.

🎙 Hear Blue Owl’s Global Private Wealth President & CEO Sean Connor share insights and lessons learned from working with the wealth channel. Listen here.

🎙 Hear Ritholtz Wealth Management’s Managing Partner Michael Batnick share views on how wealth managers are navigating private markets. Listen here.

📝 Read about the evolution of GP stakes, why alternative asset management business models are better than SaaS, and our partnership with Todd Owens and David Ballard at Cantilever, a mid-market GP stakes firm anchored by BTG Pactual. Read here.

🎥 Watch internet pioneer Steve Case, Chairman & CEO of Revolution and Co-Founder of America Online, share lessons learned from building the first internet company to go public and an investment firm built for the Third Wave of the internet. Watch & listen here.

🎙 Hear how Chris Long, Chairman, CEO, and Co-Founder of Palmer Square Capital Management has built a $29B credit investment firm and a winning NWSL soccer franchise, the KC Current. Listen here.

🎙 Hear stories from building market-defining companies Blackstone, Airbnb, and private markets from Laurence Tosi, former CFO of Blackstone and Airbnb and Managing Partner & Founder of $7.6B investment firm WestCap. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear wealth management industry titan Haig Ariyan, CEO of Arax Investment Partners, share his thoughts on the private equity opportunity in wealth management. Listen here.

🎙 Hear Blackstone CTO John Stecher discuss how technology is transforming private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with both a macro and VC lens. Listen here.

📝 Read how 73 Strings CEO & Co-Founder Yann Magnan and team are leveraging AI to build a modern and holistic monitoring and valuation platform for private markets in The AGM Q&A. Read here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, discusses how they approach alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Michael Rutter and Nick Owens for their contributions to the newsletter.