AGM Alts Weekly | 6.29.25: Morningstar Investment Conference and report recap - "Credit is king"

AGM Alts Weekly #109: Making private markets more public, every week.

👋 Hi, I’m Michael.

Welcome to AGM, the meeting place for private markets.

I’m excited to share my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Some testimonials about the AGM Sunday Alts Weekly newsletter include:

“When it comes to the intersection of alternative investments and wealth management, Michael just gets it.” CIO, $18B AUM RIA.

“This is our primary resource for learning and reading about alts.” Head of Marketing, $250B AUM alternative asset manager.

“If you want timely and informative insights on everything private markets, Michael Sidgmore and Alt Goes Mainstream weekly update and podcast are fantastic resources.” CIO, $47B AUM RIA.

“The only email I never delete when clearing my inbox.” Senior distribution professional, $330B+ AUM asset manager.

Join us to understand what’s going on in private markets so you and your firm can stay up to date on the latest trends at the intersection of private markets and wealth management and navigate this rapidly changing landscape.

Presented by

For too long, private equity funds have relied on manual processes — spreadsheets, scattered documents, disjointed data — to track complex investment and ownership structures. It’s slow, error-prone, and not scalable. And when regulators, investors, or auditors come knocking, it’s a fire drill every time.

At DealsPlus, we help private equity funds digitise investment and ownership structures, eliminating data silos. Our software helps power key workflows such as: quarterly reporting, audits, compliance, and exits.

Good morning from Washington, DC. I’ve just returned from Chicago, where Morningstar CEO Kunal Kapoor and I recorded a live podcast episode of Alt Goes Mainstream at the Morningstar Investment Conference.

Kunal and I had a fascinating conversation. We covered a number of the most pressing topics in private markets today: the convergence of public and private, liquidity vs illiquidity, investor education, the importance of transparency, and the why, what, and how behind evergreen funds.

Speaking of transparency and evergreen funds, Morningstar released a robust report on the state of evergreen funds, titled “The State of Semiliquid Funds,” at their conference this week.

The report highlighted a number of key trends with evergreen funds and unpacked nuances of vehicle structure, fees, fundraising, and performance.

Let’s dive in.

“Credit is king”

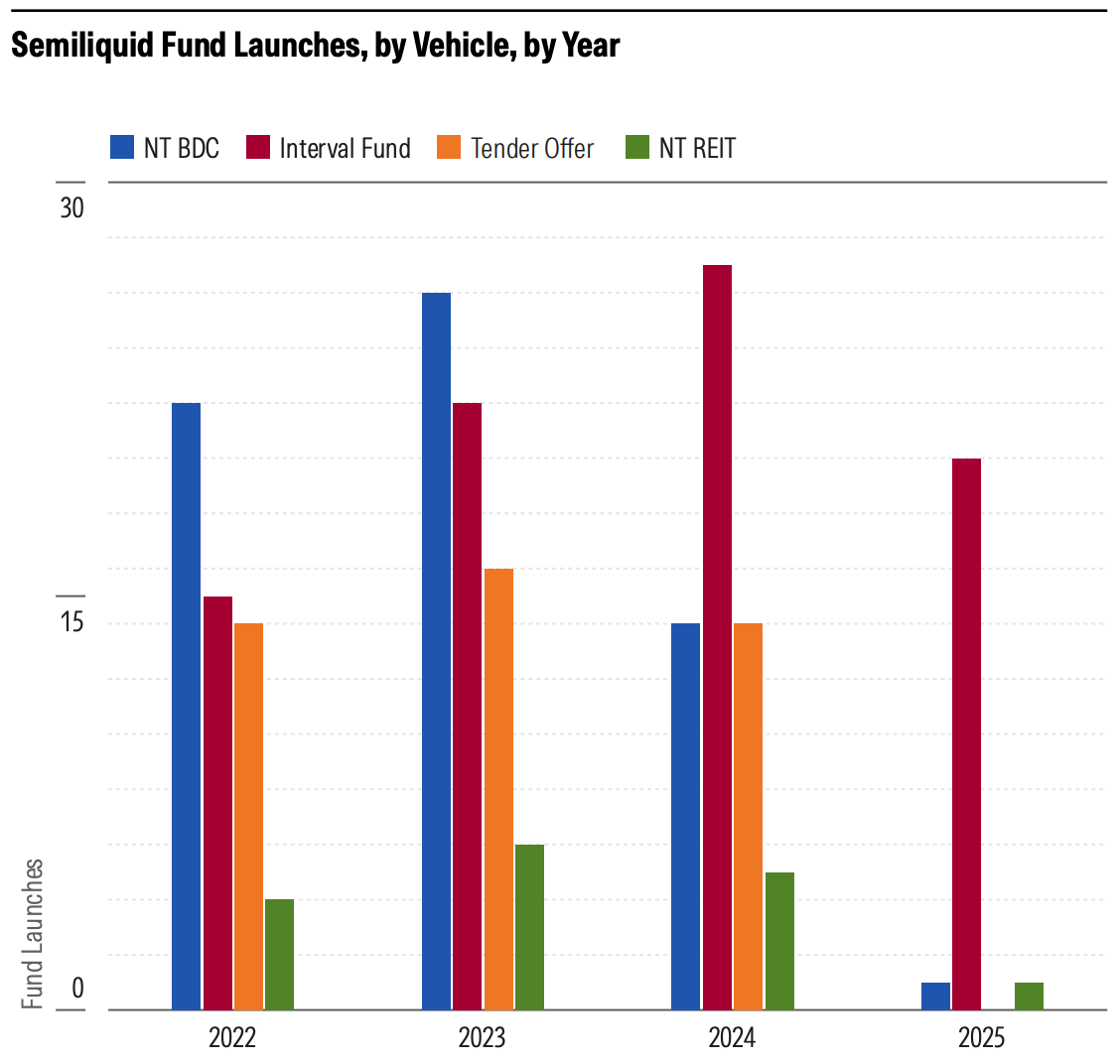

Charts from Morningstar’s presentation highlighted the rapid ascent of evergreen fund structures — both in terms of new fund launches and net flows into evergreen funds.

Net assets in evergreen funds have grown around 60% since 2022, reaching almost $350B.

Credit has often been the strategy of choice for investors looking to allocate to evergreen fund structures, particularly for the largest evergreen funds.

2025 looks like it will be another big year for evergreen fund launches.

It’s also worth noting that the interest and inflows into evergreen structures is mainly advisor-led at this point. Individuals, for the most part, are unable to access evergreen funds directly, as evergreen funds are not yet available on retail brokerage platforms like Fidelity, Schwab, and others … for now, as I wrote about the “brokerages going for broke” (eventually) in the 10.13.24 AGM Alts Weekly.

Interestingly, while non-traded BDCs have been the vehicle of choice in recent years, interval funds have been the most common vehicle to launch in 2025, in part due to their friendly operational structures for wealth platforms. Interval fund launches have far outpaced other vehicle structures — and look to blow past its 2024 record of 27 interval fund launches.

The vehicle of choice

One of the more notable stats from Morningstar’s report?

The popularity of credit funds — and non-traded BDCs, in particular — are amongst investors.

Credit evergreen structures have grown to almost $200B of net assets, more than doubling in the past two years.

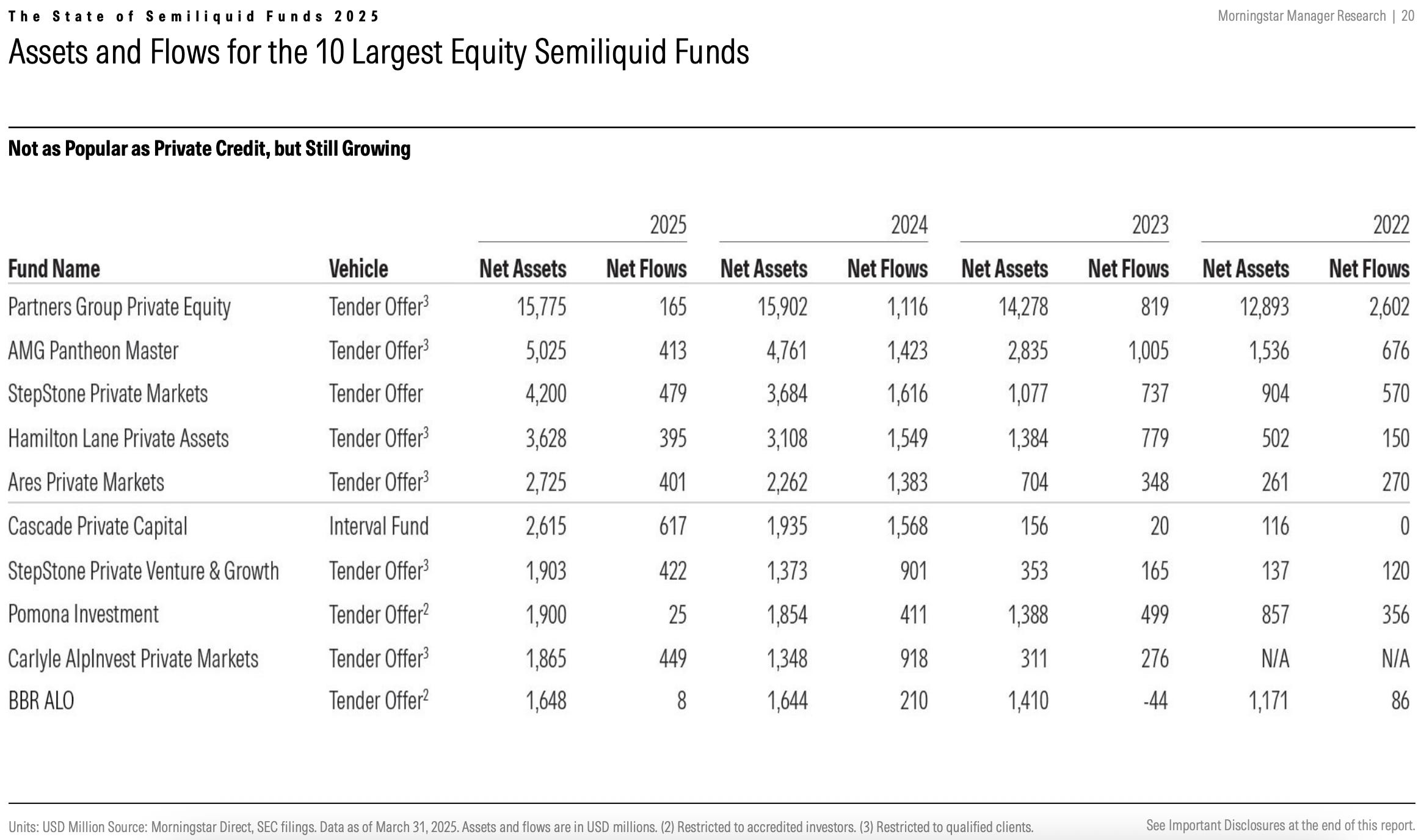

Non-traded BDCs appear to be the vehicle of choice in the evergreen credit space. Four of the top five largest evergreen credit vehicles are non-traded BDCs, according to Morningstar as the chart below illustrates.

The majority of the top ten credit evergreen funds are non-traded BDCs, as well.

Blackstone’s private credit fund, BCRED, is the industry’s largest credit evergreen vehicle, topping $42B in net assets. That figure is up from $22.6B in net assets in 2022.

Blackstone isn’t the only firm to witness its credit evergreen funds experience astronomical growth in net assets.

Cliffwater’s credit interval fund grew from $10B in net assets in 2022 to over $27.8B in net assets by 2025.

Blue Owl’s non-traded BDC increased its net assets from $5.78B in 2022 to over $16.2B in 2025.

Apollo’s non-traded BDC grew from $2.1B in 2022 to over $11.3B in 2025.

Perhaps an explanation for the popularity of evergreen credit funds lies in a comparison to leveraged loans.

Morningstar compared the returns of the largest private credit evergreen funds to the Morningstar LSTA Leveraged Loan Index since the inception of each evergreen’s oldest share class. Many of the evergreens outperformed, some by a wide margin.

But, it’s worth noting that many of the private credit evergreen structures employ leverage, so it’s worth evaluating evergreen returns in the context of their leverage, too.

As credit experiences a rapid rise in inflows, real estate and infrastructure evergreens have headed in the opposite direction.

Morningstar found that real estate/infrastructure evergreen funds were the only broad asset class group to see assets decline over the past three years. Net assets in real estate/infrastructure evergreens fell to $74B at the end of 2024, from $80B in 2023 and $91B at the end of 2022.

While private equity has historically been the largest asset class within private markets, flows into evergreen private equity strategies are outpaced by those into its private credit counterparts.

Morningstar reported that there was approximately $50B in net assets in private equity evergreen funds in 2024. This figure is a sizable increase from 2022, when there was $24B in net assets in private equity evergreens, but it still pales in comparison to the close to $200B in net assets in credit vehicles.

Tender offer funds have dominated the private equity evergreen fund landscape. Each of the five largest private equity evergreen funds, led by Partners Group (hear more about evergreen funds from evergreen fund pioneer Partners Group’s Rob Collins on Alt Goes Mainstream here and here), are tender offer fund structures. And all but one fund in the top ten — Cascade Private Capital, which is now owned by Cliffwater — is a tender offer structure.

The 2025 fundraising story has yet to be fully written, but it looks like some of the top ten largest private equity evergreen structures could surpass their 2024 net flows if fundraising performance from Q1 2025 continues apace for the rest of the year.

Morningstar’s report gives rise to a host of takeaways for both asset managers and wealth managers as they look to navigate the rapidly changing landscape of public and private markets.

Cliffwater is a prolific fundraiser

Another set of figures jumped out in Morningstar’s report: Cliffwater has had a prolific fundraising run.

Cliffwater’s private credit evergreen structure, Cliffwater Corporate Lending interval fund, is the second largest private credit evergreen vehicle, topping $27B in net assets.

This figure is significantly higher than the $10B in net assets in 2022. Not only is Cliffwater’s Corporate Lending fund a top two chart topper, but the firm has a second evergreen fund, the Enhanced Lending interval fund that is over $5B in net assets, which has increased almost 5x since 2022.

Part of the magic of Cliffwater’s credit fund? The fund is comprised of a diversified set of loans — and credit funds — that provides exposure to a pool of 3,800 borrowers. Other funds in the top ten all have strong origination engines, but investors are limited to the origination capabilities of the firm’s respective investment platform, which is not the case with Cliffwater.

It’s not just Cliffwater’s credit funds that have had a good fundraising run. It’s also their private equity evergreen fund — Cascade Private Capital — which has had the highest net flows of any private equity evergreen fund in the top ten funds in 2025.

There’s probably also something to be learned from Cliffwater’s content strategy. The firm has led with content — via research and indices — for years. Not only has this provided the firm with a deep understanding of the market that can be delivered in an authoritative, agnostic voice that resonates with LPs, but the firm has also been afforded with the opportunity to build strong relationships with GPs that have resulted in the ability to invest in — and co-invest alongside — GPs in their evergreen structures. This construct has enabled Cliffwater to effectively provide diversified access to private credit and private equity through evergreen wrappers to the wealth channel, making this appealing to investors who want exposure to a large number of GPs and underlying investments.

For investors that want exposure to the broad market, an evergreen structure that offers access to multiple GPs (so long as the layered fees are not too exorbitant) and underlying investments and co-investments could be a good fit.

The convergence of public and private, divergence of fees?

Public and private markets are converging — that was a theme prevalent in conversations at the Morningstar Investment Conference.

But as public and private converge (which, interestingly, is the title of a new job posted by Morningstar), fees appear to be diverging.

Morningstar’s report illustrates that evergreen fund fees are significantly higher than mutual fund and ETF fees.

Now, there are reasons why there’s a difference in fees, particularly in credit.

Evergreen funds, particularly evergreen credit structures, use leverage, which means that there are borrowing costs.

Will evergreen fund fees likely come down over time? Yes, there’s a possibility that that will occur, particularly if evergreen fund structures grow in size.

It’s a topic that Kunal and I discussed in our podcast — and it’s a critical part of the investor experience.

But, as Apollo’s Marc Rowan said on stage at the Morningstar Investment Conference in his interview with Kunal, private markets are justified when it delivers “excess returns per unit of risk.”

If returns from private markets outpace public markets, then perhaps the fees remain both justified and steady. Fees have remained relatively steady for many private markets firms in closed-end funds.

Charts from J.P. Morgan Asset Management’s recent “Guide to Alternatives” highlight that returns in many private markets asset classes have outpaced that of public markets (based on returns from 1Q15-1Q25).

J.P. Morgan’s chart also highlights the importance of manager selection in private markets. Interquartile dispersion is significantly wider in private markets than in public markets.

This feature also extends to evergreen structures, as $47B AUM Clearstead CIO Aneet Deshpande highlighted in a LinkedIn post (which was AGM’s Post of the Week last week).

It also appears that adding private markets strategies to a 60/40 portfolio both increases annualized returns and dampens volatility.

Morningstar’s research gives rise to a question worth asking: how much should private markets funds be compared to ETFs and mutual funds?

Yes, fees often different between private markets funds and ETFs and mutual funds, but perhaps so too is the intent behind the why of allocating to private markets.

That’s part of the message that Apollo CEO Marc Rowan delivered in his talk at the Morningstar Investment Conference with Morningstar CEO Kunal Kapoor.

Kunal asked Marc great questions that took the conversation directly to the heart of many of the most pressing issues and questions at the intersection of public and private markets today.

Marc’s talk with Kunal provided both a number of key takeaways for alternative asset managers, traditional asset managers, and investors as they look to navigate the convergence between public and private that we’ll dive into next week.

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

AGM Post of the Week

There are strains on LPs ability to deploy additional capital, as Arctos’ Chart of the Week indicates, in large part due to the lack of distributions back to LPs.

AGM News of the Week

Articles we are reading

📝 Private equity-backed Visma picks London for blockbuster tech IPO | Alexandra Heal and Ivan Levingston, Financial Times

💡 Financial Times’ Alexandra Heal and Ivan Levingston report that Hg-backed €19B Visma has chosen London over Amsterdam (and the US) for its landmark IPO. This decision represents a big win for the London Stock Exchange, which has seen a decline in listings. Last year, 88 companies delisted or transferred their primary listing from the LSE, with only 18 new listings happening in their place. 2025 has been another challenging year for the LSE; just three IPOs with a combined market capitalization at listing of less than £100M have occurred. But London still has appeal to companies and investors, as the decision with the Visma listing highlights. According to people familiar with the deliberations, London won out on the Visma IPO because of its deep capital markets and the presence of more investors who focus on buying UK stocks.

Visma, the mission-critical accounting and payroll software provider to small and medium-sized businesses which has grown through 350 bolt-on acquisitions after Hg took the company private from the Oslo stock exchange in 2006 at a valuation of £380M, has grown into one of Europe’s largest software companies. The company reported €2.8B in revenues and free cashflow of €885M in 2024.

The company’s success marks a major win for Hg and other private equity firms, including TPG. Hg owns around 70% of Visma, with the remainder of the cap table including Singapore’s sovereign wealth fund GIC, TPG, Intermediate Capital Group, Canadian pension plan CPP Investments, Jane Street, and Altaroc, amongst others, in addition to group employees.

💸 AGM’s 2/20: The LSE scored a big win by convincing Visma to list in London as opposed to Amsterdam, where alternative asset manager CVC listed last year, or the US. Many European companies as of late, such as British fintech Wise, have chosen to list in the US given its deep capital markets, but Visma’s choice of the LSE bucks that trend. Perhaps it’s a sign that European markets could be making a comeback.

Is it part of the broader trend that now could be Europe’s time? It will be interesting to see how European capital markets unfold over the coming years, particularly as many of the industry’s largest alternative asset managers choose to direct meaningful capital to the region. A few weeks ago, Blackstone said that they would be investing $500B into Europe over the next 10 years. Surely, a good portion of that will go to credit, real estate, and infrastructure, all of which are markets that require scale and capital to finance a number of megatrends. One example of this trend? Blue Owl Capital’s Co-President and Head of Real Assets Marc Zahr outlined in the Blue Owl 2025 Midyear Outlook why Europe represents a compelling investment opportunity in the triple net lease real estate investment strategy, citing strong tailwinds and favorable data. Marc noted “increased investment in supply chain resilience and defense spending” as means of “fostering opportunities to reshore production back to the region.” The data appears to align with this view. In Q1 2025, real estate transaction volume in Europe reached $50B, a 30% year-over-year increase.

But it’s not just these other large asset classes within private markets where investors are directing capital across Europe. Last week, AGM covered Thoma Bravo’s bullish case for European software companies, which unpacked Thoma Bravo Partner and Head of the firm’s European Operations Irina Hemmers’ op-ed in the Financial Times. Hemmers laid out a case for the compelling reasons to invest into European software companies. Now that there’s precedent with one of Europe’s largest software companies, Visma, choosing a London listing, perhaps over the coming years more companies will choose Europe — and more investors will buy Europe — in both public and private markets, strengthening the case for alternative asset managers and asset allocators to direct capital to European markets.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know, and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Blackstone (Alternative asset manager) - Private Wealth Solutions - Content Marketing, Vice President - Tokyo. Click here to learn more.

🔍 KKR (Alternative asset manager) - Global Wealth Solutions - Investor Relations - Principal. Click here to learn more.

🔍 Apollo Global Management (Alternative asset manager) - Principal, ABF Credit Risk Manager. Click here to learn more.

🔍 Ares (Alternative asset manager) - Vice President, Product Management & Client Services, Wealth Management Solutions, APAC. Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Strategy & Corporate Development Associate. Click here to learn more.

🔍 Franklin Templeton (Asset manager) - Head of Marketing - France, Benelux, and the Nordics. Click here to learn more.

🔍 BlackRock (Asset manager) - Americas Client Business - Head of AI and Data Transformation. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - RIA, Family Office Business Development - Vice President. Click here to learn more.

🔍 Morningstar (Investment research company) - Senior Product Manager, Public/Private Convergence. Click here to learn more.

🔍 Goldman Sachs Alternatives (Alternative asset manager) - Asset & Wealth Management, Alternative Capital Markets, Liquidity Solutions, Vice President - New York. Click here to learn more.

🔍 Ultimus Fund Solutions (Fund administrator) - SVP, Business Development. Click here to learn more.

🔍 Lincoln Financial (Insurance) - Alternative Investment Sales Specialist Account Executive. Click here to learn more.

🤝 Interested in partnering with Alt Goes Mainstream? 🤝

Alt Goes Mainstream is a community of engaged experts and executives in private markets.

Fill out this form using the link below to explore partnership opportunities.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

📝 Read the news of the week in private markets and wealth management from the first edition of the AGM Alts & Wealth Weekly News Roundup. Read here.

🎥 Watch IEQ Managing Partner and Founder Eric Harrison and iCapital Managing Partner and Co-Head of iCapital Solutions Steve Houston discuss innovative approaches to wealth management live from iCapital Connect. Watch here.

📝 Read The AGM Op-Ed with EQT Partner and Head of Private Wealth Americas Peter Aliprantis on why now is a “inflection point for private wealth.” Read here.

🎥 Watch Blue Owl’s MD, Head of Alternative Credit Ivan Zinn unpack private credit and why ABF has become a prominent part of the private credit ecosystem. Watch here.

📝 Read The AGM Op-Ed with Blue Owl Head of Alternative Credit Ivan Zinn on why “asset-based finance today mirrors the evolution of corporate direct lending from over a decade ago.” Read here.

🎥 Watch Lincoln Financial’s EVP and CIO Jayson Bronchetti discuss the role of insurance companies in private markets as he discusses how he manages a portfolio of $300B in assets. Watch here.

🎥 Watch Krilogy’s Partner and CIO John McArthur discuss how an RIA can chart a growth path by building out its private markets capabilities. Watch here.

🎥 Watch New Mountain Capital’s Founder & Chief Executive Officer Steve Klinsky discuss how $55B AUM New Mountain has built a business that builds businesses. Watch here.

🎥 Watch Arcesium’s Private Markets Head Cesar Estrada discuss data silos and technology integrations in private markets. Watch here.

🎥 Watch GeoWealth President & COO Jack Hannah and iCapital SVP, Partnerships Michael Doniger discuss the ground-breaking BlackRock, iCapital, and GeoWealth unified managed account partnership live from iCapital Connect. Watch here.

🎥 Watch Goldman Sachs’ Managing Director, Global Head of Alternatives, Third Party Wealth Kyle Kniffen discuss how they are “standing on the shoulders of Goldman Sachs to be a complete partner” for the wealth channel. Watch here.

🎥 Watch Fortress Investment Group Managing Director & Co-Head of Private Wealth Solutions Adam Bobker discuss how Fortress has built a wealth solutions business from a whiteboard, leaning on the firm’s pioneering history of innovation. Watch here.

🎥 Watch Constellation Wealth Capital President & Managing Partner Karl Heckenberg on why there will be a $1T independent wealth management firm. Watch here.

🎙 Listen to Ted Seides, Founder of Capital Allocators, and I discuss the convergence of the institutional world and the wealth world as we dive into the intersection of private markets and private wealth to kick off a Capital Allocators mini-series on Private Wealth. Listen here.

🎥 Watch BlackRock Managing Director, Co-Head of US Wealth Business, Senior Sponsor for Retirement Business Jaime Magyera and iCapital Chairman & CEO Lawrence Calcano discuss the ground-breaking BlackRock, iCapital, and GeoWealth unified managed account partnership live from iCapital Connect. Watch here.

🎥 Watch EQT Partner & Head of Private Wealth Americas Peter Aliprantis discuss how the firm is bringing EQT’s success to the US wealth market. Watch here.

🎥 Watch KKR Partner & Co-CEO of KKR Private Equity Conglomerate LLC (K-PEC) Alisa Wood discuss how the firm has innovated in private markets, why KKR came up with the Conglomerate structure, and how evergreens can play a role in investors’ portfolios. Watch here.

🎥 Watch Cantilever Group’s Co-Founder and Managing Partner Todd Owens in a live podcast from BTG Pactual’s NYC office share why GP stakes can be the best of all worlds. Watch here.

📝 Read The AGM Op-Ed with Arcesium Private Markets Head Cesar Estrada on the rise of asset-based finance and why it’s the next growth engine for private credit. Read here.

🎥 Watch BlackRock’s Head of the Americas Client Business Joe DeVico, Head of Product for US Wealth & Head of Alts to Wealth Jon Diorio, and Partners Group's Co-Head of Private Wealth Rob Collins discuss their landmark private markets model portfolio partnership that could be the industry’s “iPhone Moment.” Watch here.

🎥 Watch the third episode of Going Public on Alt Goes Mainstream with Evercore ISI Senior MD and Senior Research Analyst Glenn Schorr as we discuss separating the forest from the trees and Glenn’s “Final Four” firms he would pick in honor of March Madness. Watch here.

🎥 Watch Brookfield Oaktree Wealth Solutions CEO John Sweeney discuss how to build a high-performing wealth solutions team and why the word “solutions” matters when working with the wealth channel. Watch here.

🎥 Watch Cerity Partners’ Partner & Chief Client Officer Tom Cohn and Partner Amita Schultes talk about how and why they have combined a leading OCIO with a $100B AUM wealth management practice. Watch here.

🎥 Watch Marc Lipschultz, Co-CEO of Blue Owl, talk about how they have aimed to skate where the puck is going as Blue Owl has grown its AUM to $265B in nine years. Watch here.

📝 Read The AGM Q&A with Blue Owl Co-CEO Marc Lipschultz, where he highlights some of the trends that have propelled alternative asset management into the mainstream: scale, a focus on private credit, and a focus on private wealth. Read here.

🎙 Listen to Stephanie Drescher, Partner & Chief Client & Product Development Officer of Apollo, discuss what is safe and what is risky as she dives into both the convergence between public and private and the nuances of asset allocation. Listen here.

🎥 Watch Mike Tiedemann, CEO of $72B AUM AlTi Global share why being a global wealth manager can be a differentiator. Watch here.

🎥 Watch Joan Solotar, Global Head of Private Wealth Solutions at Blackstone share why it’s not even early innings, but that it’s “spring training” for private markets adoption by the wealth channel. Watch here.

🎥 Watch Jeff Carlin, Senior Managing Director, Head of Global Wealth Advisory Services at Nuveen live from Nuveen’s nPowered conference on why “it’s all about the end client.” Watch here.

🎥 Watch Venkat Subramaniam, Co-Founder of DealsPlus on building a single source of truth for private markets. Watch here.

🎥 Watch Yann Magnan, Co-Founder & CEO of 73 Strings discuss the opportunity for AI to automate private markets. Watch here.

🎥 Watch Lawrence Calcano, Chairman & CEO of iCapital on episode 14 of the latest Monthly Alts Pulse as we discuss whether or not private markets has moved from access as table stakes to customization and differentiation. Watch here.

🎥 Watch Hamilton Lane Managing Director, Co-Head US Private Wealth Solutions Stephanie Davis and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the third episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch KKR Managing Director, Head of Americas, Global Wealth Solutions (GWS) Doug Krupa and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the second episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch Vista Equity Partners Managing Director, Global Head of Private Wealth Solutions Dan Parant and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the first episode of the Investing with an Evergreen Lens Series. Watch here.

📝 Read about a year in the book of alts — a compilation of the 1,000+ pages written in weekly newsletters on Alt Goes Mainstream in 2024. Read here.

📝 Read about the launch of the AGM Studio, a collaboration between Alt Goes Mainstream and Broadhaven Ventures to incubate, invest in, and help scale companies and funds in private markets. Read here.

🎙 Hear Churchill Asset Management by Nuveen’s MD, Senior Investment Strategist & Co-Head of the Chicago Office Alona Gornick discuss the evolution of private credit, the power of permanent capital, and the importance of the product specialist. Listen here.

🎥 Watch Stepstone Private Wealth CEO Bob Long discuss StepStone Private Wealth’s edge and nuances with their evergreen structures in the first episode of “What’s Your Edge.” Watch here.

🎙 Hear $5B AUM Ritholtz Wealth Management’s Director of Institutional Asset Management Ben Carlson bring a wealth of common sense to asset allocation and private markets. Listen here.

🎙 Hear Blue Owl, Inc. Board Member and Blue Owl GP Strategic Capital Senior Managing Director Sean Ward on how $57.8B AUM Blue Owl GP Strategic Capital has pioneered GP staking and transformed GP stakes into an industry. Listen here.

🎥 Watch Co-Founder & Managing Partner of Cantilever Group and former Goldman Sachs and Broadhaven Capital Partners Partner Todd Owens discuss the middle market opportunity in GP stakes investing. Watch here.

🎙 Hear Intapp’s President, Industries, and Co-Founder of DealCloud by Intapp Ben Harrison discuss how data and automation are transforming private markets. Listen here.

🎙 Hear Bernstein Private Wealth Management’s CIO Alex Chaloff discuss how a $125B wealth manager navigates private markets. Listen here.

🎙 Hear me discuss why and how alts are going mainstream on The Compound’s Animal Spirits podcast with Ritholtz Wealth’s Michael Batnick and Ben Carlson. Listen here.

🎙 Hear Manulife’s Global Head of Private Markets Anne Valentine Andrews share how to approach building a private markets investment platform at an industry behemoth and the merits of infrastructure investing. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, on the AGM podcast discuss driving efficiency across the entire value chain to transform private markets. Watch here.

🎙 Hear Blue Owl’s Global Private Wealth President & CEO Sean Connor share insights and lessons learned from working with the wealth channel. Listen here.

🎙 Hear Ritholtz Wealth Management’s Managing Partner Michael Batnick share views on how wealth managers are navigating private markets. Listen here.

📝 Read about the evolution of GP stakes, why alternative asset management business models are better than SaaS, and our partnership with Todd Owens and David Ballard at Cantilever, a mid-market GP stakes firm anchored by BTG Pactual. Read here.

🎙 Hear how Chris Long, Chairman, CEO, and Co-Founder of Palmer Square Capital Management has built a $29B credit investment firm and a winning NWSL soccer franchise, the KC Current. Listen here.

🎙 Hear stories from building market-defining companies Blackstone, Airbnb, and private markets from Laurence Tosi, former CFO of Blackstone and Airbnb and Managing Partner & Founder of $7.6B investment firm WestCap. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with both a macro and VC lens. Listen here.

📝 Read how 73 Strings CEO & Co-Founder Yann Magnan and team are leveraging AI to build a modern and holistic monitoring and valuation platform for private markets in The AGM Q&A. Read here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, discusses how they approach alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Ryan McCormack, Nick Owens, and Michael Rutter for their contributions to the newsletter.