AGM Alts Weekly | 5.3.26: Alternative asset managers in three charts

AGM Alts Weekly #153: Making private markets more public, every week.

“Alt Goes Mainstream is category of one.” Global Head of Marketing & Communications, $X00B AUM alternative asset manager.

“When it comes to the intersection of alternative investments and wealth management, Michael just gets it.” CIO, $18B AUM RIA.

Presented by

For too long, private equity funds have relied on manual processes — spreadsheets, scattered documents, disjointed data — to track complex investment and ownership structures. It’s slow, error-prone, and not scalable. And when regulators, investors, or auditors come knocking, it’s a fire drill every time.

At DealsPlus, we help private equity funds digitise investment and ownership structures, eliminating data silos. Our software helps power key workflows such as: quarterly reporting, audits, compliance, and exits.

Good afternoon from Washington, D.C.

The performance of the publicly traded alternative asset managers has reflected both the opportunities and challenges that private markets has faced over the past quarter.

Recent months have been defined by volatility, change, and uncertainty. Some asset managers and LPs have been able to cut through the noise. But it has not been an easy period to navigate for GPs and LPs alike.

With so many firms reporting earnings or sharing recent investor presentations, I thought it could be useful to highlight three charts from each of the many publicly traded firms’ recent presentations that provide an interesting perspective or unique insight on the present and future of private markets.

Let’s dive in.

Blackstone

First Quarter 2026 Results (April 23, 2026) presentation here.

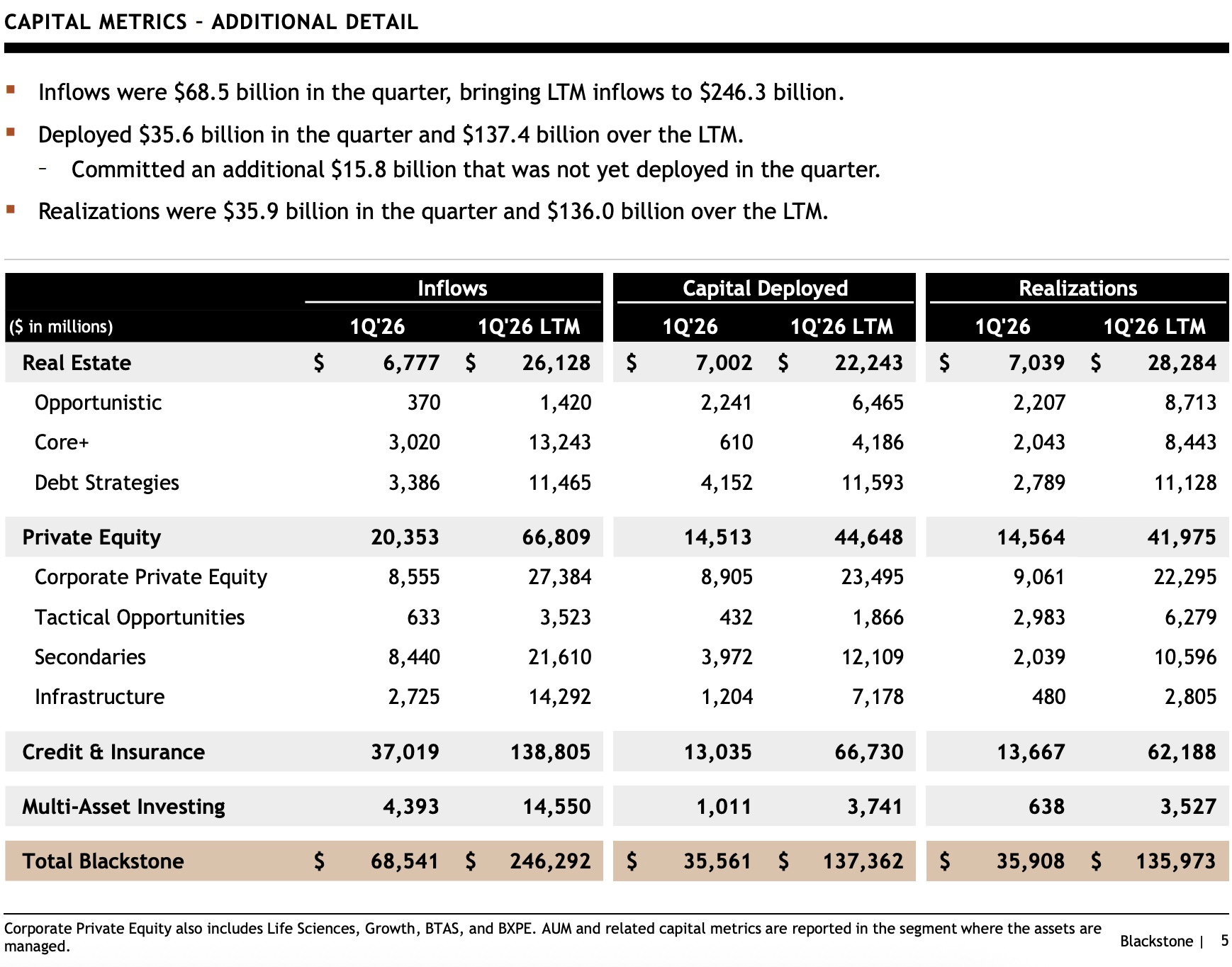

The chart: Blackstone saw $68.5B of inflows in the quarter, bringing LTM inflows to $246.3B. Inflows in Credit & Insurance were $37.02B in Q1 despite the headlines around private credit.

The takeaway: Despite a more challenging environment for alternative asset managers, Blackstone had meaningful inflows in Q1, with institutional and insurance capital exhibiting strong demand in areas including credit. Secondaries and Corporate Private Equity stand out as strategies with strong inflows over the past year, reflecting LP demand for these strategies.

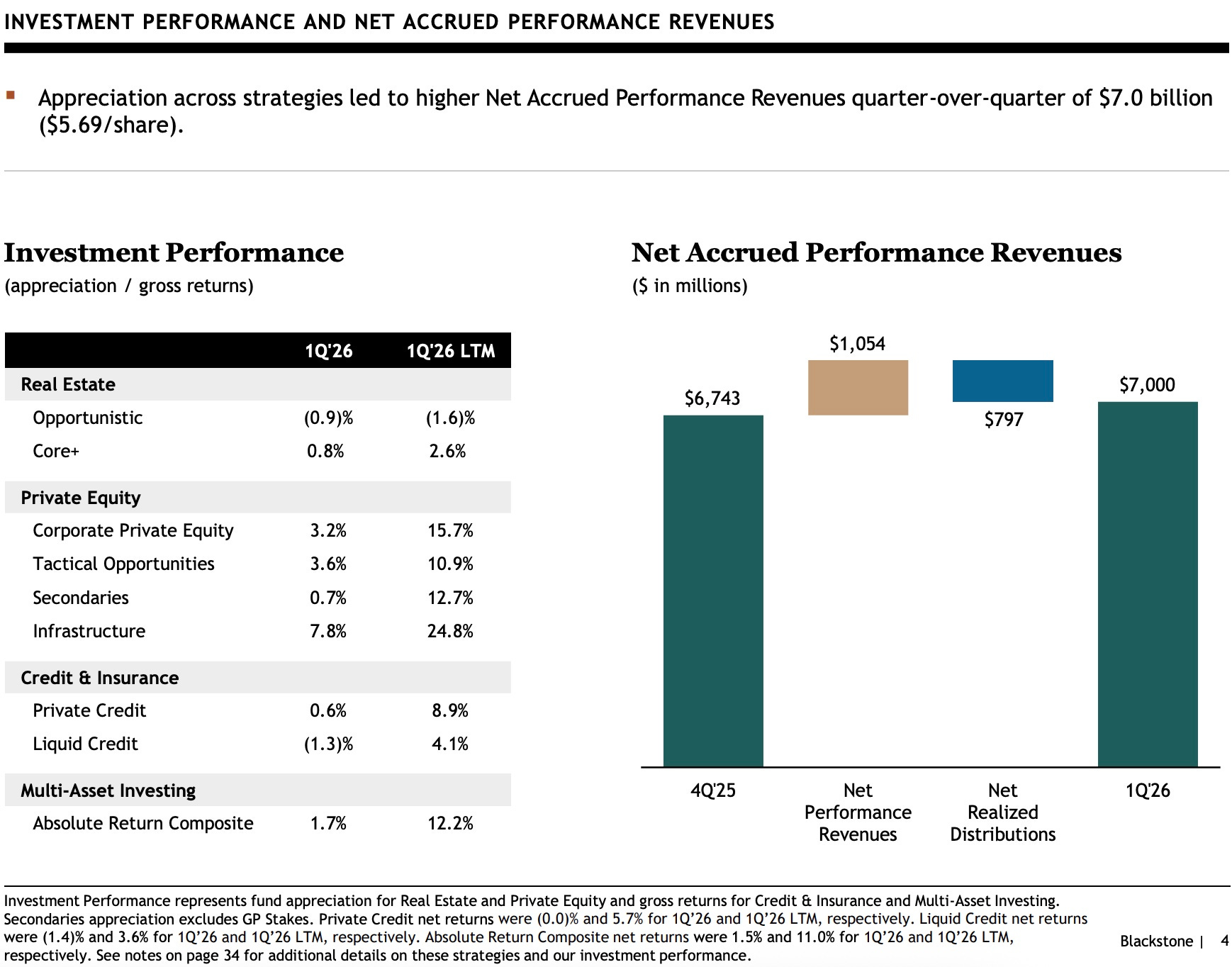

The chart: Investment performance in strategies including Infrastructure (7.8% in Q1) and Corporate Private Equity (3.2% in Q1) garner attention.

The takeaway: Infrastructure’s performance in the quarter and over the last twelve months can help explain why the asset class has caught institutional and wealth LP’s attention. The size and scale of the opportunity must also be noted. In Blackstone President & COO Jon Gray’s recent “Market Views” session from April, he shared that Blackstone has “made a strategic decision to try to be the biggest investor in AI infrastructure in the world.” Gray said that Blackstone will sign “6 gigawatts of leases for data centers … which will represent $100B of spend on data centers, mainly in the US.”

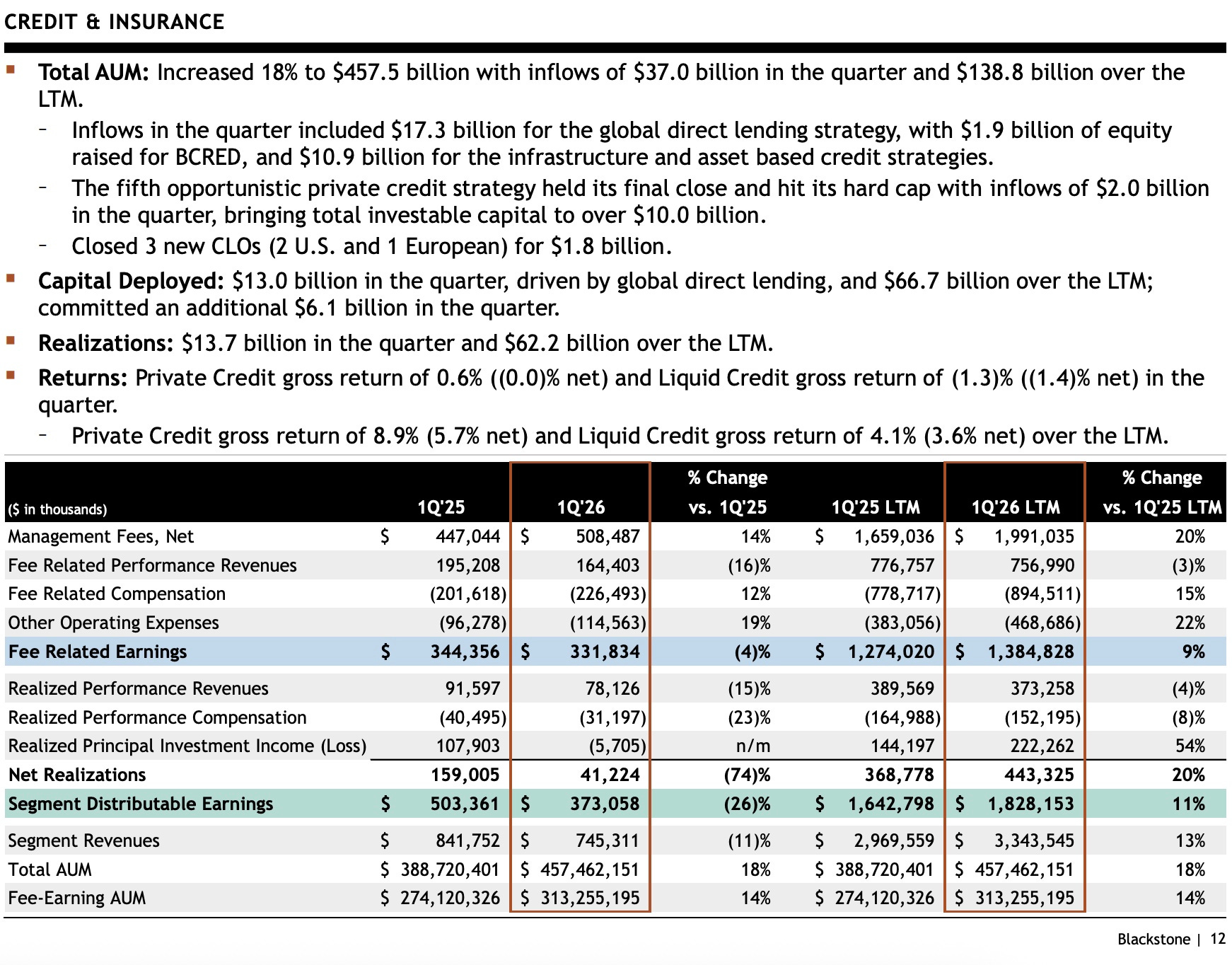

The chart: Blackstone’s Private Credit business saw $17.3B of inflows for its global direct lending strategies, including $1.9B of capital raised for BCRED, its evergreen credit fund. Infrastructure and asset-based credit strategies also had meaningful fundraising figures.

The takeaway: Despite the headwinds and headlines in private credit, Blackstone raised meaningful capital in private credit, particularly in asset-based finance, and saw institutional LPs continue to allocate to credit.

KKR

Overview Presentation - 4Q’25 (March 24, 2026) presentation here (note: KKR’s Q1 earnings presentation is on May 5, 2026, so this newsletter will include the latest Investor Presentation from March 2026 instead).

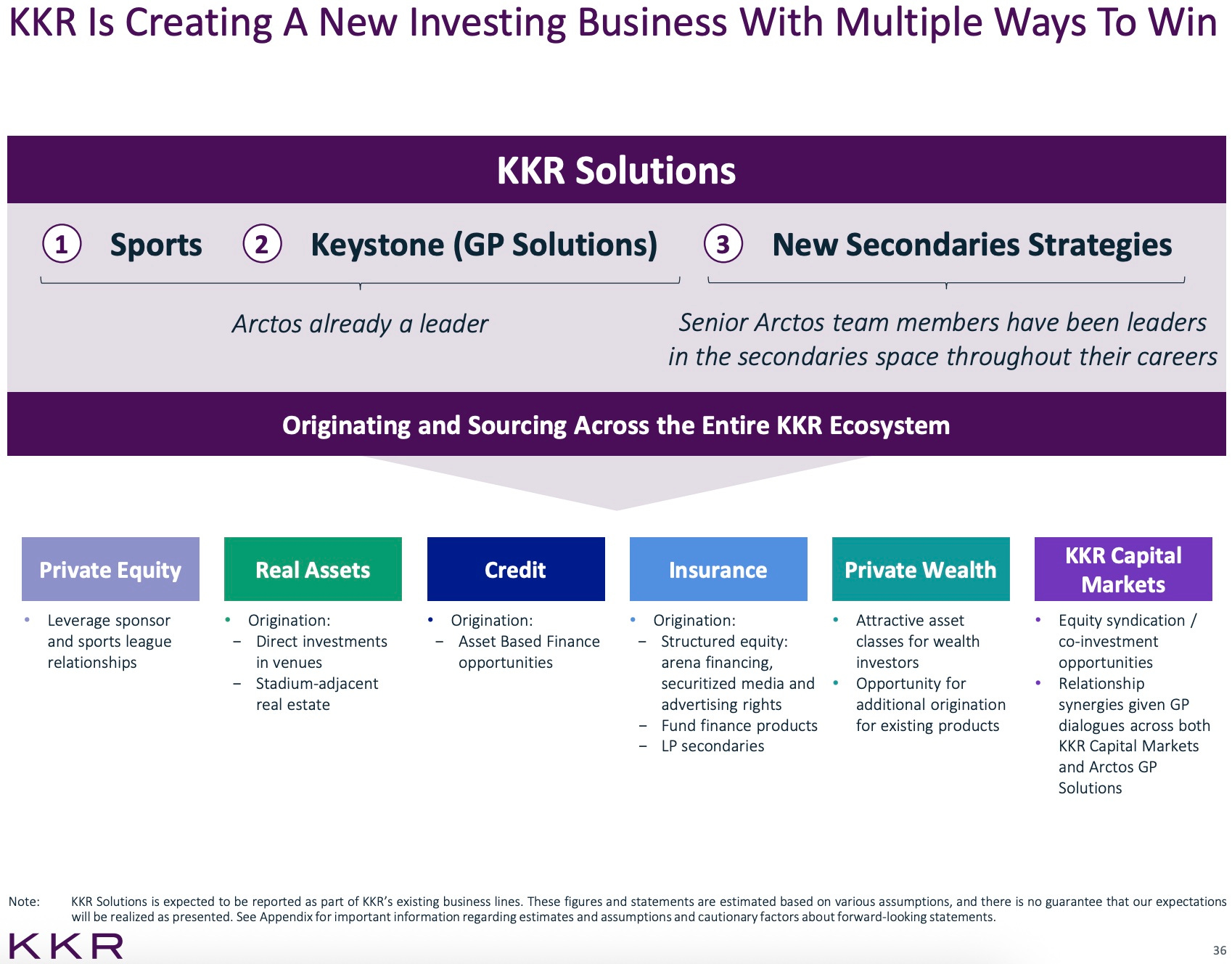

The chart: KKR acquired Arctos, a $15B alternative asset manager that is a market leader in Sports and GP Solutions (Keystone) in February for up to $1.4B. Arctos will also enable KKR to expand into secondaries strategies.

The takeaway: Sports and GP Solutions provide interesting complements to KKR’s existing diversified private markets platform, but the really intriguing aspect of their acquisition of Arctos is the ability to expand into secondaries. KKR noted that they expect KKR Solutions (across Sports, GP Solutions, and Secondaries) to be a $100B AUM business over time, as I wrote about in the 2.8.26 AGM Alts Weekly. Secondaries has the chance to be a growth strategy in a growth industry, and coupled with KKR’s sizable wealth distribution team, it is not hard to see secondaries becoming a major part of KKR’s $744B+ AUM platform going forward.

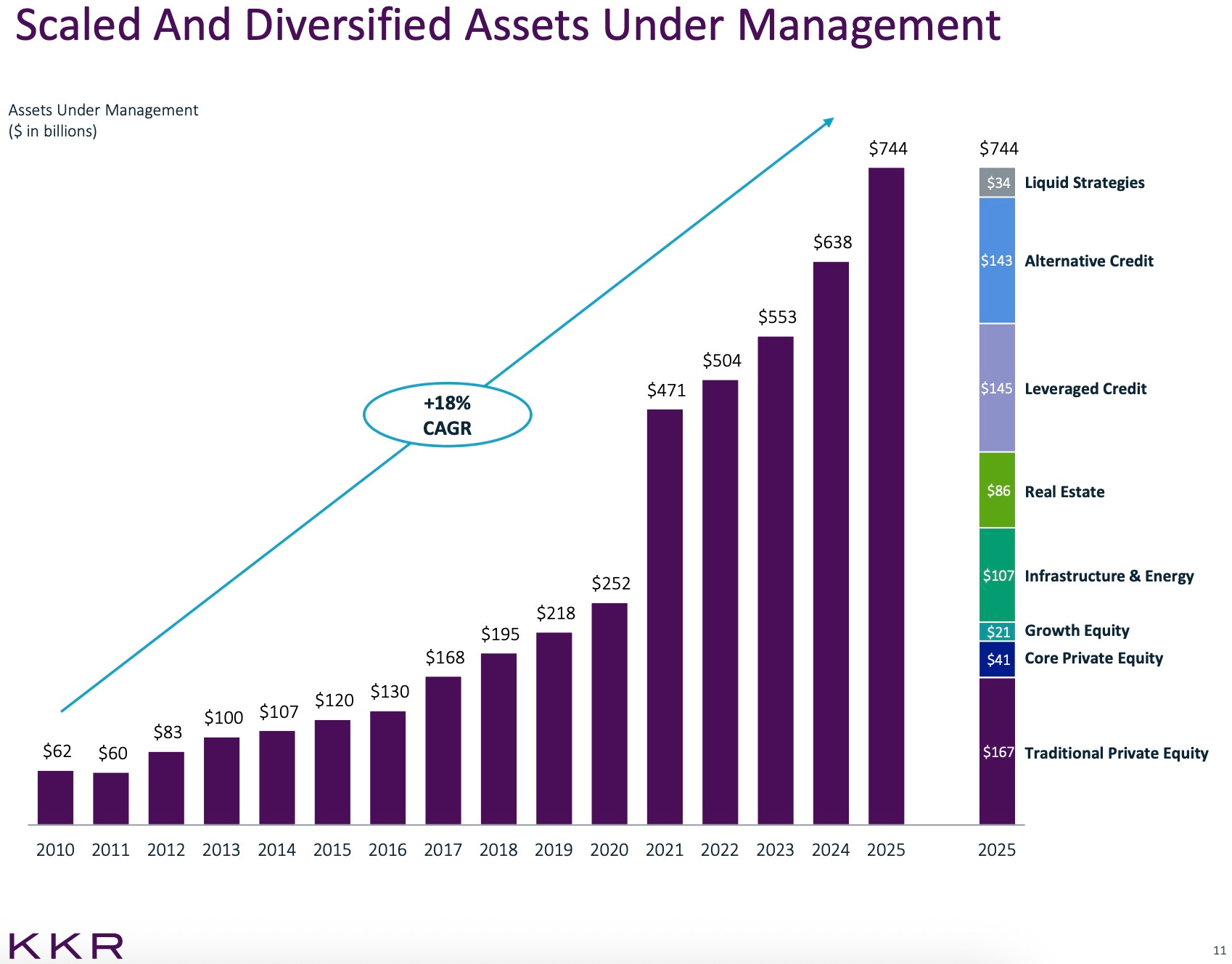

The chart: KKR’s AUM crossed $744B AUM by the end of 2025, with the firm’s remarkable growth since 2018 representing an 18% CAGR.

The takeaway: Traditional Private Equity ($167B AUM, and $229B if Growth Equity and Core Private Equity are included) still represents the largest portion of KKR’s AUM, staying true to the firm’s roots as they celebrated their 50th anniversary this past week. The firm has built out a diversified platform across PE, Infrastructure, Real Estate, and Credit with no single strategy representing the lion’s share of the firm’s AUM.

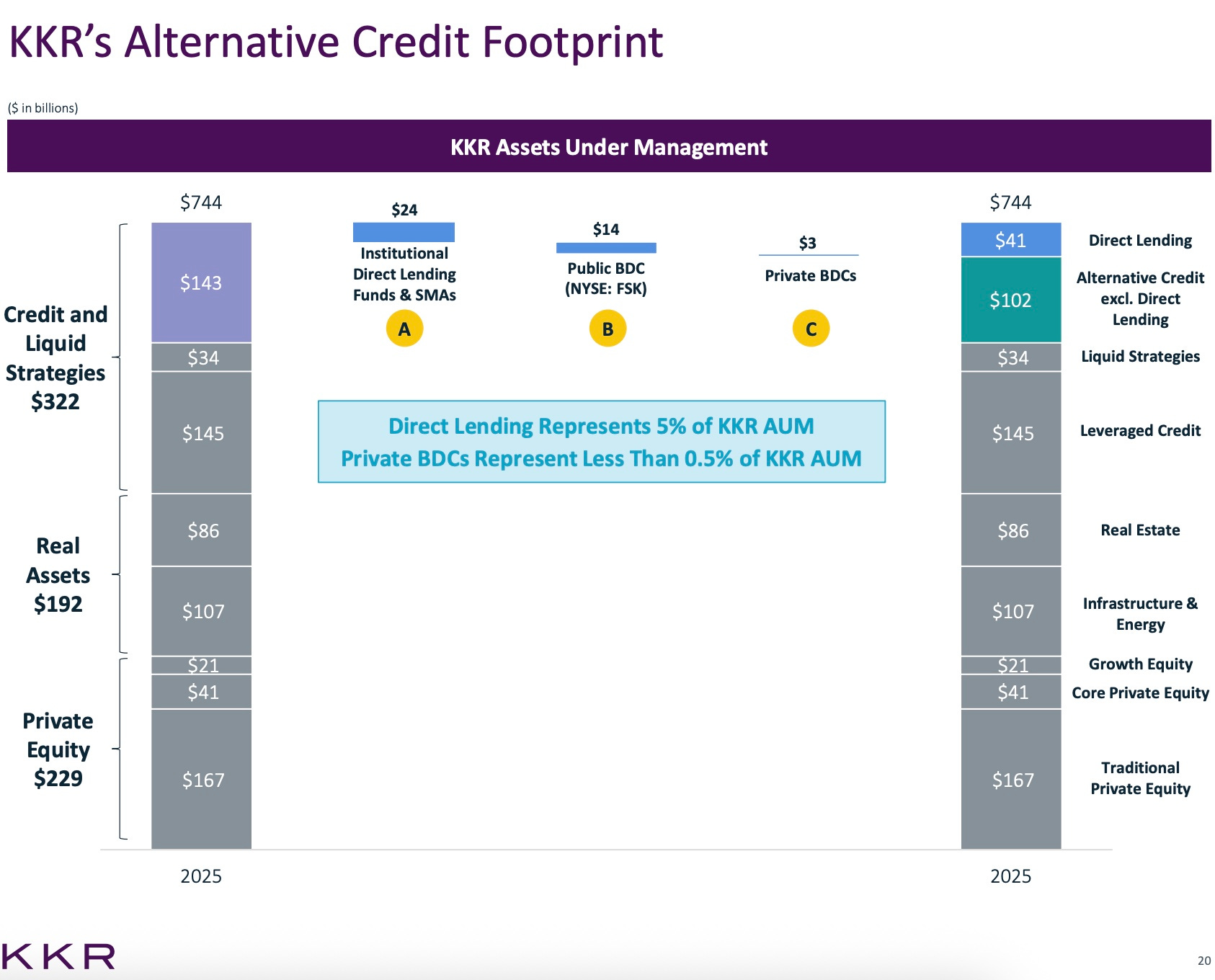

The chart: Direct lending represents 5% of KKR AUM. Private BDCs represent less than 0.5% of KKR’s AUM.

The takeaway: While direct lending has captured much of the attention in the press, direct lending represents a small portion of many of the alternative asset managers’ total AUM. This slide serves as a reminder that firms with a diversified investment platform will benefit from market cycles, press cycles, and challenges in certain asset classes due to diversification of products and investment strategies.

Brookfield

Investor Presentation February 2026 here (note: Brookfield’s Q1 earnings presentation is on May 8, 2026, so this newsletter will include the latest Investor Presentation from February 2026).

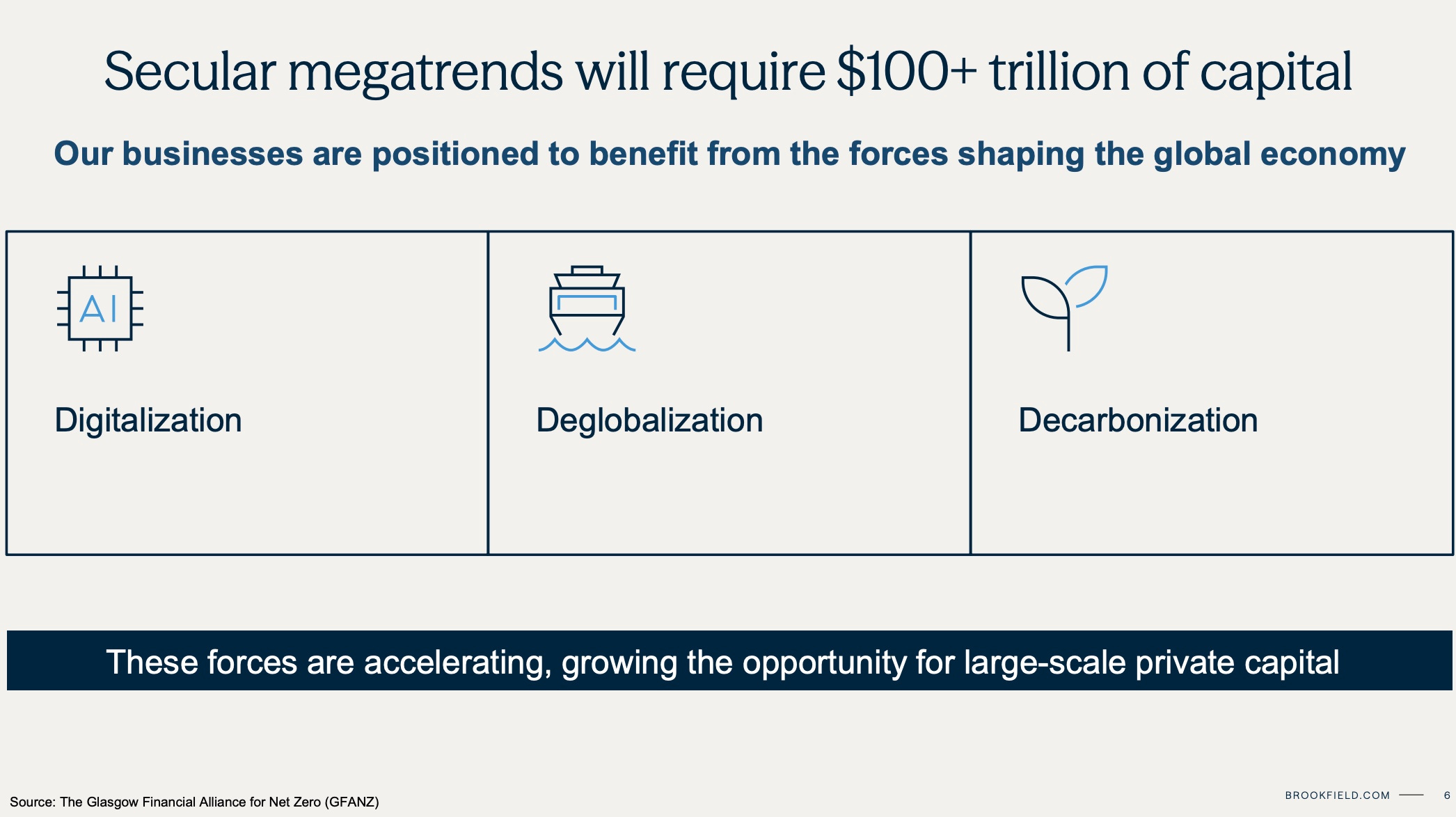

The chart: Megatrends across digitalization, deglobalization, and decarbonization require $100T of capital, according to Brookfield Asset Management.

The takeaway: Scaled investment firms that have the brand, platform, and resources to attract large quantums of capital from institutional and wealth channel investors will be in pole position to finance many of these megatrends.

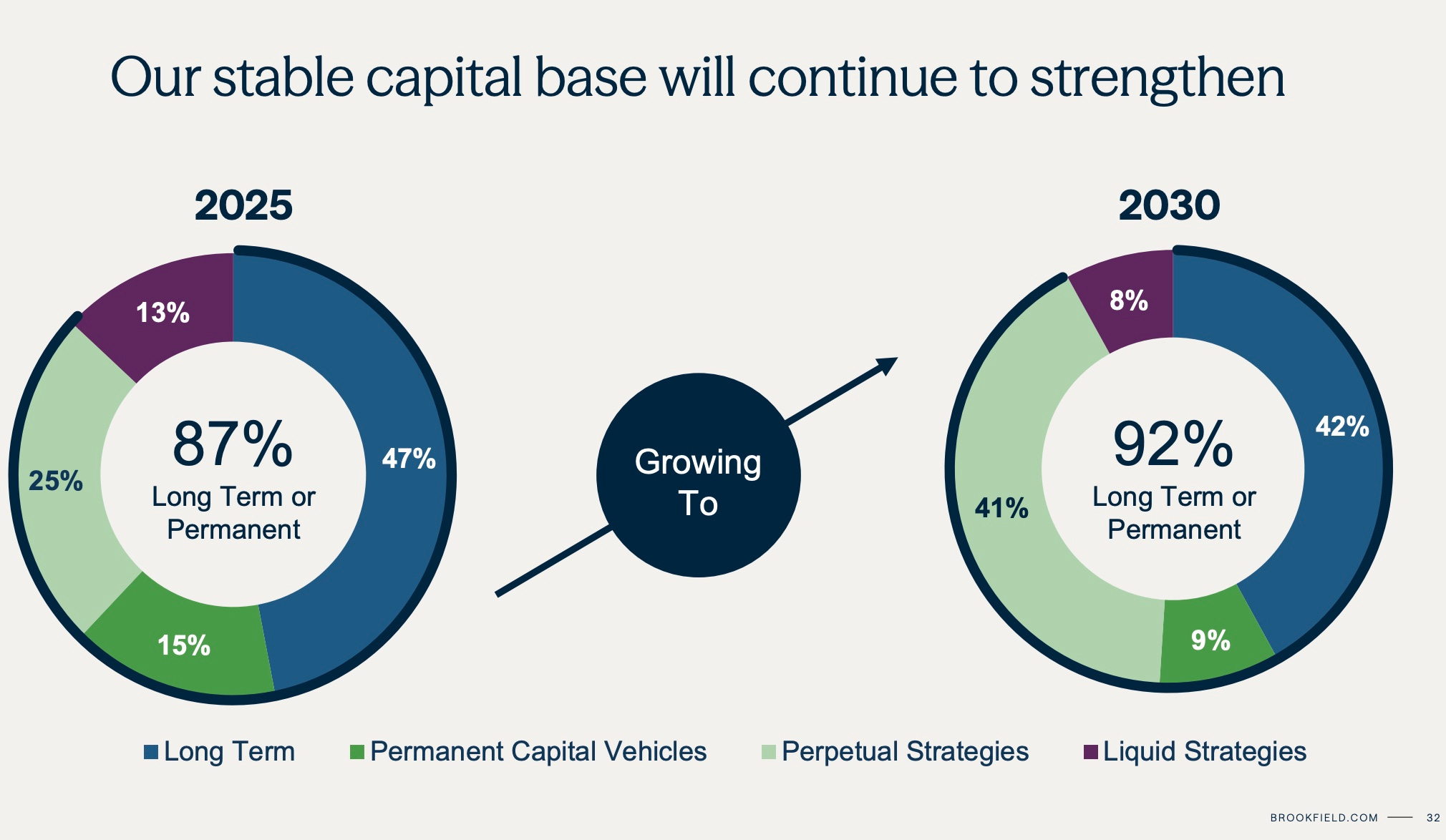

The chart: BAM expects to increase the percentage of its long-term or permanent capital from 87% to 92% by 2030.

The takeaway: Long-term or permanent capital means a few things: one, that BAM anticipates that an increasing portion of the firm’s capital will likely come from evergreen vehicles (and likely wealth channel investors) and, two, this long-term and permanent capital base is well-suited to invest into megatrends that require long-term capital, particularly as it relates to infrastructure, real estate, and private equity. It’s also worth noting that a meaningful portion of BAM’s capital comes from the firm’s balance sheet.

The chart: BAM sees continued growth from institutional investors, even as the firm and its peers expands its presence in the wealth channel.

The takeaway: Institutional investors will still continue to remain the largest source of capital for many alternative asset managers, even as they continue to focus on wealth channel investors. It will be important for alternative asset managers to figure out how to harmonize their fundraising efforts across institutional and wealth channel LPs, and firms that do so will benefit from increased connectivity across its fundraising (and marketing) teams.

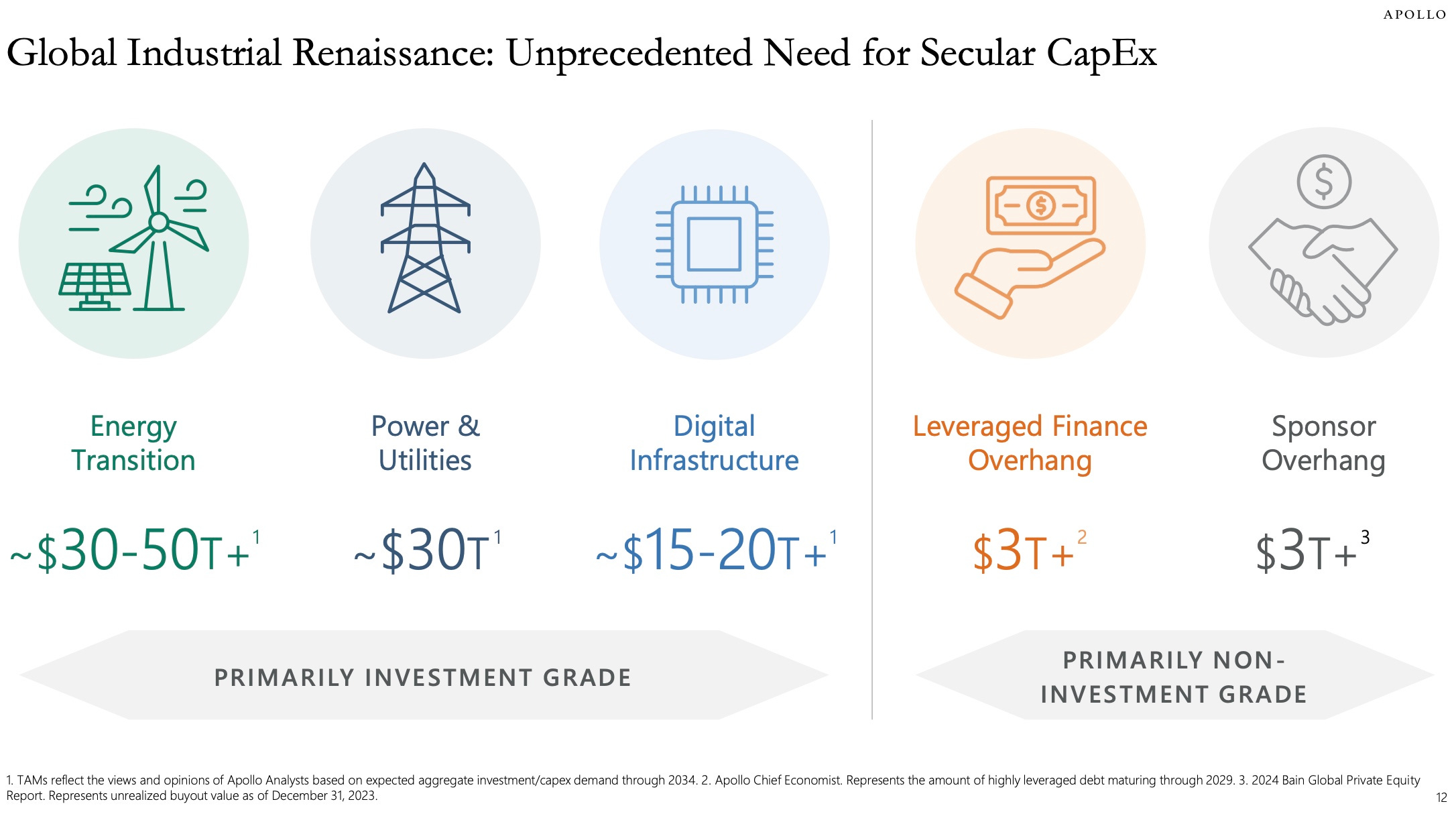

Apollo

Investor Presentation February 2026 here (note: Apollo’s Q1 earnings presentation is on May 6, 2026, so this newsletter will include the latest Investor Presentation from February 2026 instead).

The chart: Investing in megatrends that require trillions of dollars of capital to finance themes such as the energy transition, power generation, and digital infrastructure is a recurring theme for the industry’s largest alternative asset managers.

The takeaway: Firms that have the ability to invest into investment grade solutions will have the scale to pursue these investment opportunities. They will also have the platform and relationships across both institutional and wealth channels to raise the capital required to finance these opportunities.

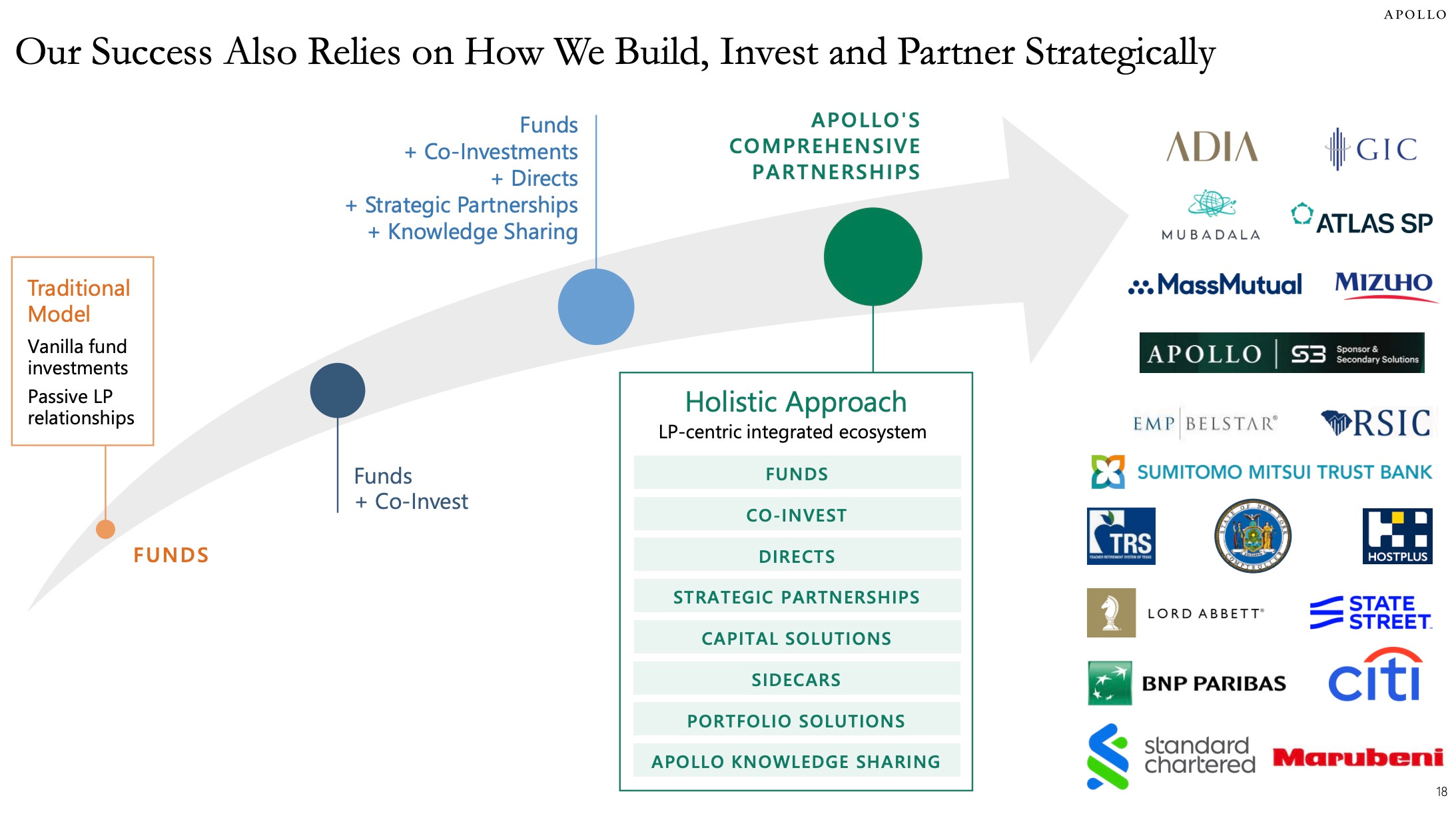

The chart: The chart below is emblematic of a broader industry evolution. As the largest alternative asset managers become “one-stop-shops,” their business strategy is focused on becoming a solutions provider for LPs.

The takeaway: LPs are increasingly looking to do more with less managers. The firms that have the scaled platforms and capabilities to serve investors with what Apollo calls a “holistic approach” will be likely winners with institutional and wealth channel LPs. This feature can perhaps explain why the largest alternative asset managers are so focused on building their brands. Firms will win LP relationships and trust on brand, and, of course, performance … but as the following slide will show, there will be equity and fixed income alpha, but also equity and fixed income beta across private markets. There will be cases where LPs choose private equity or private credit beta for their portfolio. The next question for LPs? Will they look to partner with firms that have a multi-manager platform approach or with a single firm and its brand?

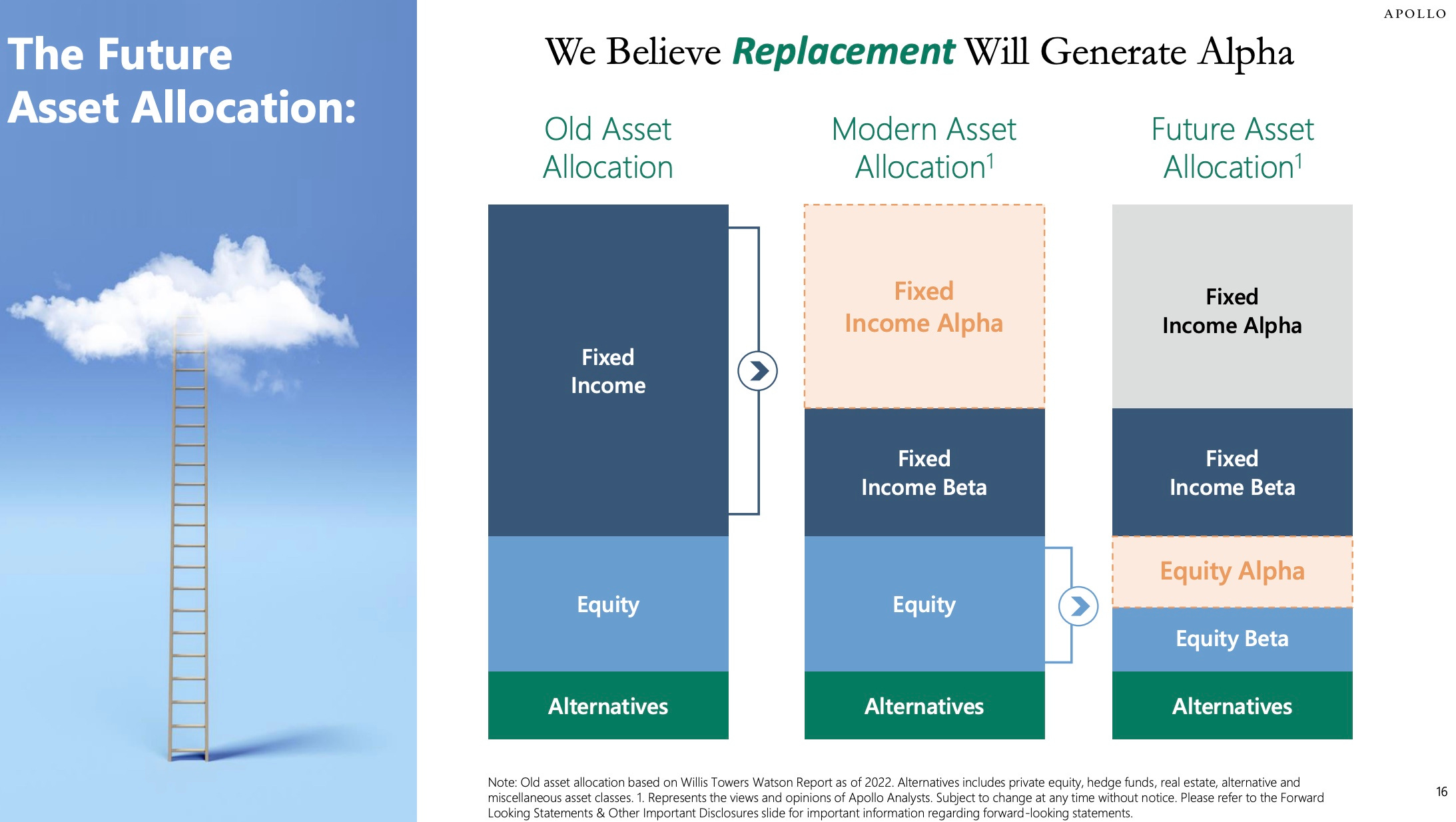

The chart: Apollo believes that asset allocation is changing. Fixed income will evolve into fixed income alpha and fixed income beta. Same with equity.

The takeaway: If asset allocation is evolving, so too will innovation around product construction and delivery of total portfolio solutions. In the wealth channel, model portfolios that incorporate this modern and future asset allocation framework will become more commonplace as the technology continues to improve to enable for rebalancing of exposures across a portfolio in evergreen fund structures.

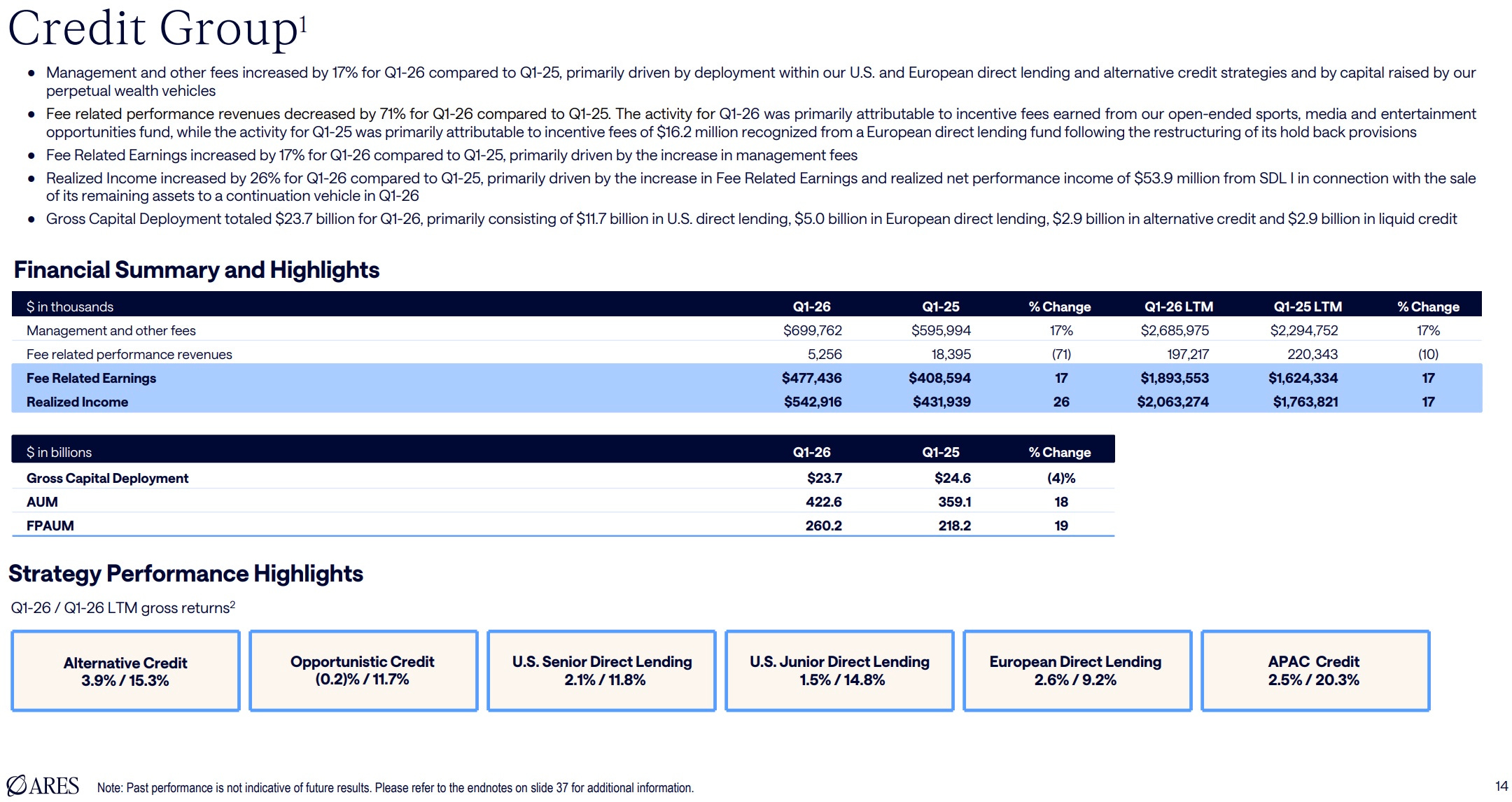

Ares

First Quarter 2026 Results presentation here.

The chart: Ares achieved $29.5B in gross new capital commitments in Q126, a 46% increase compared to Q125.

The takeaway: $20.4B of its $29.5B in capital raised in Q126 flowed into credit strategies, with US Direct Lending raising $9.5B and European Direct Lending raising $4B. Ares CEO Michael Arougheti said that institutional investors in particular are not shying away from allocating in this current market. He said, “everything we’re seeing on the ground is that the institutional investor is not anxious. They’re not allocating away from private credit. In fact, I think they are looking at this as a huge opportunity to take advantage of a bizarre dislocation and bring liquidity into the market to capture excess return.”

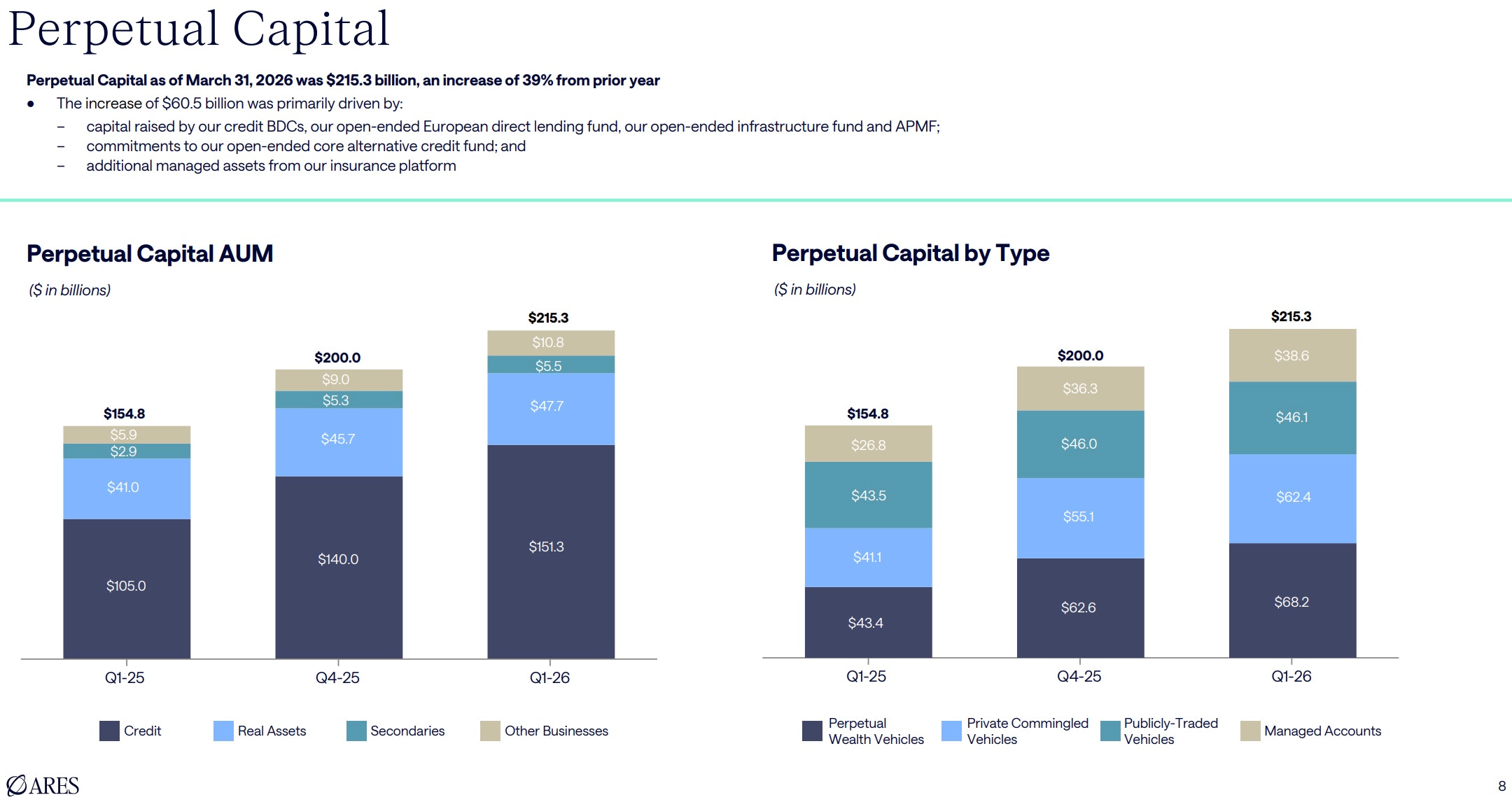

The chart: Ares has continued to see an increase in AUM within its perpetual wealth vehicles and in credit.

The takeaway: AUM in perpetual wealth vehicles increased from $62.6B in Q425 to $68.2B in Q126. AUM in perpetual wealth vehicles in Q125 was $43.4B.

The chart: Ares’ credit business has continued to grow over the past twelve months. Management fees grew 17%. Notably, performance fee revenue decreased by 71% from Q125 to Q126.

The takeaway: Ares pulled back its gross capital deployment in Q126 by 4% relative to its capital deployment in Q125. Gross performance across its credit strategies over the past twelve months is notable.

EQT

Q1 Announcement 2026 Webcast (April 22, 2026) presentation here.

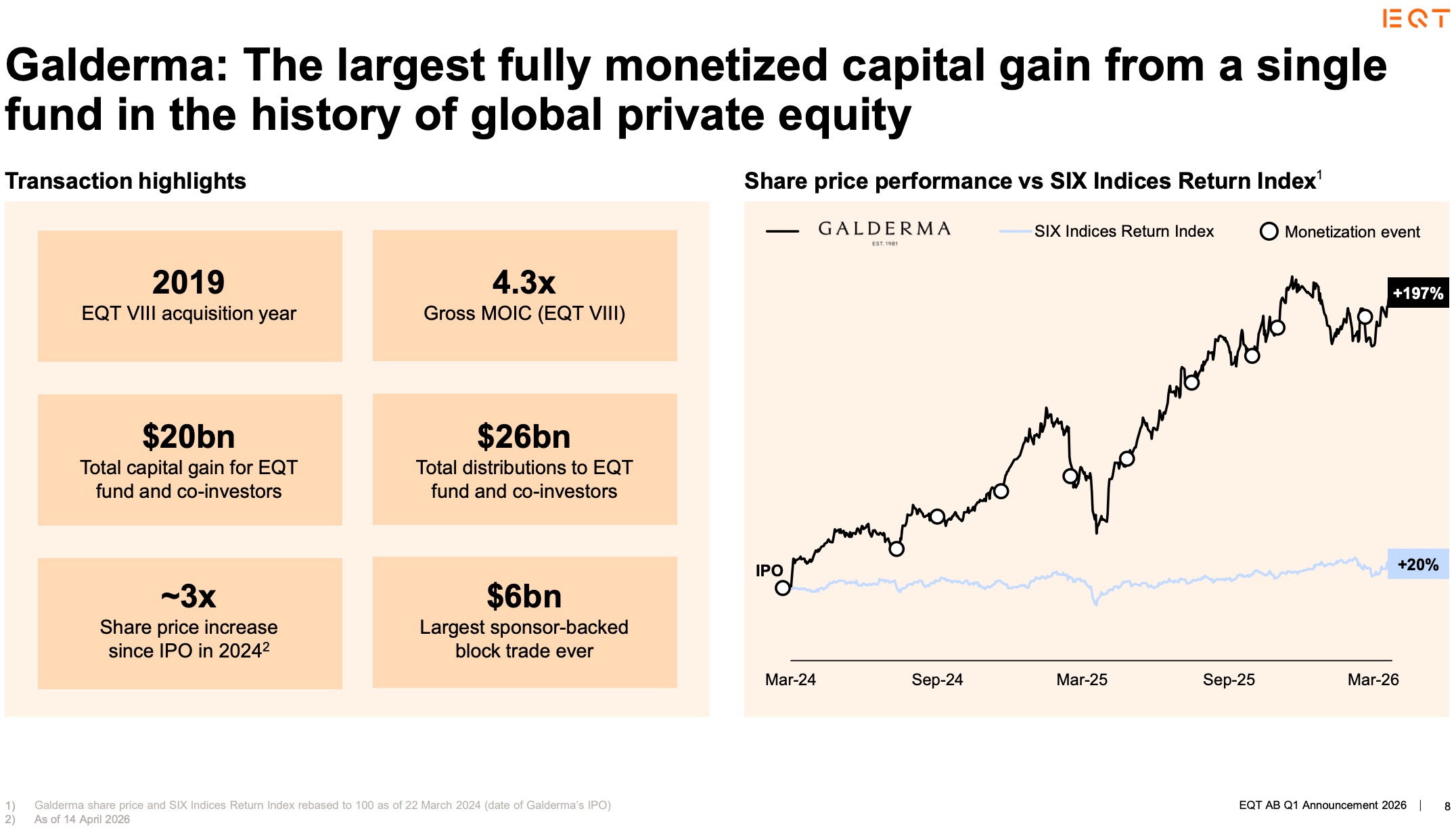

The chart: EQT’s exit of Galderma represented the largest fully monetized capital gain from a single fund in the history of global private equity, generating a $20B capital gain for EQT fund (VIII) and co-investors.

The takeaway: EQT has generated a number of meaningful exits as of late, punctuated by Galderma. IFS has also generated meaningful DPI for EQT. On the EQT earnings call, CEO Per Franzen said the firm is targeting “approximately 30 exit events this year” (note: Franzen said that the “exit pipeline [is] nicely spread across our focus sectors”).

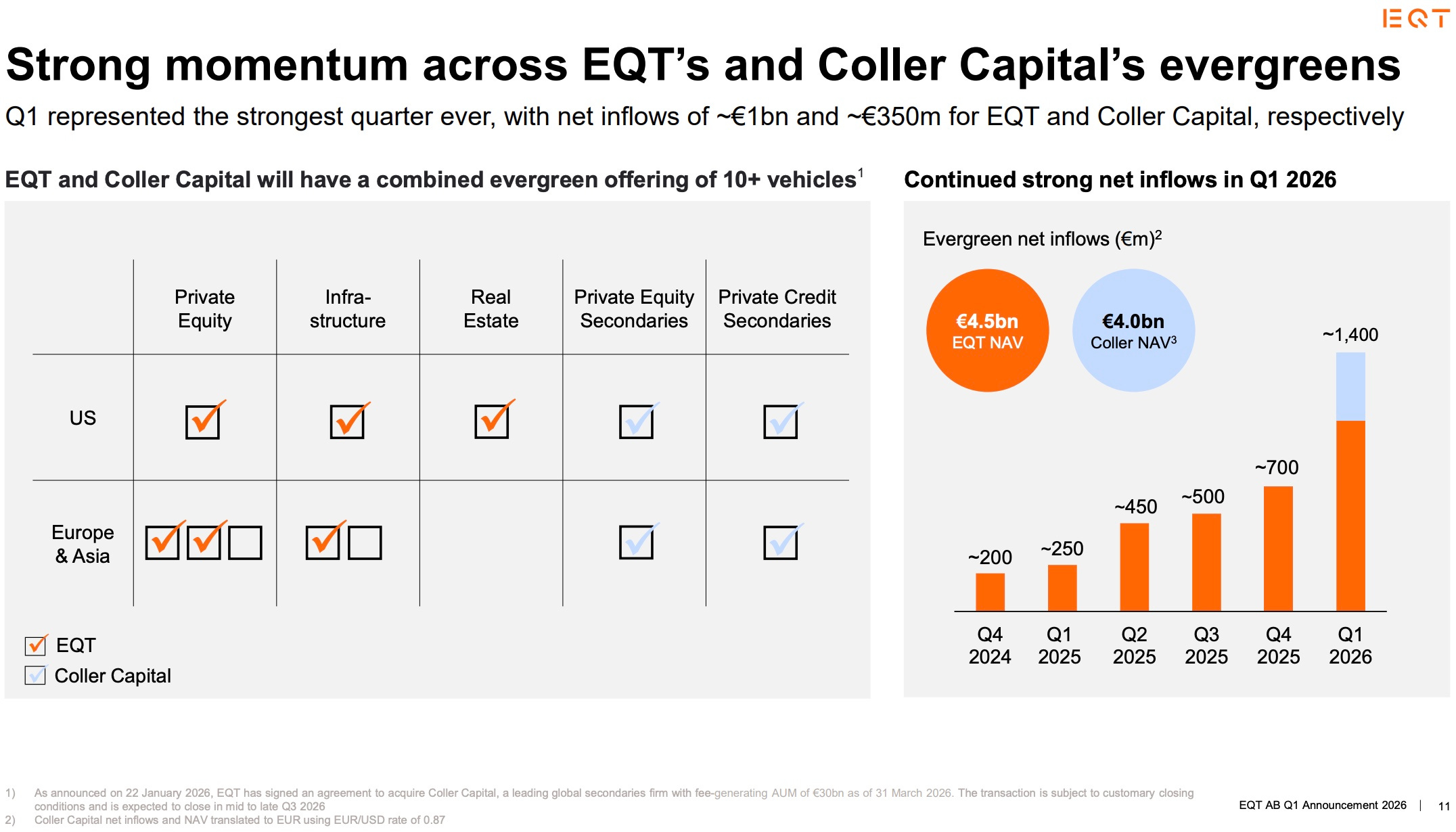

The chart: EQT’s private wealth fundraising had its best quarter on record. EQT’s evergreens generated €1B of inflows and Coller Capital, EQT’s newly acquired secondaries business that will be rebranded as Coller EQT, achieved €350M of inflows.

The takeaway: EQT’s acquisition of Coller has, in part, enabled the firm to double its net inflows from €700M in Q425 to €1.4B in Q126. EQT’s combined evergreen NAV now stands at over €4.5B and Coller’s is at €4B.

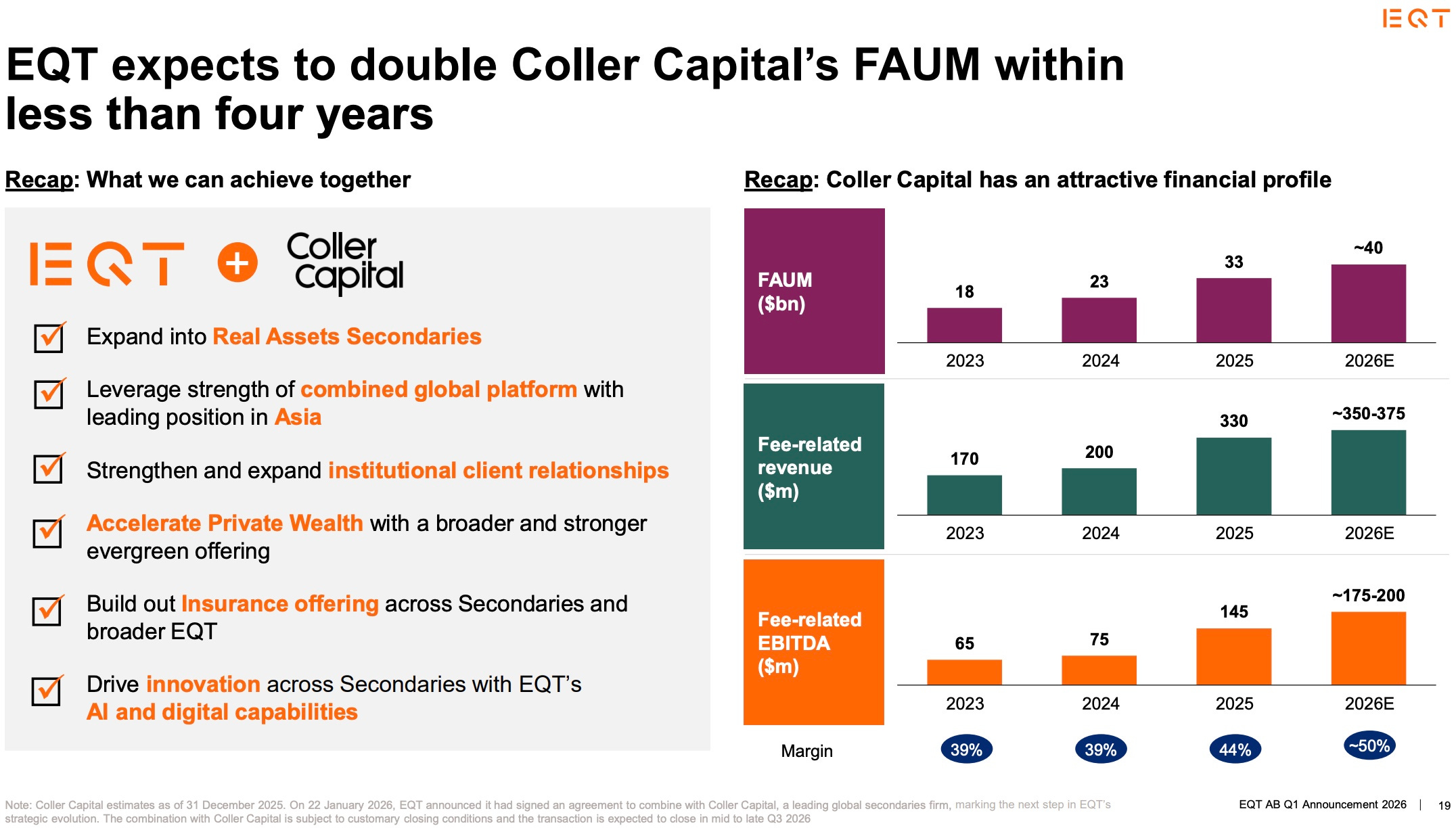

The chart: EQT expects to double Coller Capital’s FAUM within under four years from ~$40B to $80B by expanding into other secondaries strategies, deepening institutional client relationships, and growing its private wealth capabilities.

The takeaway: Secondaries is expected to have another record year of volume in 2026, so EQT is well-positioned to capture a meaningful portion of growth within the secondaries market by adding one of the market leaders Coller Capital to its platform. Coller’s already strong business (expected 50% 2026E fee-related EBITDA margin) should benefit from being part of EQT’s large, global platform, particularly given EQT’s capabilities in private wealth, as I shared in a LinkedIn post about the $3.7B acquisition.

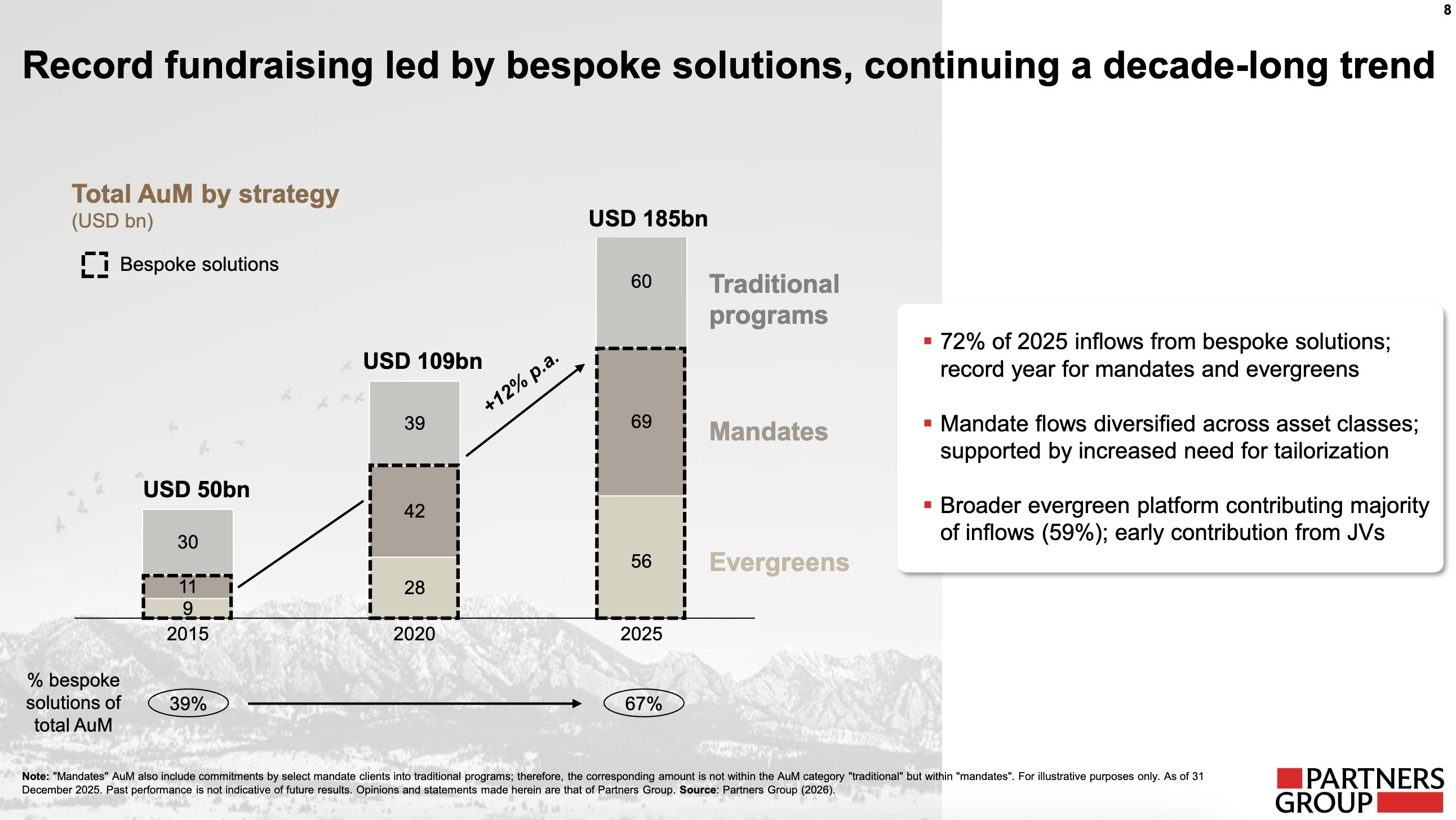

Partners Group

Annual Results 2025 presentation here.

The chart: Bespoke solutions drove Partners Group’s fundraising over the past year. Bespoke solutions represent 67% of Partners Group’s total AUM.

The takeaway: The firm’s continued growth of bespoke solutions for LPs highlights that LPs, particularly institutional LPs, are still very much looking for tailored private markets solutions. This datapoint is promising for the private markets solutions providers, such as Partners Group and its peers, which can continue to provide LPs with diversified and bespoke access to private markets, particularly in the middle-market, where it can be challenging for LPs to source and underwrite managers and co-investments at scale.

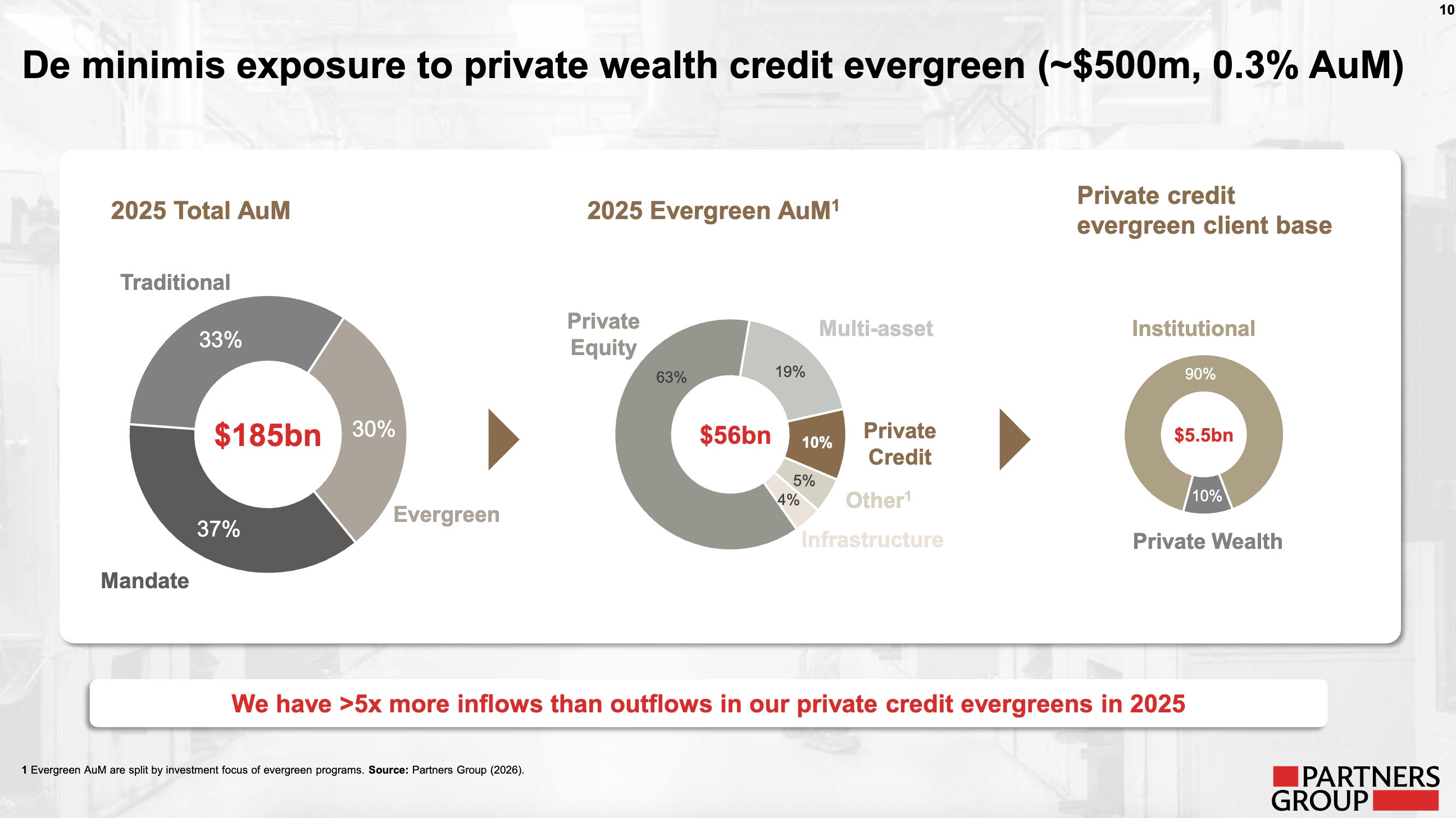

The chart: Partners Group has a small portion of its AUM (0.3% AUM, ~$500M) exposed to private wealth credit evergreen.

The takeaway: Private credit evergreen AUM for Partners Group only represents 10% of the firm’s overall evergreen AUM ($56B) and 0.3% of the firm’s overall AUM ($185B). While Partners Group has been a pioneer in evergreen fund structures, evergreens only comprise 30% of the firm’s total AUM.

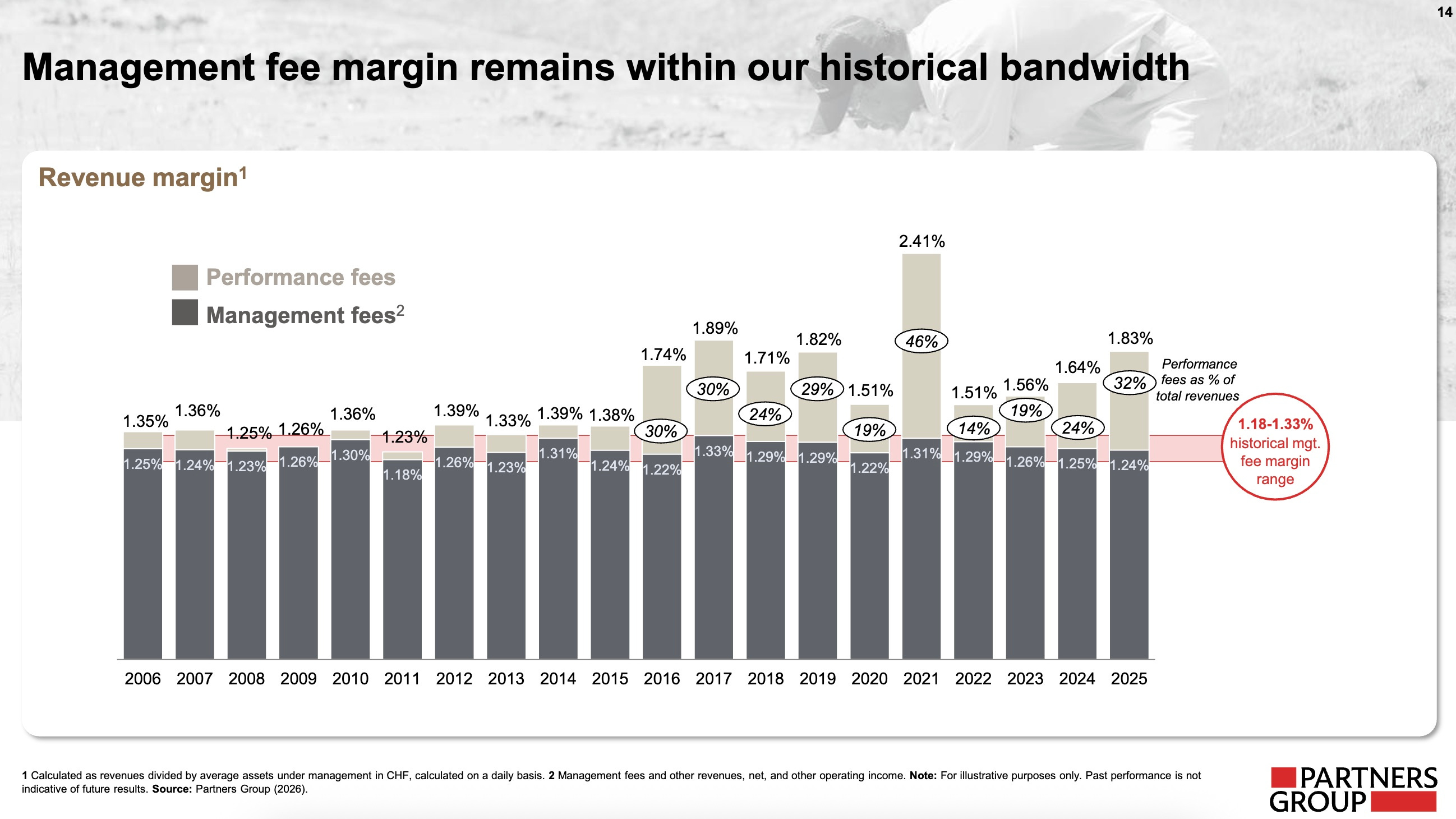

The chart: Management fee margin range has remained steady over the past 19 years for Partners Group, with management fee margin ranging from 1.18-1.33%.

The takeaway: This slide illustrates that alternative asset managers themselves have strong and durable business profiles, largely due to consistent and long-dated “enterprise-like” contractual relationships with LP customers that tend to be repeat customers. This feature of alternative asset managers is one reason why I am constructive on GP stakes as an investment strategy, with alternative asset manager business models being “better than SaaS.”

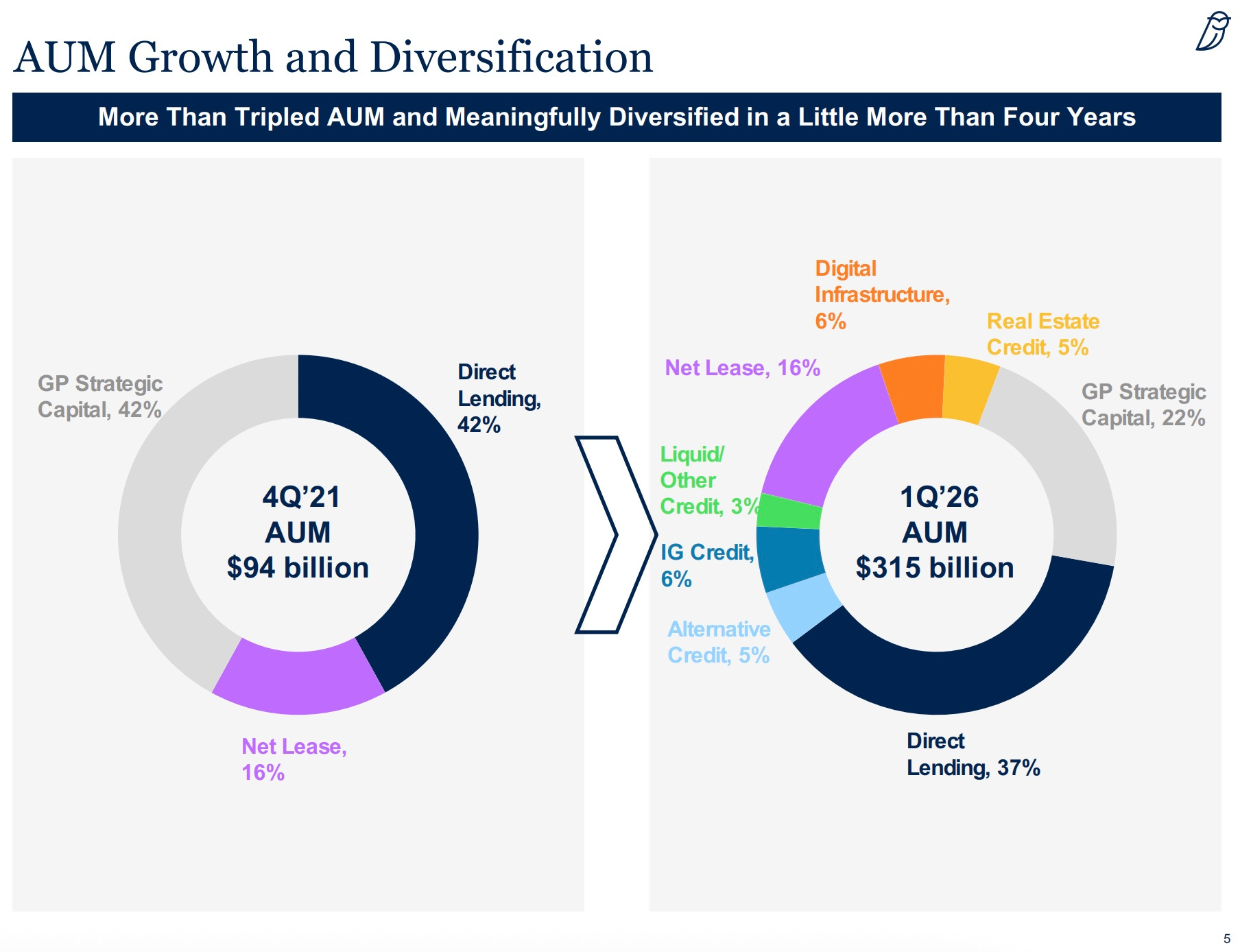

Blue Owl

First Quarter 2026 Earnings (April 30, 2026) presentation here.

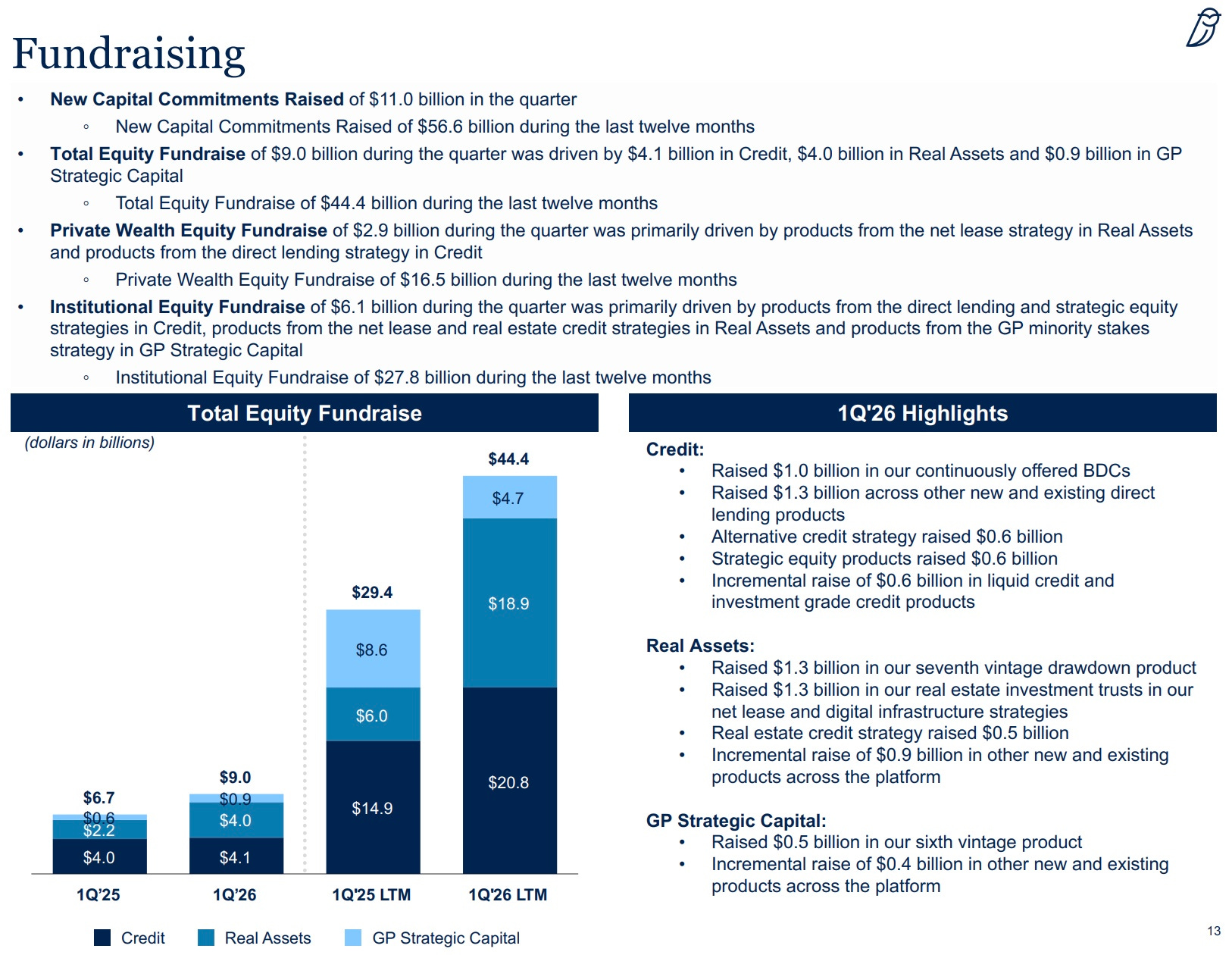

The chart: Blue Owl’s $315B AUM has grown over threefold in four years and is diversified across Credit (mainly Direct Lending), Real Assets (Net Lease, Digital Infrastructure, and RE Credit), and GP Strategic Capital (GP Stakes).

The takeaway: Direct Lending comprises 37% of the firm’s AUM as of 1Q26, down from 42% in 4Q21. It’s worth noting that the firm’s GP stakes strategy, GP Strategic Capital, has some exposure to private credit, albeit indirectly through its minority ownership in a number of the industry’s top private credit firms. Blue Owl is notably missing a private equity strategy for further AUM diversification. Should Blue Owl look to expand into private equity? The firm’s BOSE strategy, a GP-led private equity secondaries strategy that closed on $3B in February 2026, could be a foreshadowing of Blue Owl’s continued expansion into private equity as a way to diversify its platform.

The chart: Blue Owl had $4.1B of inflows coming into Credit, $4B into Real Assets, and $0.9B into GP Strategic Capital.

The takeaway: Private wealth raised $2.9B in the quarter, mainly driven by inflows into the Net Lease strategy and Direct Lending strategy. Institutional LPs contributed $6.1B of inflows in the quarter. Over the past twelve months, institutional LP inflows generated $27.8B, with private wealth inflows reaching $16.5B over the past twelve months.

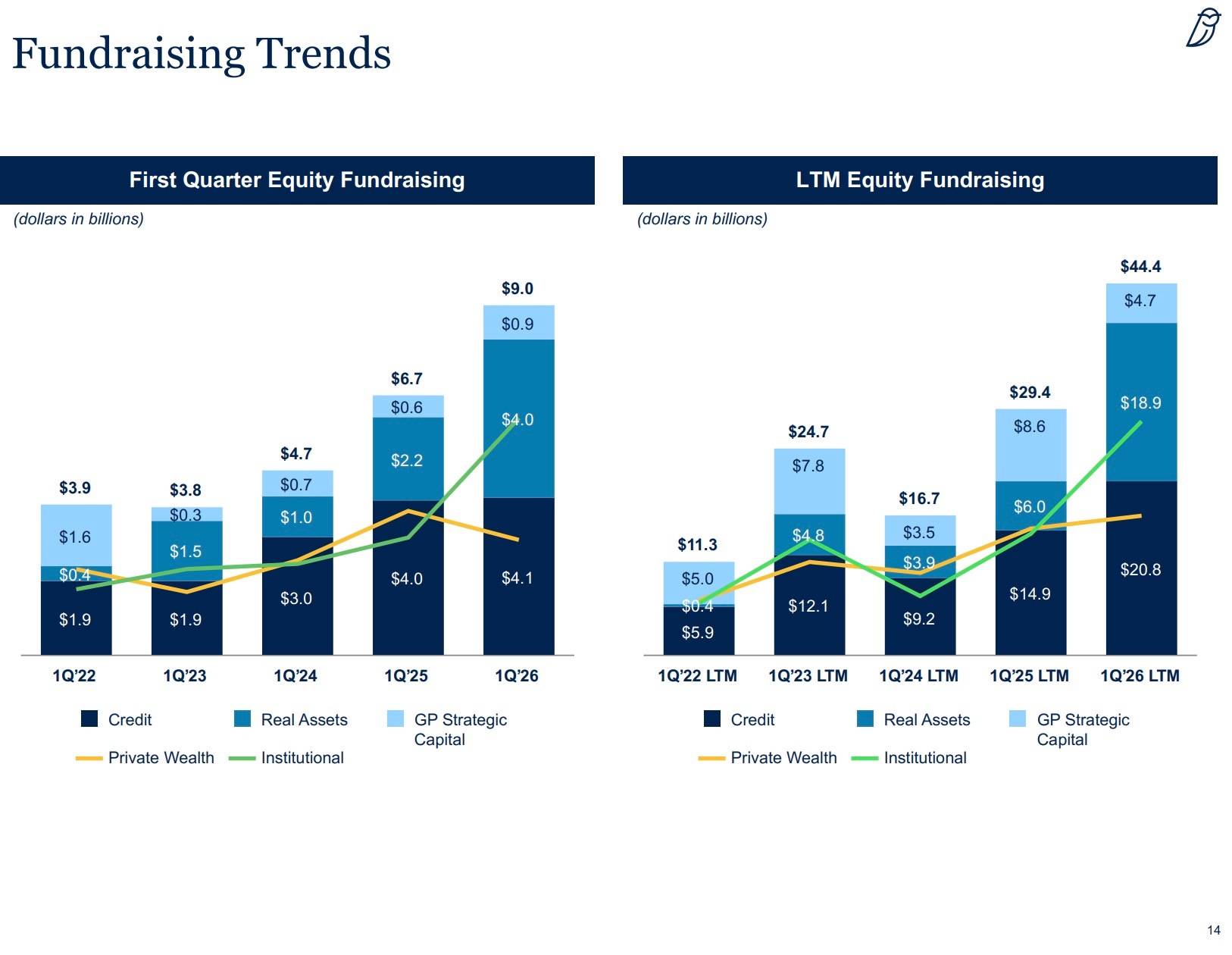

The chart: Private wealth fundraising saw a decline in 1Q26 versus Q125, while institutional fundraising saw a market increase.

The takeaway: While private wealth fundraising declined in 1Q26 compared to 1Q25, inflows from the wealth channel still increased on an absolute basis over the past twelve months. The question going forward? What will private wealth inflows look like in the year ahead, particularly given the firm’s focus on Direct Lending and credit?

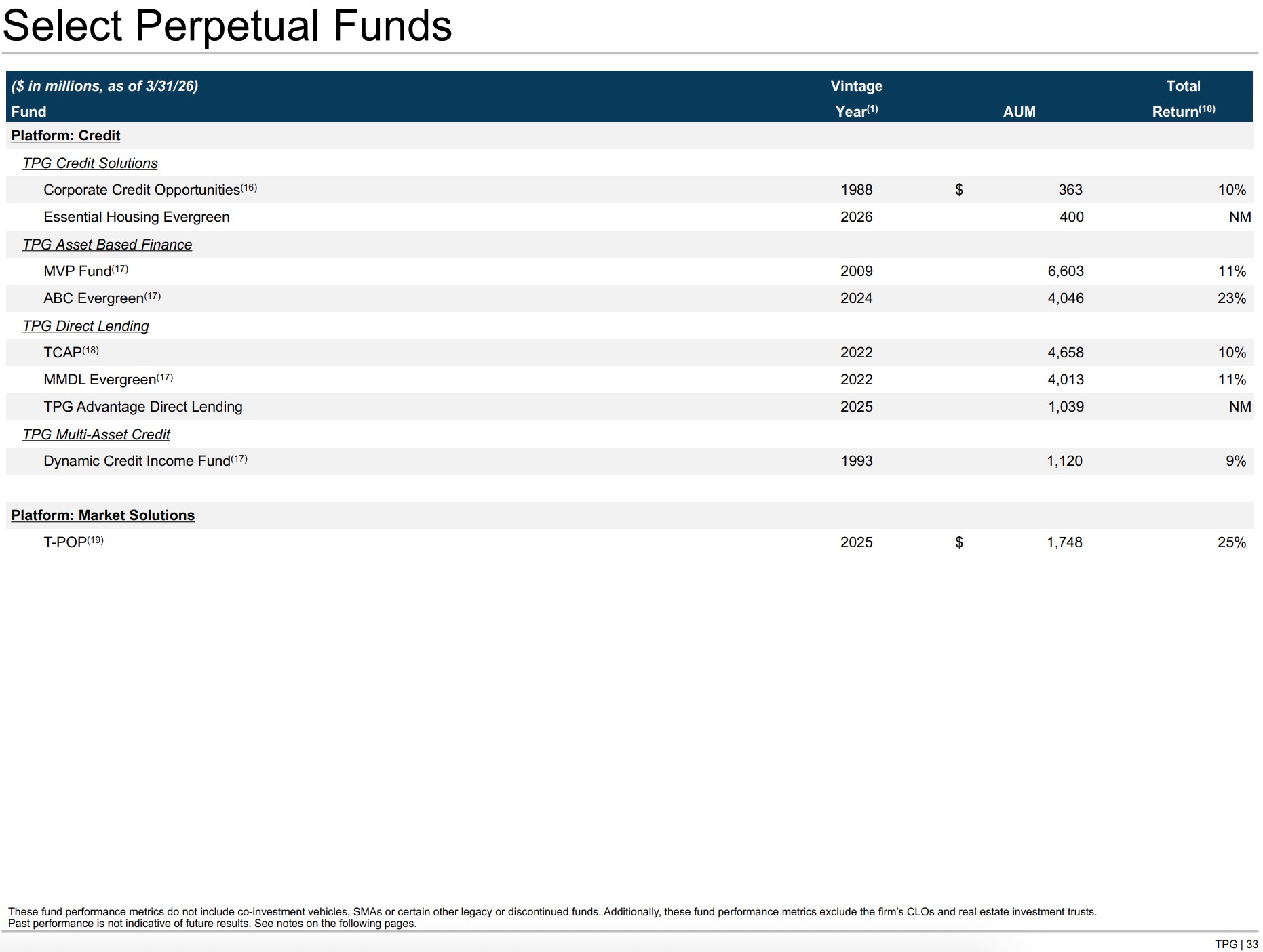

TPG

First Quarter 2026 Financial Results presentation here.

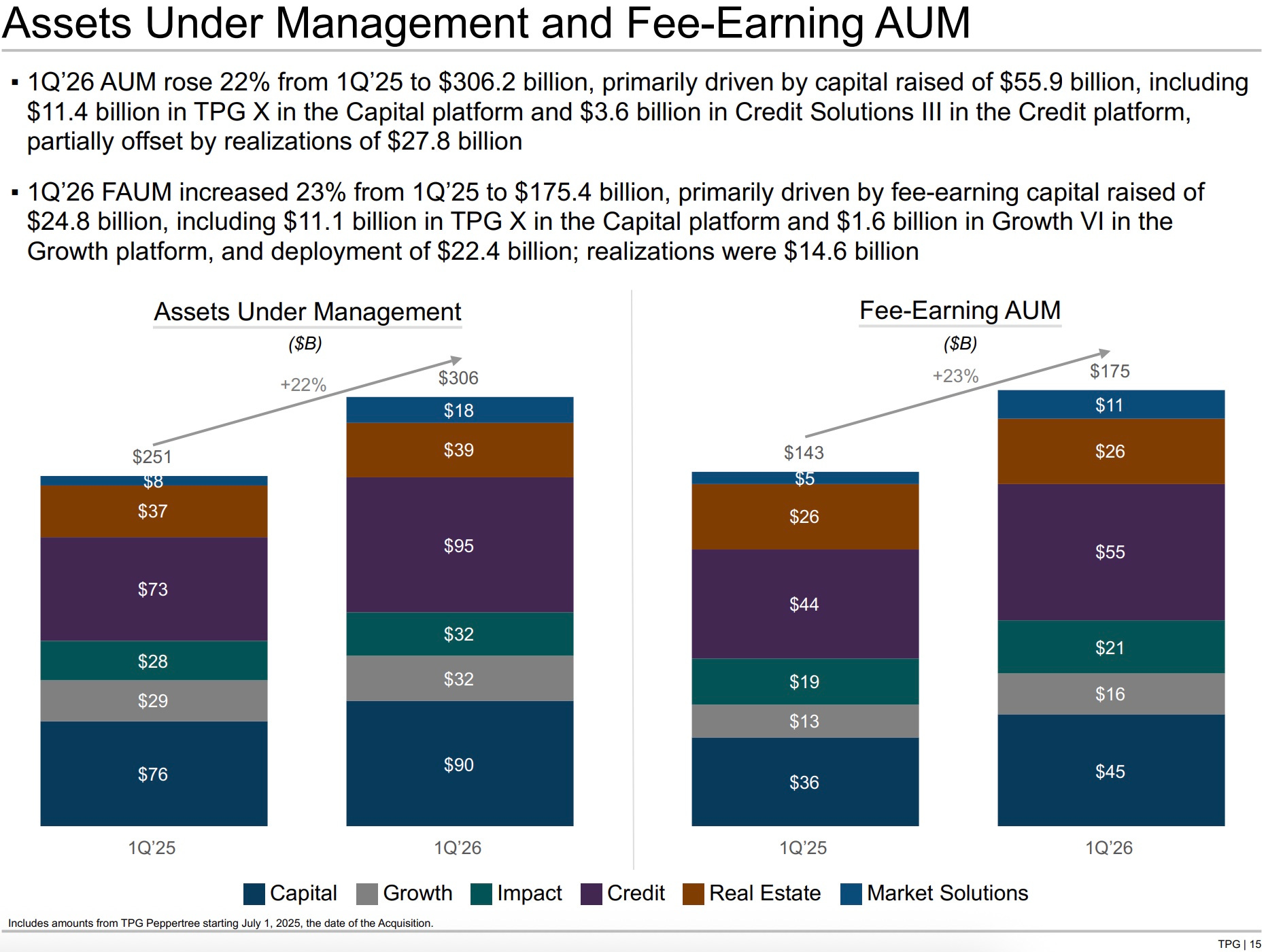

The chart: TPG’s AUM grew 22% in 1Q26 compared to 1Q25.

The takeaway: TPG’s flagship private equity buyout fund, TPG X, helped drive inflows for the firm, with $11.4B coming from the fundraise.

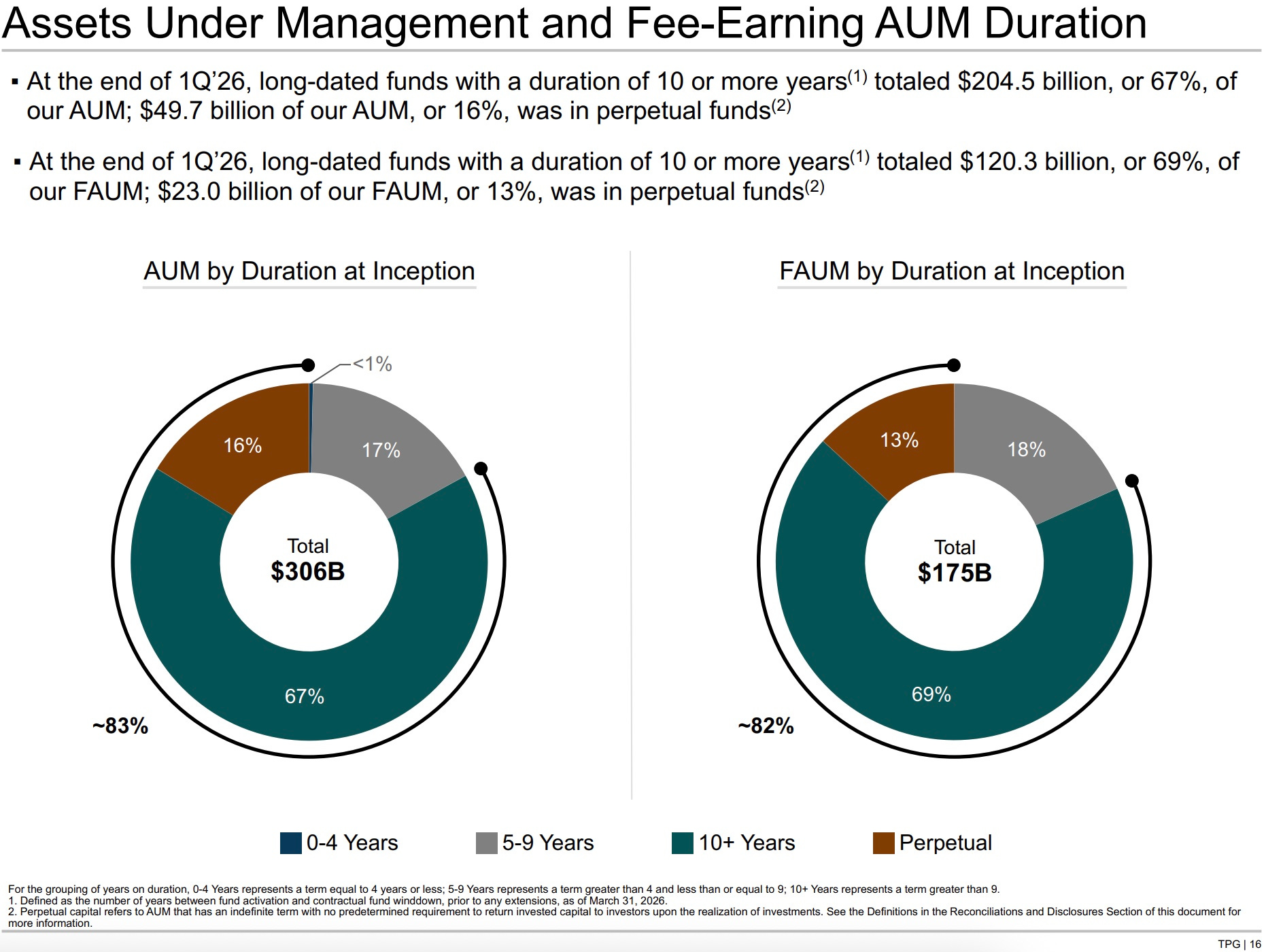

The chart: ~83% of TPG’s $306B AUM resides in long-dated funds with duration of ten or more years.

The takeaway: The overwhelming majority of TPG’s capital is in long-date and perpetual funds.

The chart: T-POP, TPG’s evergreen private equity solution, is over $1.74B AUM after a year in market.

The takeaway: I included this slide from TPG’s presentation to highlight the rapid growth of TPG’s evergreen private equity evergreen fund, T-POP. The fund, which invests 80% of its NAV into equity investments, has grown to over $1.74B AUM driven by both fundraising and a 25% return.

Carlyle

Shareholder Update (February 26, 2026) presentation here (note: Carlyle’s Q1 earnings presentation is on May 7, 2026, so this newsletter will include the latest Shareholder Update from February 2026 instead).

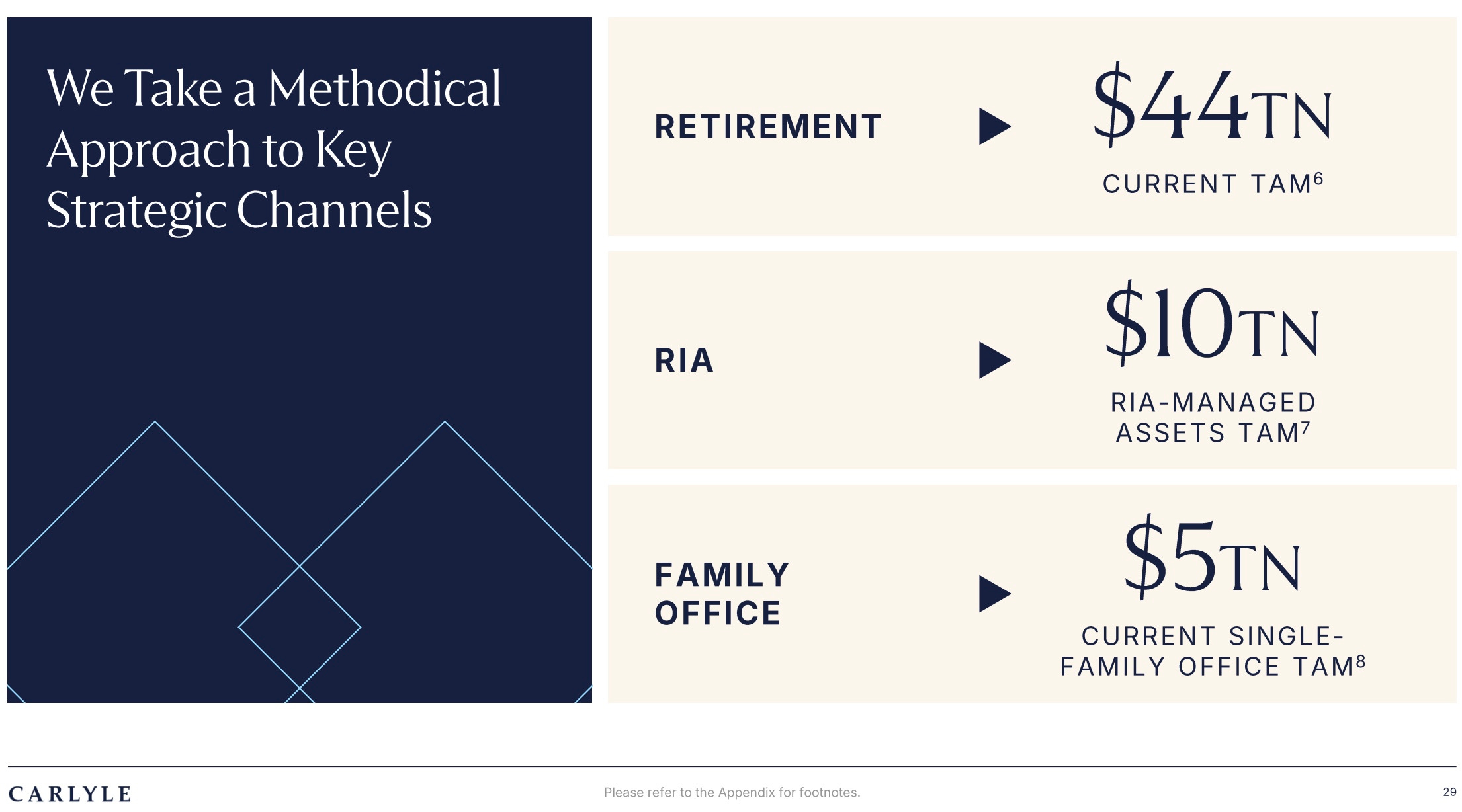

The chart: Carlyle is focused on tapping into key growth markets to drive AUM.

The takeaway: It’s notable that Carlyle highlighted both the RIA market (interestingly, the firm recently took a majority stake in MAI Capital) and Single-Family Office space as specific areas of customer channel focus. In addition to Retirement, which represents a massive TAM expansion opportunity for Carlyle and its peers, the RIA and SFO spaces are ripe for opportunity. Carlyle’s platform across private equity and secondaries in particular should appeal to these channels (more on the secondary market below).

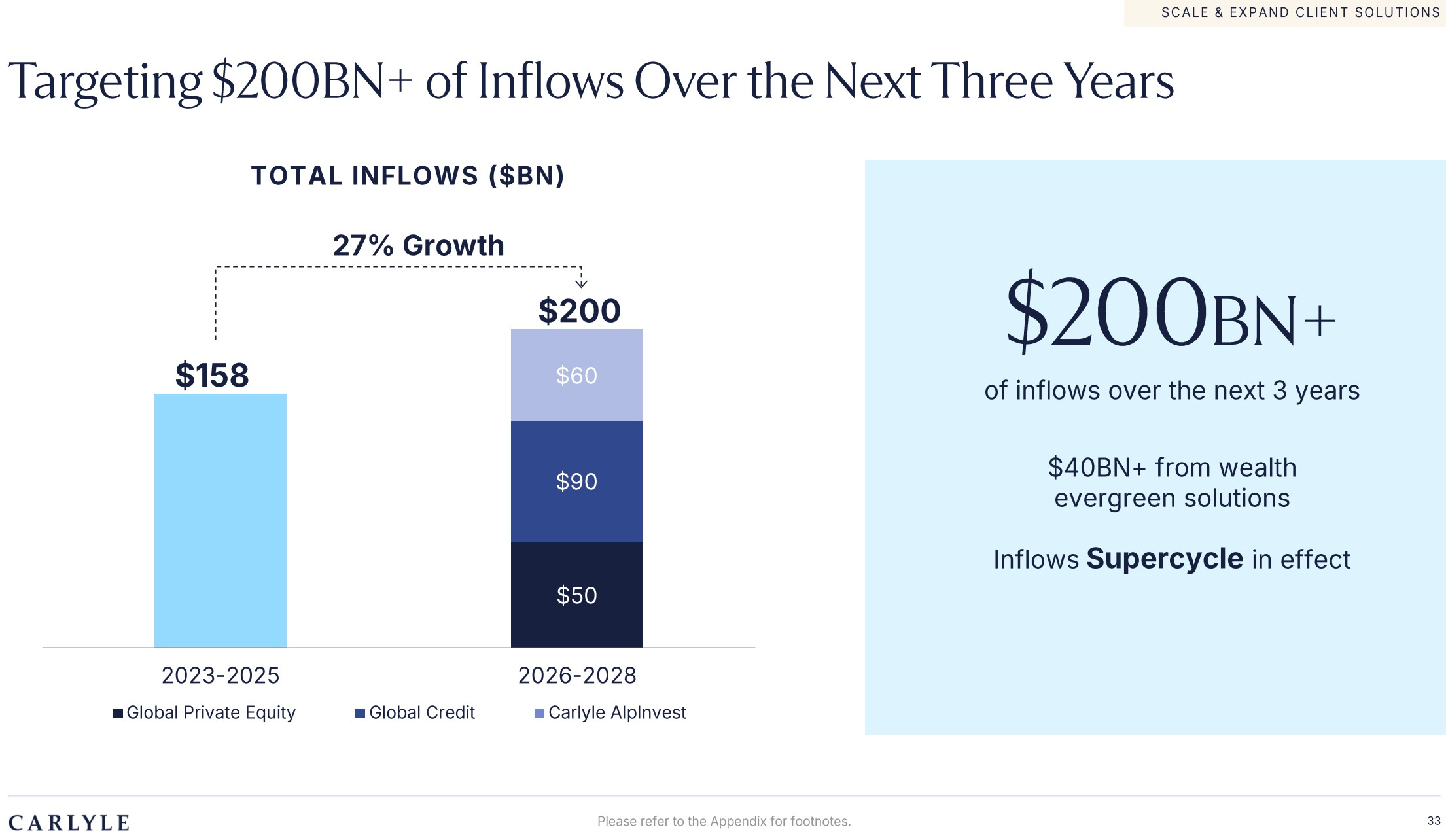

The chart: Carlyle is targeting $200B of inflows over the next three years, which would represent 27% growth.

The takeaway: Carlyle is projecting $40B of inflows from its wealth evergreen solutions, which would be almost 7x the firm’s evergreen AUM in 2023 ($6B). The firm is expecting Global Credit (of which Direct Lending is only one strategy amongst its diversified credit platform) to drive much of the inflows. Secondaries (via AlpInvest) should also drive meaningful inflows given the market opportunity in secondaries.

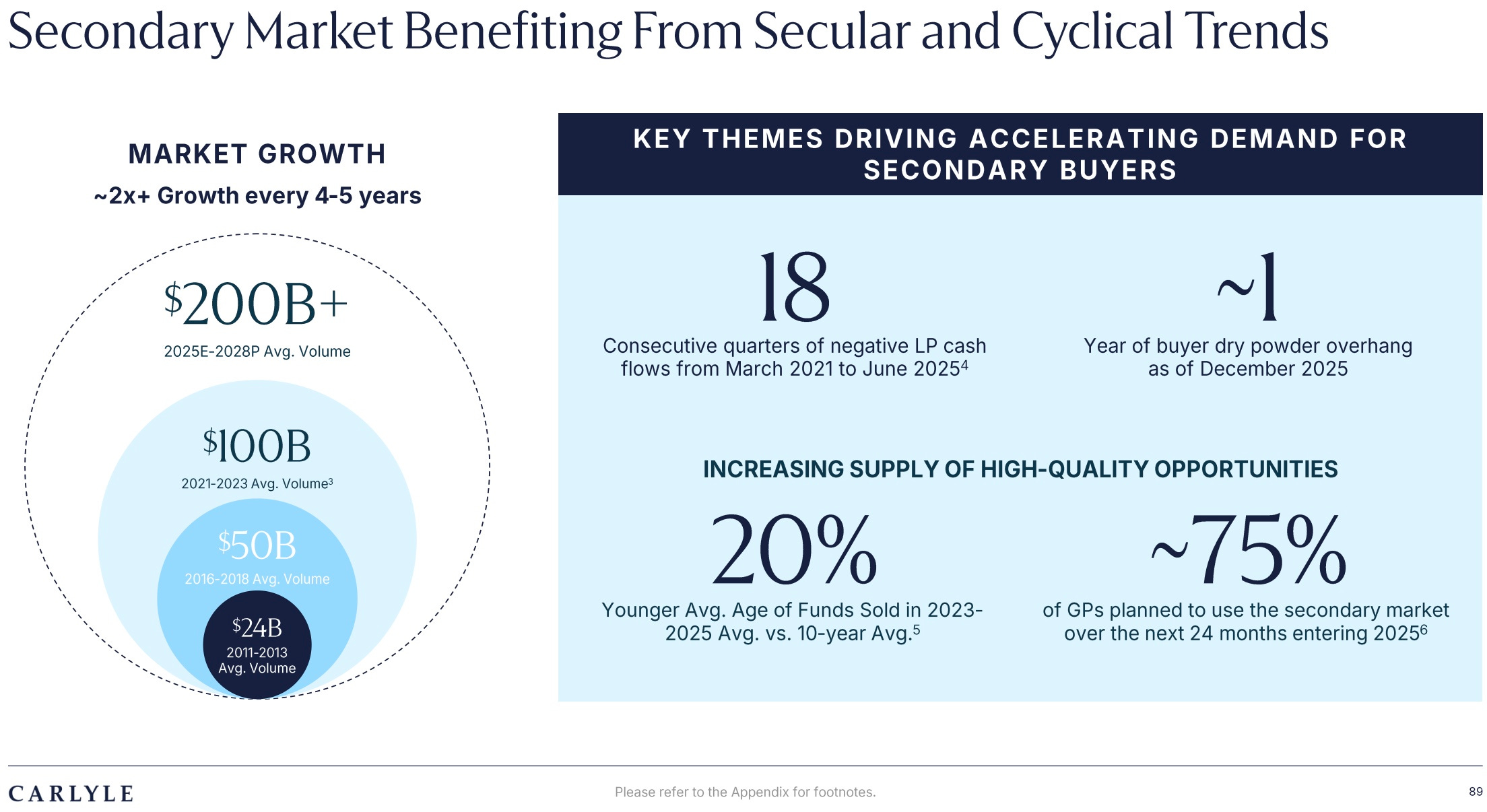

The chart: Secondaries is a growing market, with significantly more expansion to come. 75% of GPs plan to use the secondary market over the next 24 months entering 2025.

The takeaway: The secondaries market has experienced 2x growth every 4-5 years and shows no signs of abating. Firms like Carlyle, which have scaled secondaries solutions on platform, should benefit from both the growth in the secondaries market and the appeal of this strategy to the wealth channel. Statistics like those below should render it no surprise why Carlyle’s peers, KKR and EQT, have both recently acquired secondaries capabilities.

CVC

Q1 2026 Activity Update (April 30, 2026) presentation here.

The chart: Non-PE strategies now represent 52% of CVC’s total FPAUM.

The takeaway: CVC continues to diversify its AUM beyond Private Equity strategies. This continued expansion of its platform was punctuated by the firm’s acquisition of Marathon Asset Management, a credit manager. The firm also saw 40% quarterly growth in Private Wealth, with AUM in Private Wealth now at €5.2B. CVC also noted that CVC-CRED and CVC-PE have experienced minimal redemptions from evergreen vehicles thus far.

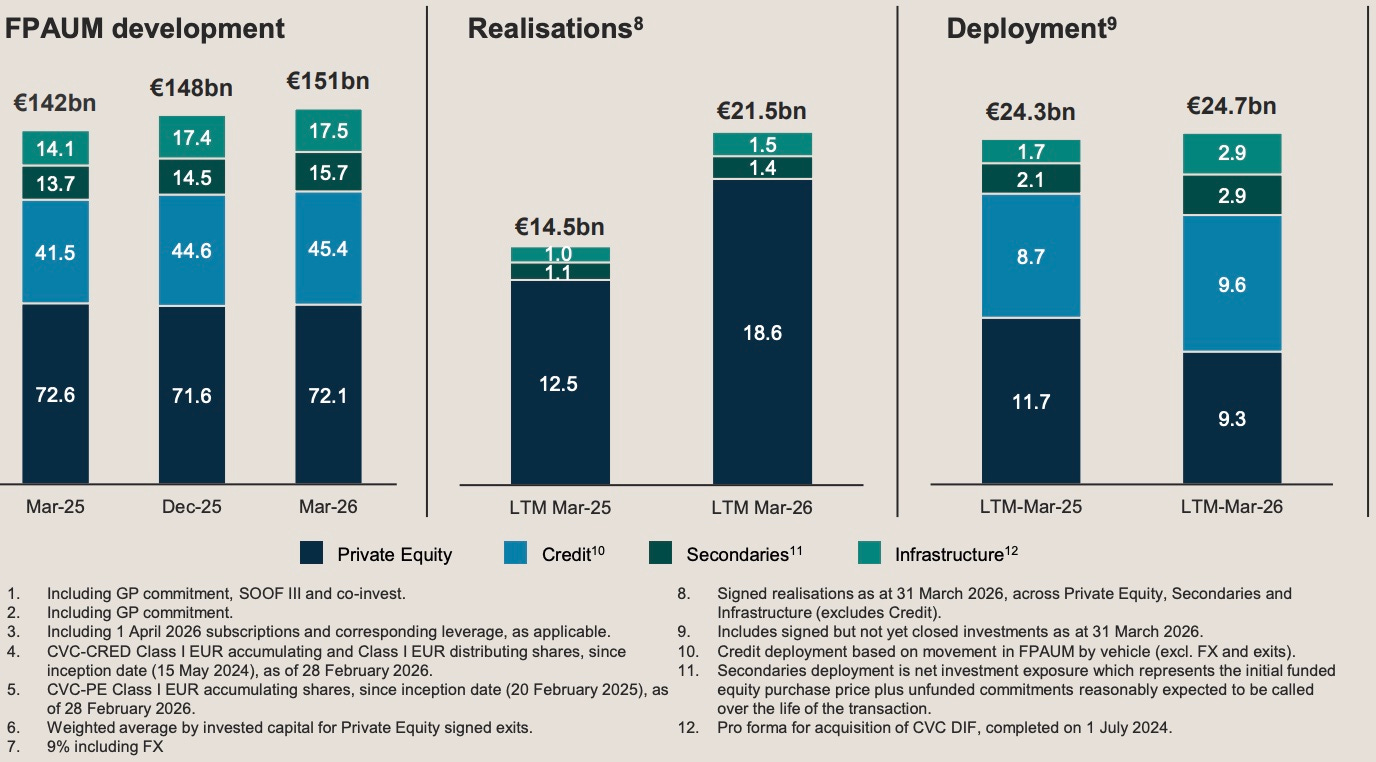

The chart: CVC’s LTM to March 2026 realizations in private equity have been meaningful, with €18.6B of realizations coming in the past year. This figure was a marked increase over the €12.5B in LTM PE realizations to March 2025.

The takeaway: The firm’s realization activity over the past twelve months was juxtaposed by a material decrease in deployment in Private Equity over LTM to March 2026, with CVC only deploying €9.3B LTM March 2026. CVC’s exit activity is a notable clue about how some of the industry’s largest private equity firms are approaching the current environment, looking to exit on high-quality assets where they believe they can achieve palatable exit prices. CVC and its peer EQT have both had meaningful exit activity in recent months.

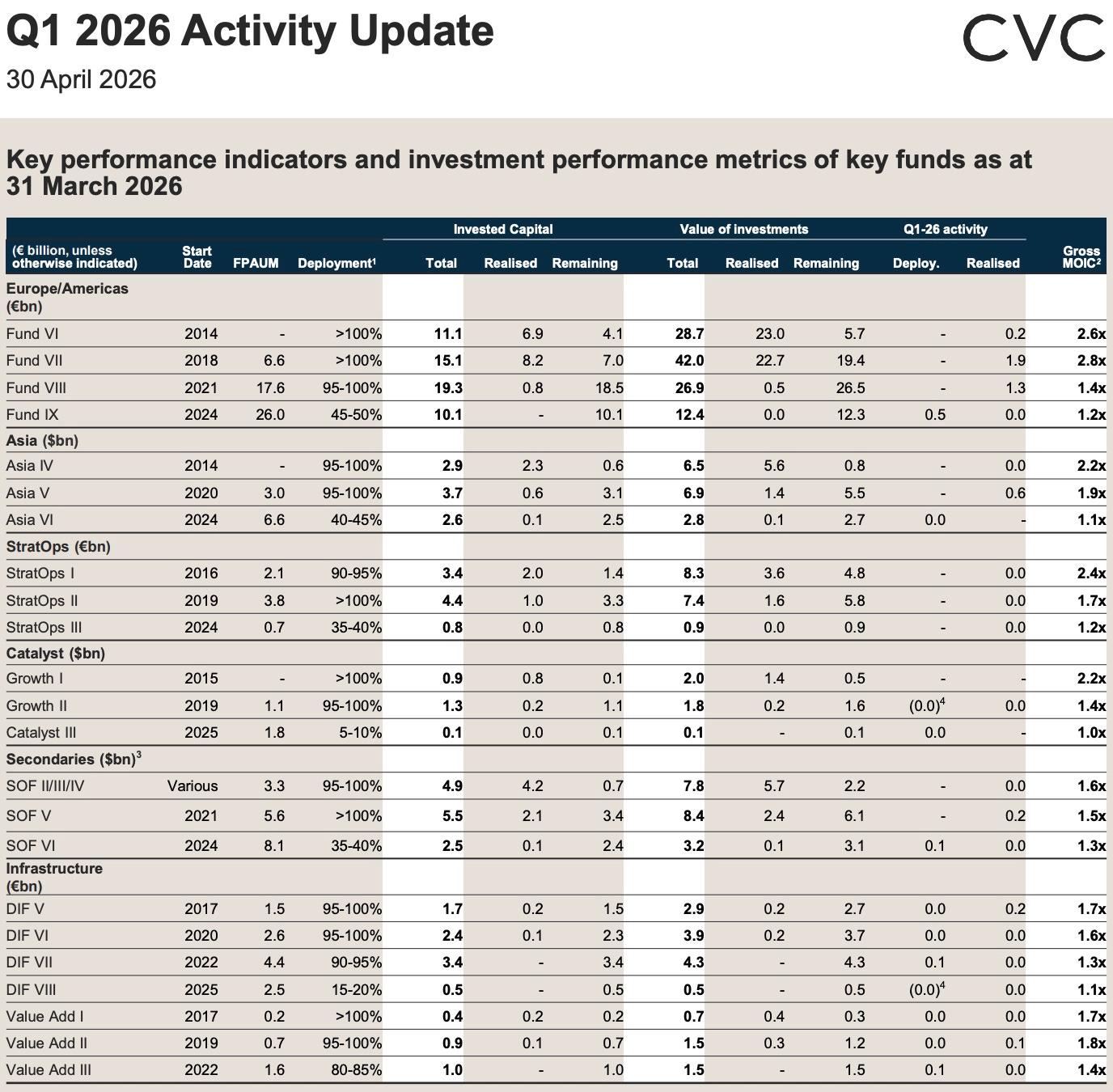

The chart: There are some notable datapoints from CVC’s flagship private equity buyout business. The firm’s 2018 vintage (VII) only had €6.6B of FPAUM (and €15.1B total invested capital). That fund has achieved a 2.8x gross MOIC.

The takeaway: It’s likely that VII fund’s performance played a contributing factor in the firm’s successor funds, VIII and XI (to date, the world’s largest buyout fund raised), raising a significantly higher % of FPAUM relative to total invested capital. VIII had €17.6B of FPAUM (on €19.3B) and XI has raised €26B in FPAUM.

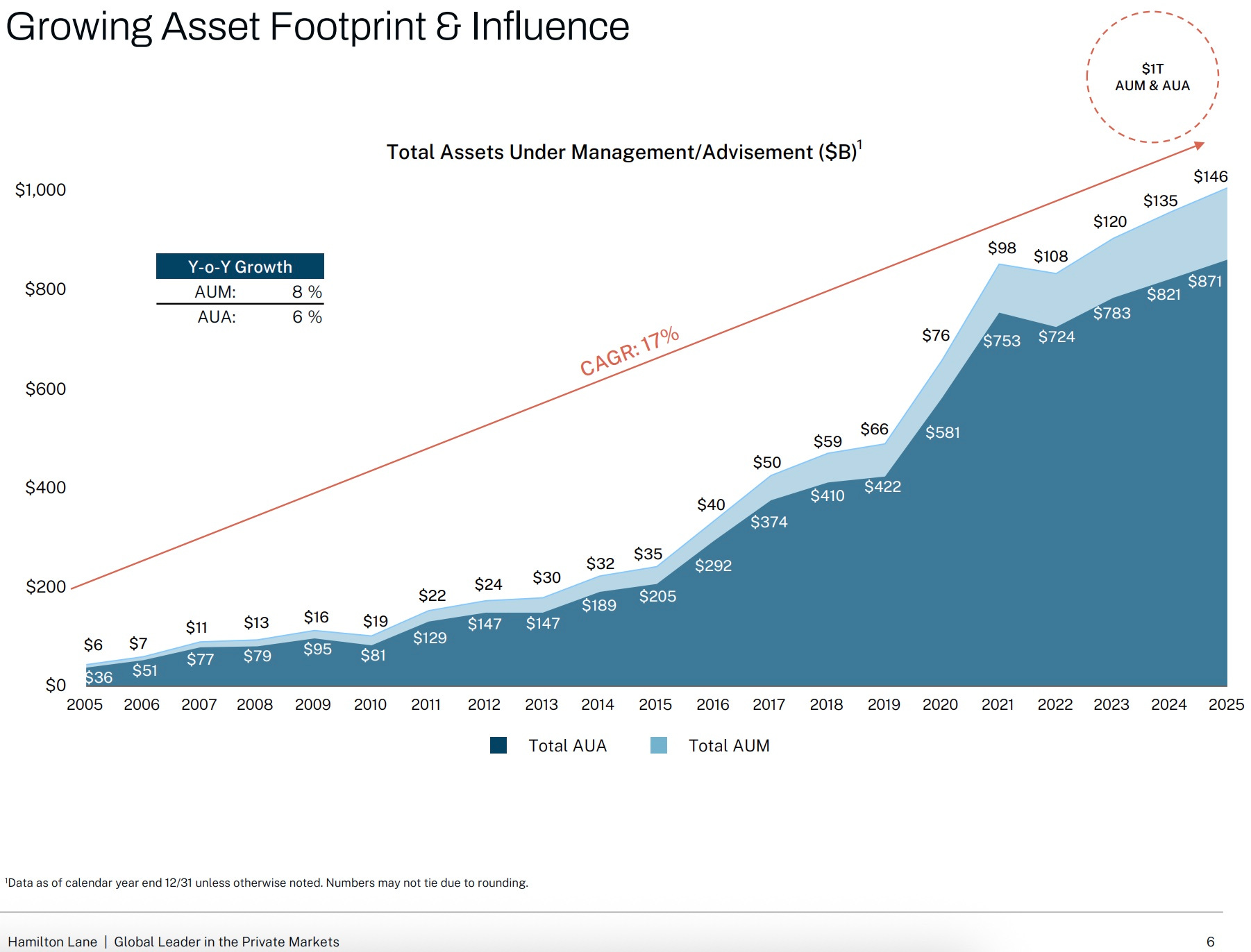

Hamilton Lane

Fiscal Year 2026 Third Quarter Results (February 3, 2026) presentation here (note: Hamilton Lane reports on a different schedule, so the presentation shared here is the firm’s Q3 results for 2026 reported in February 2026).

The chart: Hamilton Lane’s AUM/A continues to grow at a 17% CAGR. The firm’s AUM growth outpaces its AUA growth Y-o-Y.

The takeaway: Hamilton Lane has now reached $146B AUM. AUA still represents the lion’s share of the firm’s AUA, but the firm continues to transform into an AUM business.

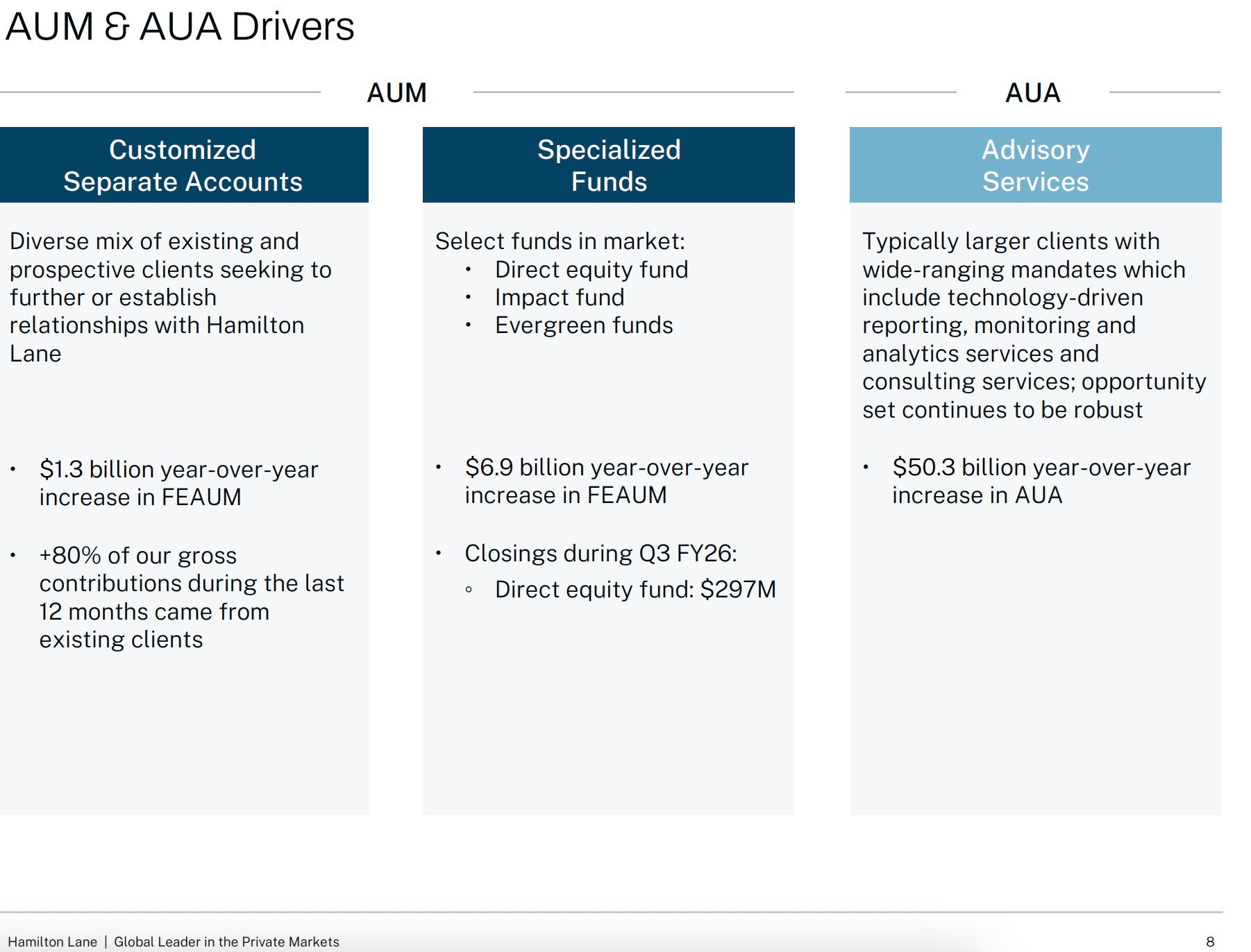

The chart: Customized Separate Accounts continue to drive a portion of the firm’s AUM (and associated revenue). Notably, 80% of their gross contributions over the past twelve months came from existing clients.

The takeaway: The above datapoint highlights that many LP clients in private markets are still looking for investment solutions and customized, bespoke exposure to private markets access. It will be interesting to see if this becomes a trend in the wealth channel as well, particularly after a number of OCIO and wealth management firm combinations.

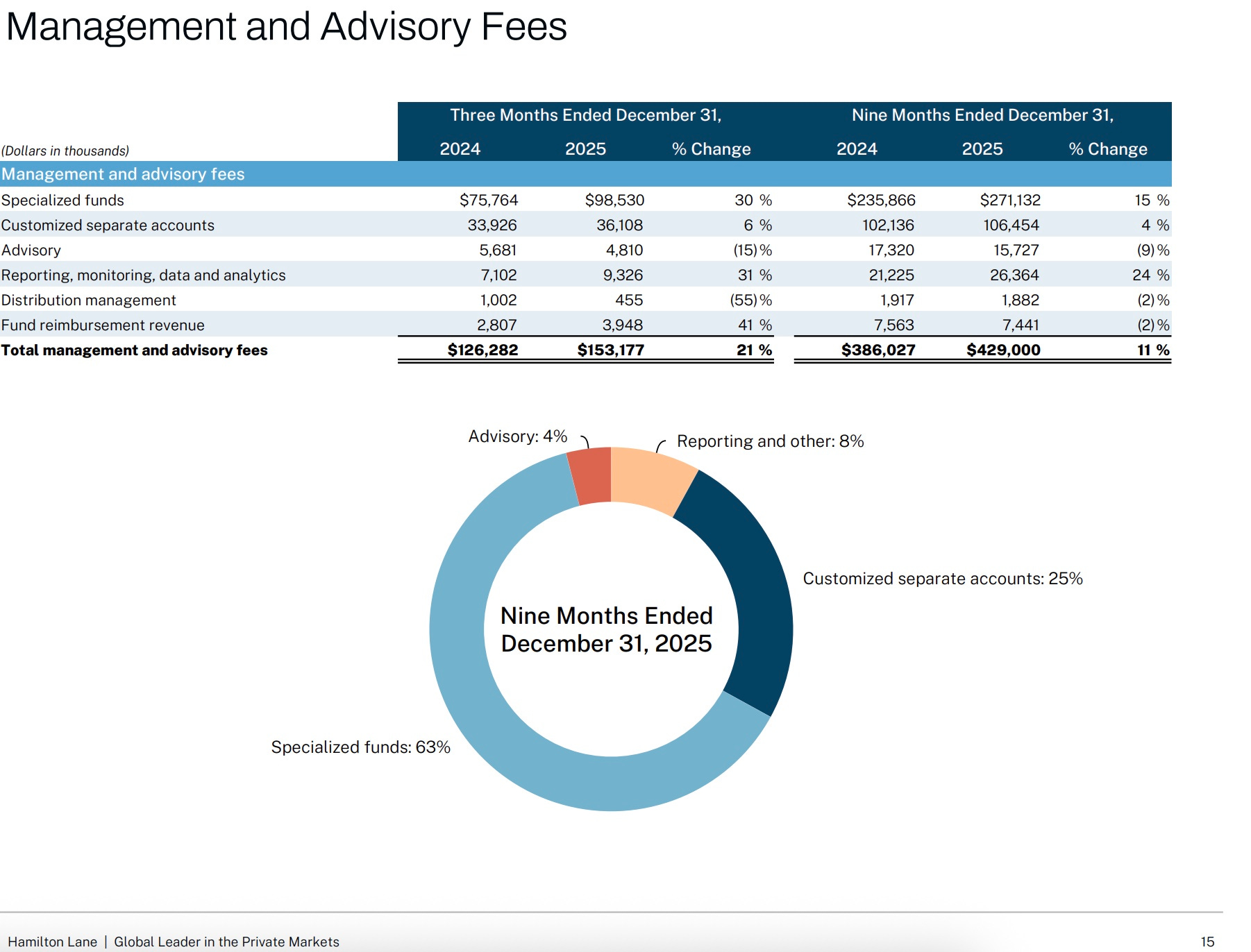

The chart: Fees for specialized funds (largely evergreens) grew meaningfully over the past three months and nine months. These growth largely drove the firm’s fee revenues.

The takeaway: Hamilton Lane is making a big push into the wealth channel with its evergreen solutions. The firm’s management fee performance reflects this feature. Notably, the firm experienced meaningful growth in its reporting, monitoring, and data / analytics fee stream.

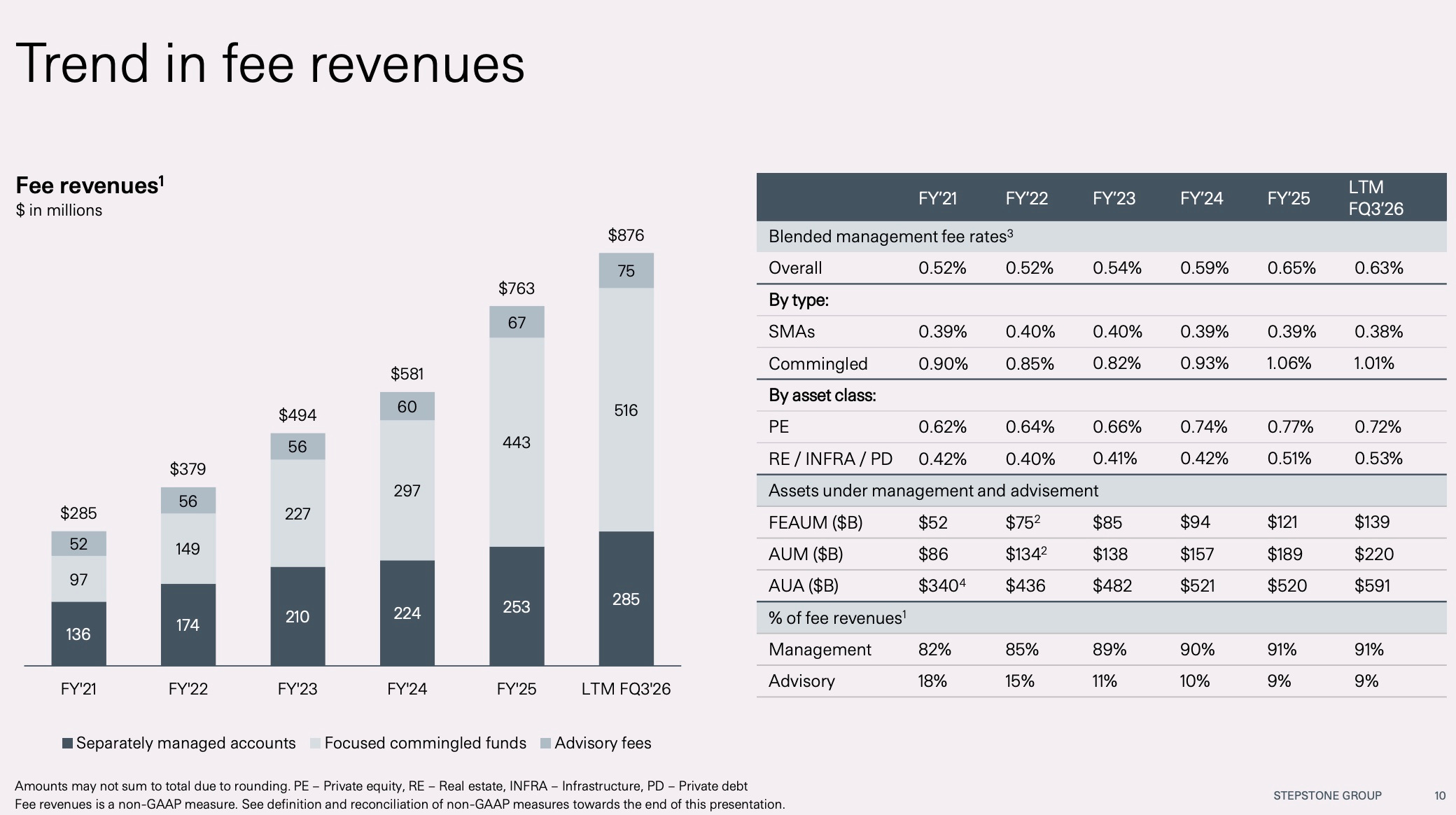

StepStone Group

Earnings Presentation Third Quarter Fiscal Year 2026 (February 5, 2026) presentation here (note: StepStone reports on a different schedule, so the presentation shared here is the firm’s Q3 results for 2026 reported in February 2026).

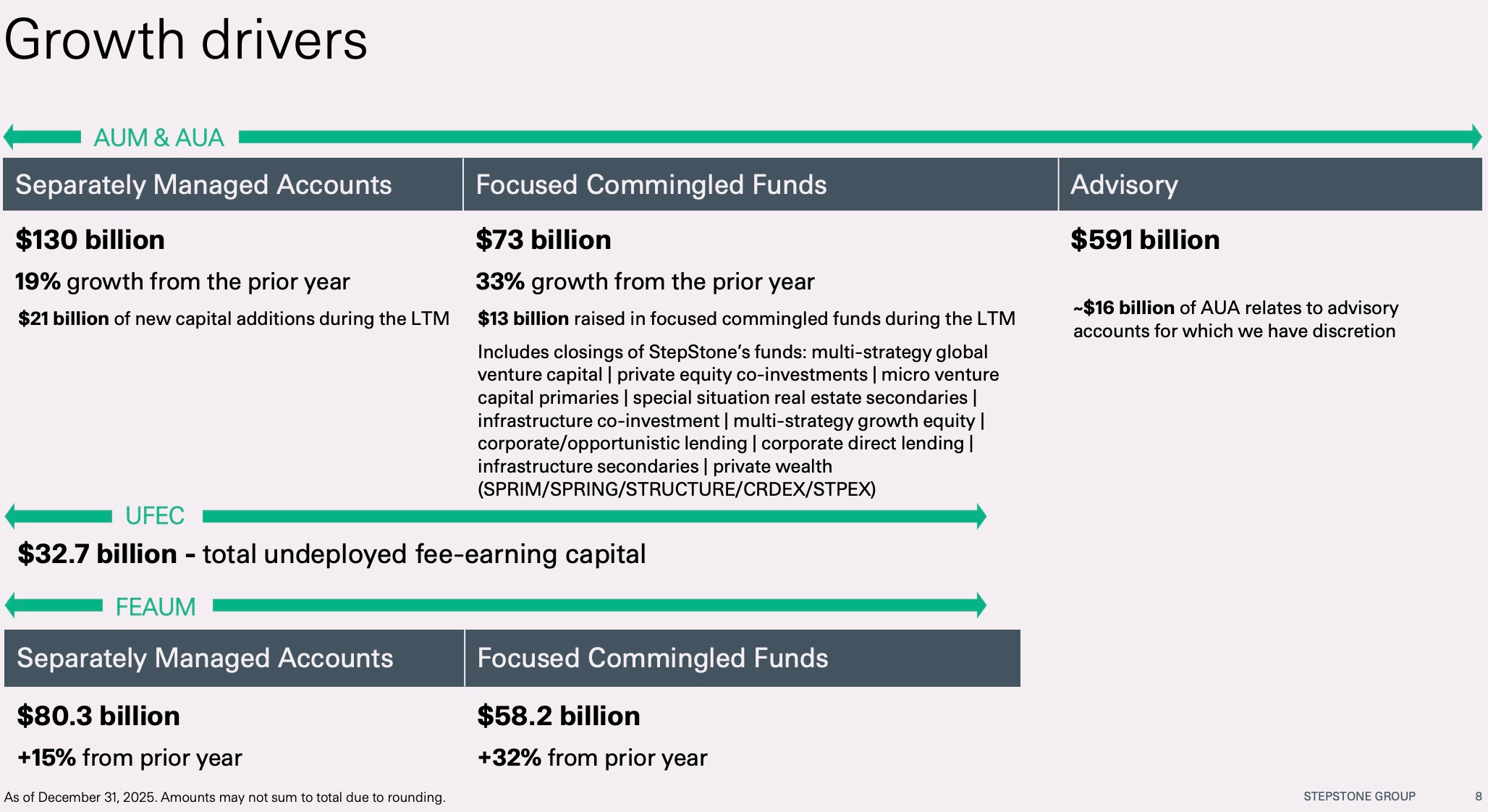

The chart: AUM of commingled funds for StepStone grew 33% over the prior year.

The takeaway: StepStone has made a concerted effort to build out its presence in the wealth channel and it’s paying off.

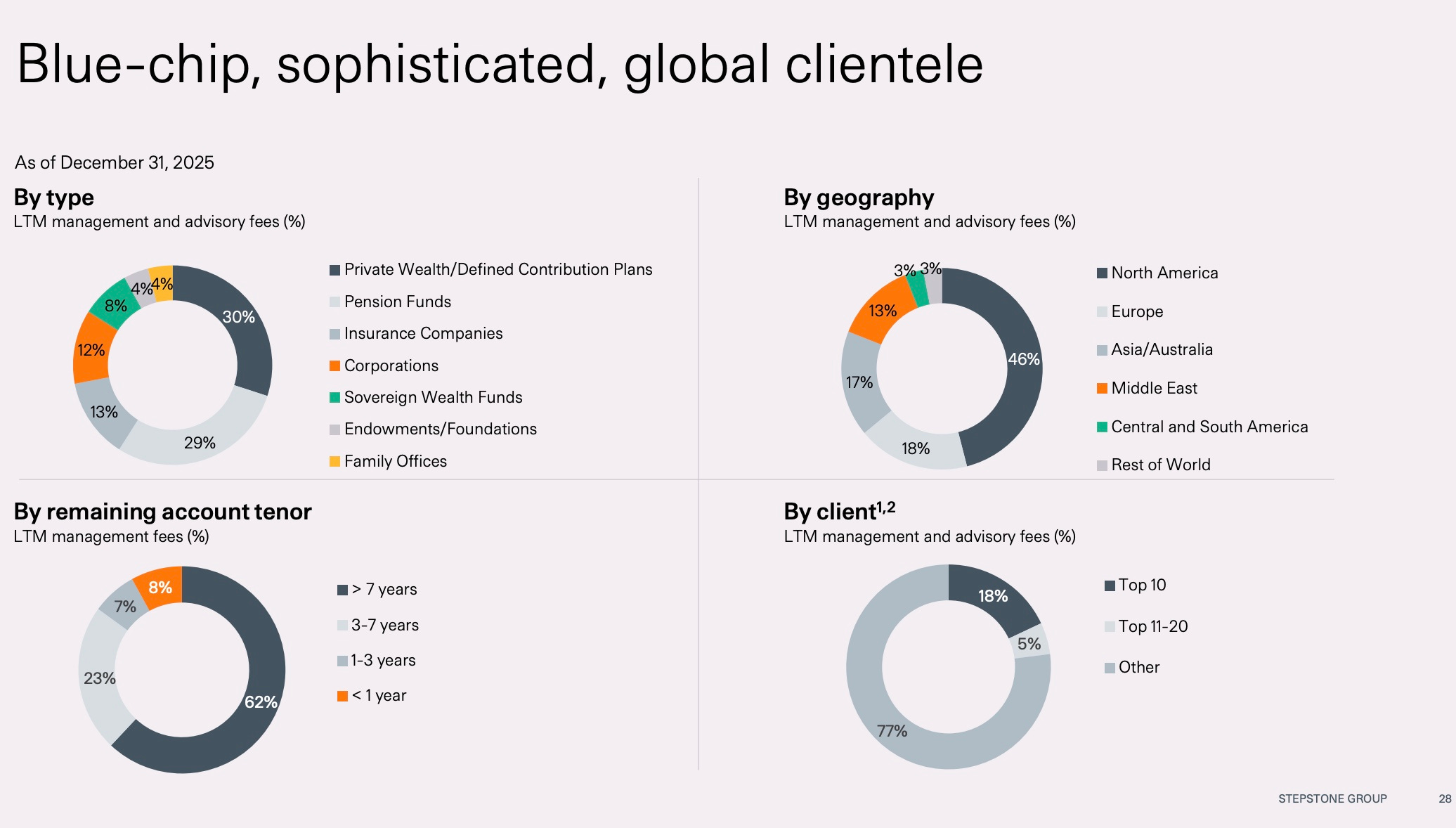

The chart: Private wealth and defined contribution plans account for 30% of the firm’s management and advisory fees.

The takeaway: Private wealth is StepStone’s largest client segment. Pensions and insurance companies also represent meaningful portions of StepStone’s fee revenue, but it will be interesting to see how the firm’s fee revenue continues to evolve given the focus on the wealth channel.

The chart: Commingled fund blended management fee rates are meaningfully higher than SMA fees.

The takeaway: Fee revenue from commingled funds is almost 2x that of separately managed accounts, which was not the case in FY21, when SMAs accounted for $136M in revenue and commingled funds accounted for $97M in revenue.

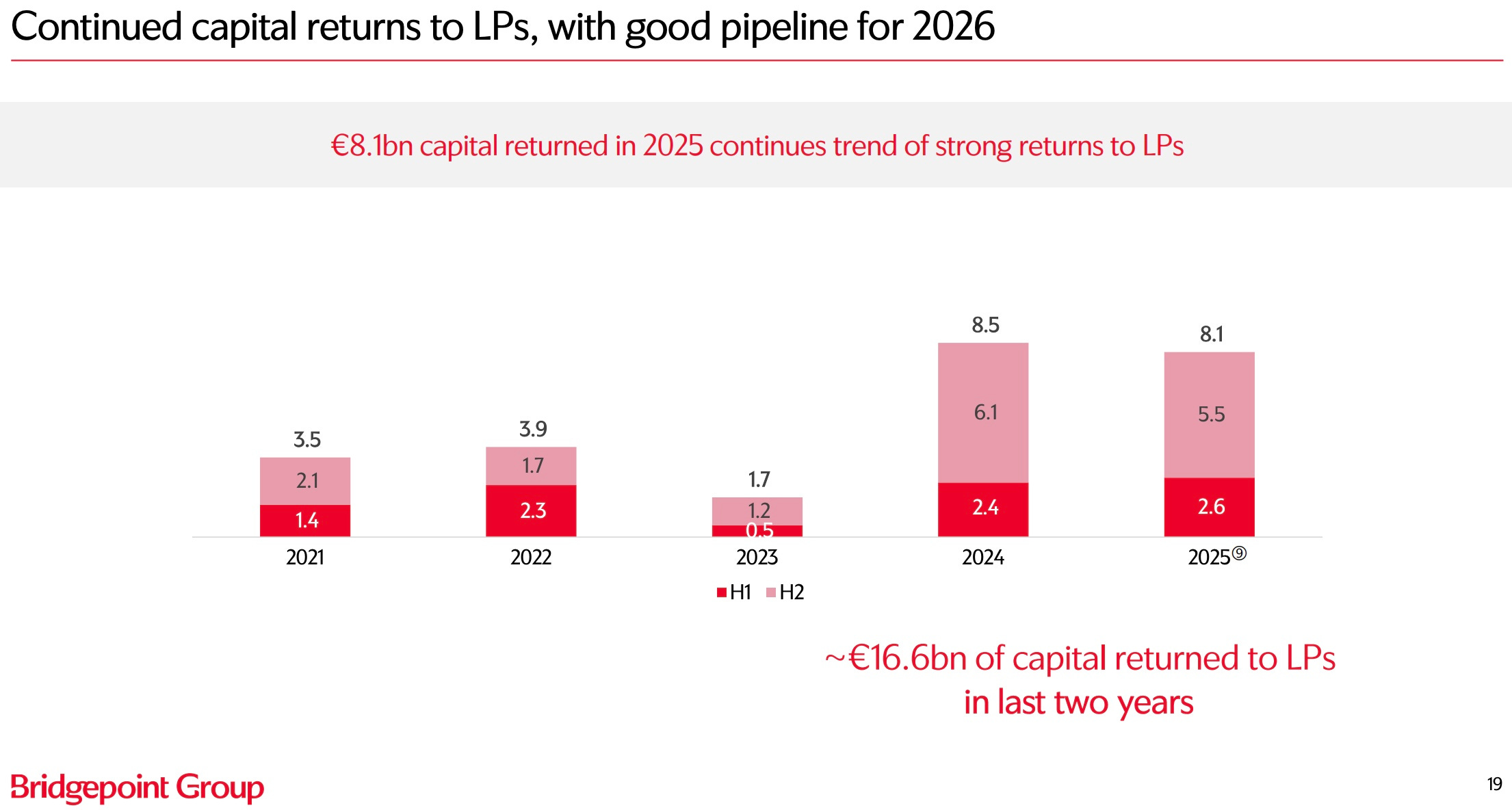

Bridgepoint

Full Year Results 2025 presentation here (note: Bridgepoint published its 2025 full year results on 12th March 2026).

The chart: Bridgepoint has returned €16.6B to LPs in the past two years, including €8.1B returned in 2025.

The takeaway: Bridgepoint’s exit activity over the past few years continues the trend from European PE firms (EQT and CVC above) that have delivered meaningful DPI back to investors over the past few years. While both EQT and CVC are global, EQT’s biggest exit, Galderma, was a Switzerland headquartered company. Bridgepoint’s focus on the European middle market has enabled the firm to achieve a number of exits due to its market leadership and expansive regional footprint.

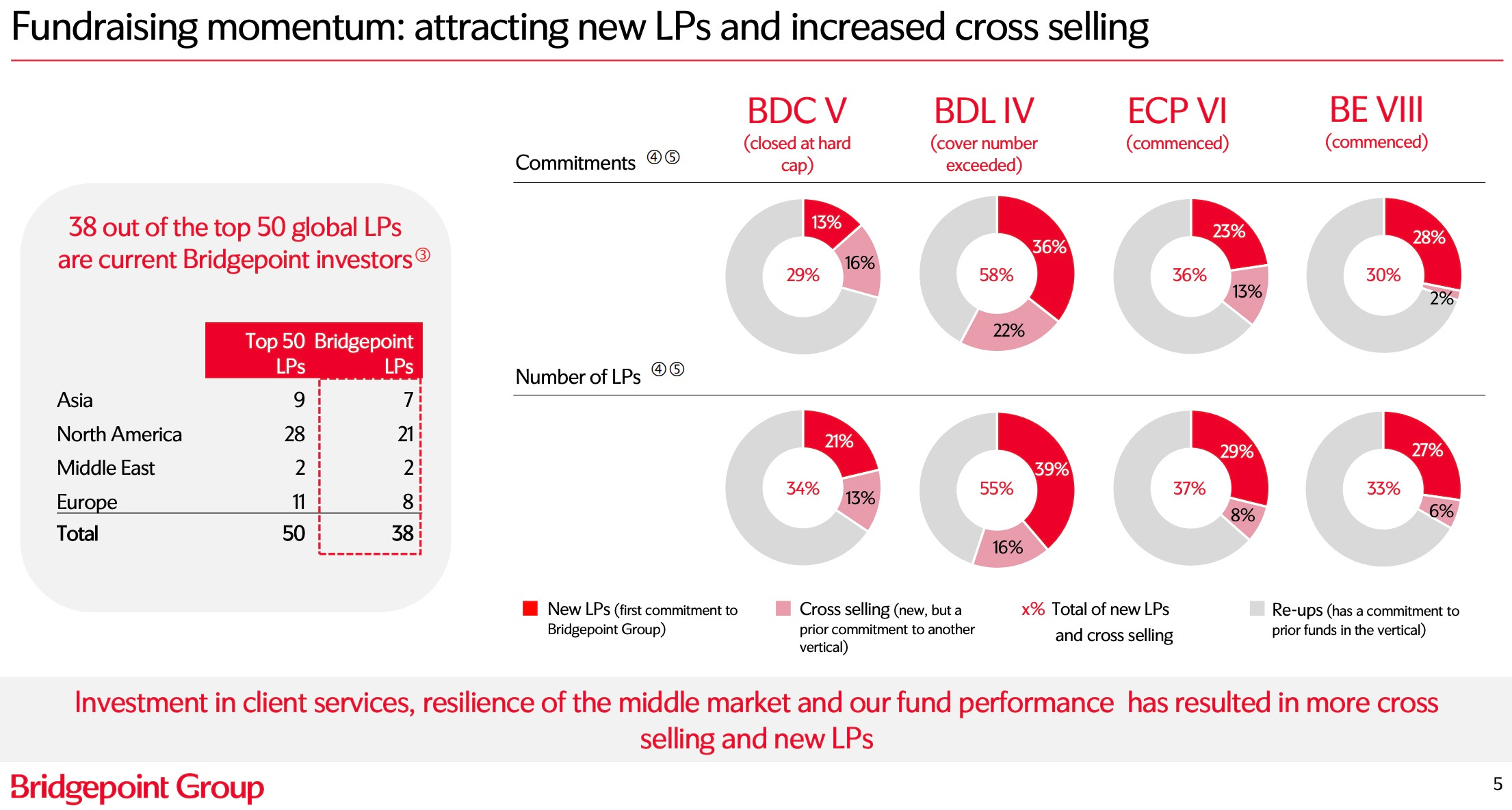

The chart: Bridgepoint has managed to successfully increase cross-selling amongst funds.

The takeaway: Bridgepoint’s ability to cross-sell across funds and strategies is highlighted below, with the fruits of the firm’s labor of acquiring a credit business (from EQT) and an energy / infrastructure business (ECP) beginning to show. Now that the firm has recently acquired Newbury Partners to add a secondaries capability, it will be interesting to see how much the firm is able to cross-sell LPs into secondaries.

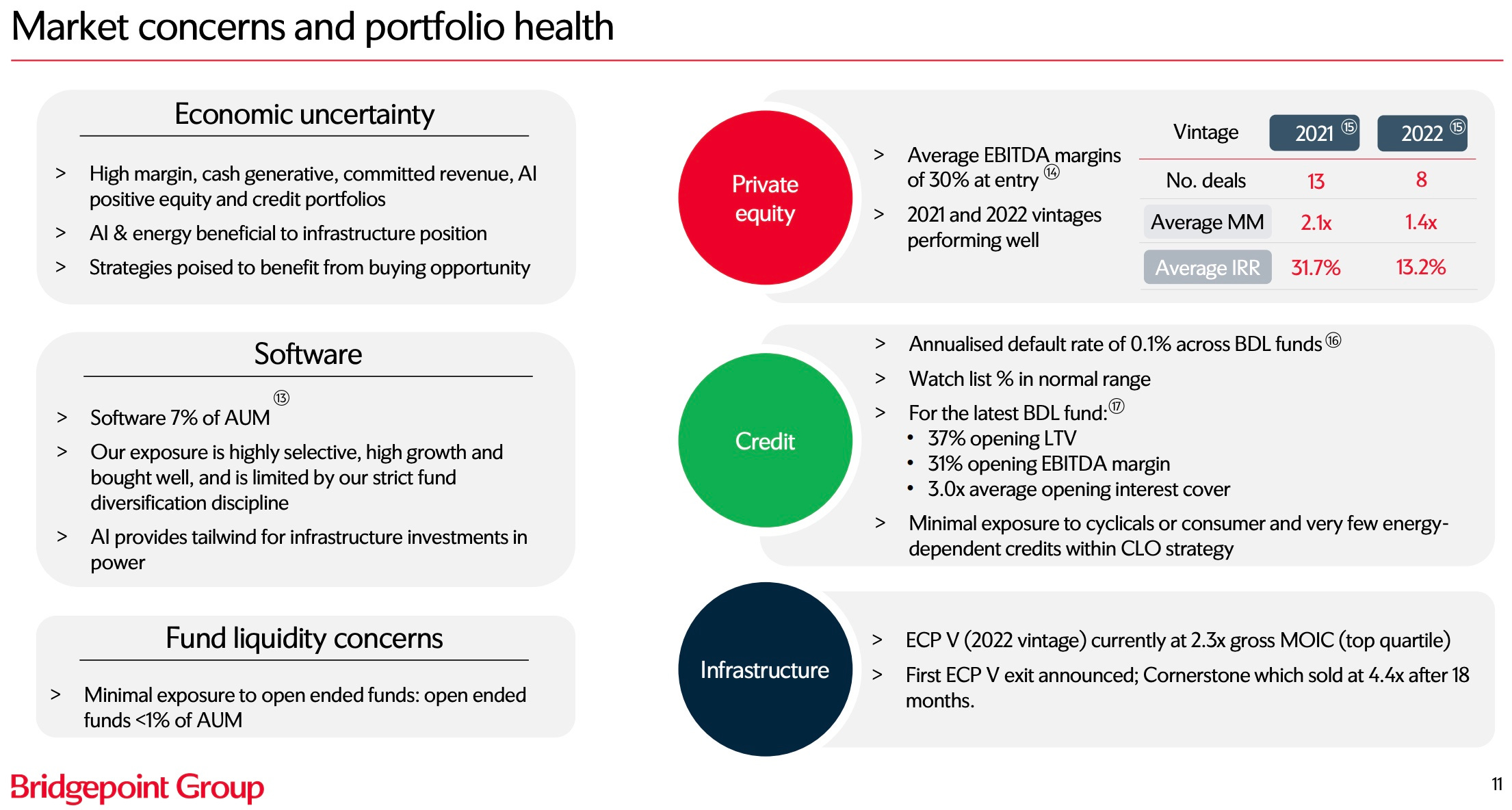

The chart: Bridgepoint has relatively low levels of exposure to software, with software at 7% of AUM, and to evergreen funds, with evergreen fund AUM representing sub 1% of total AUM.

The takeaway: Bridgepoint appears to be relatively insulated from both software and evergreen exposure to date.

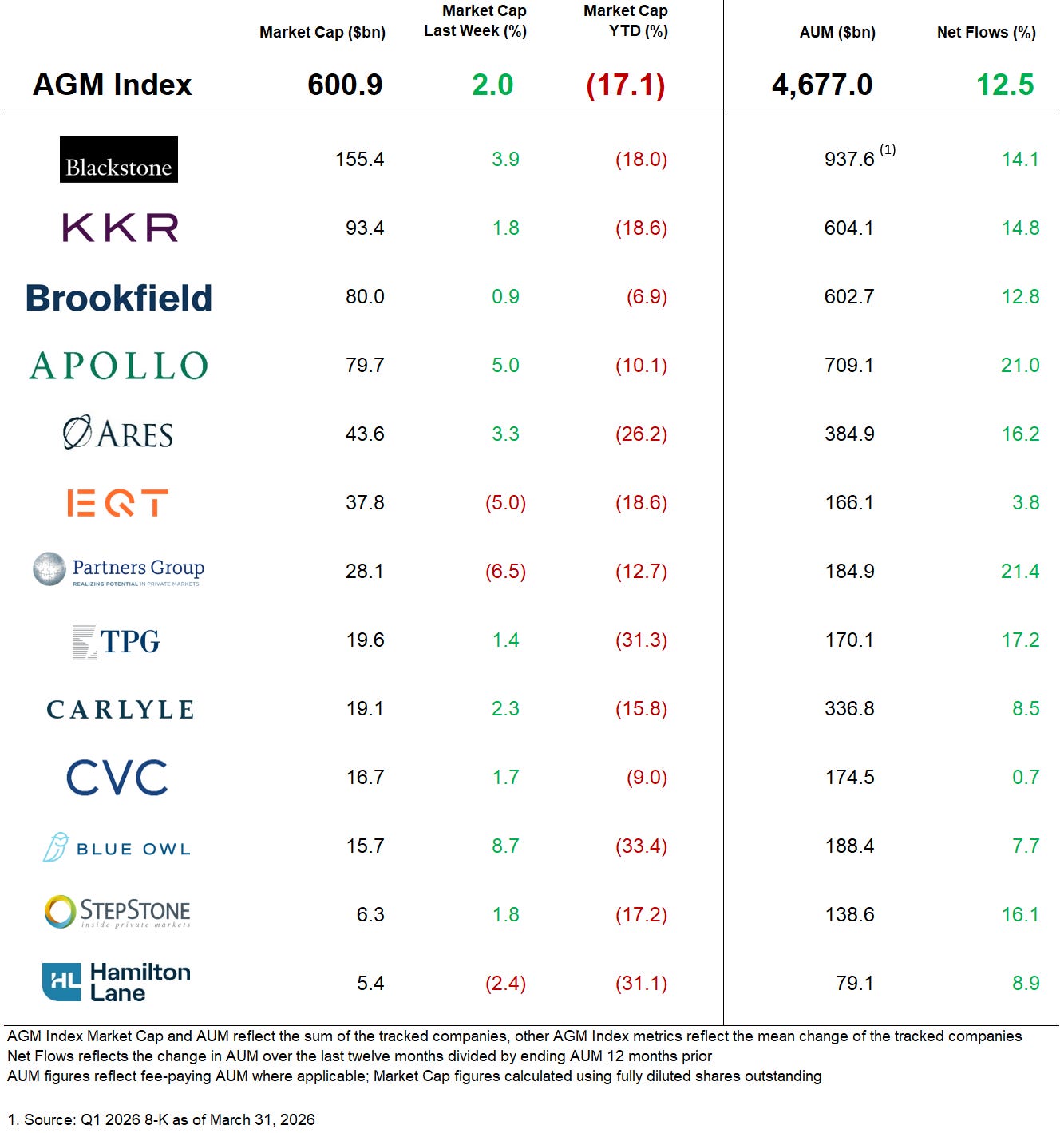

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know, and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Blackstone (Alternative asset manager) - Blackstone Private Wealth - Product Specialist, Vice President (Real Assets). Click here to learn more.

🔍 KKR (Alternative asset manager) - VP - Social Media Strategist. Click here to learn more.

🔍 Apollo Global Management (Alternative asset manager) - Director, Transformation Management - Private Credit & Private Markets. Click here to learn more.

🔍 EQT Group (Alternative asset manager) - Private Equity Associate. Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Global Client Marketing, Product Marketing & Content Strategy – Senior Associate. Click here to learn more.

🔍 Franklin Templeton (Asset manager) - Portfolio Manager, Private Markets. Click here to learn more.

🔍 Goldman Sachs Alternatives (Alternative asset manager) - Asset & Wealth Management, Client Solutions Group, Wealth Alternatives Specialist, New York - Vice President. Click here to learn more.

🔍 HarbourVest (Alternative asset manager) - Senior Associate, Business Intelligence - Global Private Wealth. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - Chief Risk Officer, Managing Director. Click here to learn more.

🔍 Ultimus Fund Solutions (Fund administrator) - Managing Director, Fund Accounting. Click here to learn more.

🔍 Anthropic (AI foundational model company) - Head of Finance AI & Innovation. Click here to learn more.

🔍 Krilogy (Wealth manager) - Senior Wealth Advisor. Click here to learn more.

🔍 MSCI (Data services) - Sales Executive, VP - Private Capital Solutions. Click here to learn more.

🤝 Interested in learning more about AGM RIA Field Trips? 🤝

Read about the expansion of Alt Goes Mainstream, with the launch of the AGM Community and AGM Events.

We’ve also built out the AGM Community RIA Advisory Board, an experienced, thoughtful, and intellectually curious group of private wealth management and private markets executives and operators, to help shape the direction of AGM Community.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

🎥 Watch Lincoln International’s Managing Director and Global Head of the Portfolio Valuations practice Brian Garfield share perspectives on how AI is impacting private markets valuations. Watch here.

📝 Read The AGM Q&A with Davidson Kempner Managing Partner and Chief Investment Officer Tony Yoseloff and Partner and Head of Research Suzanne Gibbons for opportunities in credit amidst a capital structure reset. Read here.

🎥 Watch Bridgepoint’s Partner and Chief Investment Officer Xavier Robert provide a masterclass on the European middle market investing landscape. Watch here.

🎥 Watch AlphaCore’s CEO & Founder Dick Pfister share his perspective on building a wealth management firm with “alpha at its core” in a podcast recorded live at the iCapital Connect conference. Watch here.

🎥 Watch HarbourVest’s CEO John Toomey discuss how private markets have changed and how HarbourVest has been “earning investors’ trust” for over 40 years. Watch here.

🎥 Watch Stonepeak’s Partner and Senior Managing Director, Stonepeak Credit Ryan Roberge on the evolution of infrastructure credit. Watch here.

🎥 Watch Bloomberg’s Head of Fixed Income & Private Markets Brad Foster on the convergence between public and private markets and how the market structure evolution in private markets might unfold. Watch here.

📝 Read The AGM Q&A with MSCI Head of Private Assets Luke Flemmer for perspectives on how market structure is evolving to build increased transparency in private markets. Read here.

🎥 Watch Brookfield Asset Management’s President, Private Equity Group David Nowak discuss what “earn your seat” private equity means and how Brookfield’s owner-operator and industrial heritage have shaped the firm’s private equity investment business. Watch here.

🎥 Listen and watch EQT’s Deputy Managing Partner and Chairperson of EQT Real Assets Lennart Blecher share the history, background, and evolution of the firm’s infrastructure investment business and how EQT takes an active ownership approach to real assets. Listen here and Watch here.

🎥 Watch Stable Asset Management’s Founder & CEO Erik Serrano Berntsen discuss the evolution of the GP seeding market and what it takes to build a great alternative asset management firm. Watch here.

🎥 Watch MSCI’s Head of Private Assets Luke Flemmer discuss the evolution in private markets market structure and how standardization, normalization, and transparency of data will transform private markets. Watch here.

🎥 Watch AGM Unscripted at the Goldman Sachs Alternatives Summit with Partners Matt Gibson (here), James Reynolds (here), Kristin Olson (here), Harold Hope (here), Michael Bruun (here), and Jeff Fine (here).

🎥 Watch Lexington Partners’ Partner Taylor Robinson share details about the evolution of the secondaries market and why secondaries are in the spotlight. Watch here.

📝 Read The AGM Q&A with Blue Owl Senior MD and CEO of Global Private Wealth Sean Connor on how they are serving the wealth channel in 2026 and beyond. Read here.

🎥 Watch Ultimus Fund Solutions’ CEO Gary Tenkman discuss how Ultimus is helping to build core fund administration infrastructure that powering the evergreen evolution and is helping to make private markets go mainstream. Watch here.

🎥 Watch Goldman Sachs’ Partner and Global Head of Private Wealth Management Capital Markets and Global Head of Goldman Sachs Apex Family Office Coverage Sara Naison-Tarajano discuss how Goldman Sachs has built its Apex Family Office Coverage group to serve UHNW families and family offices. Watch here.

📝 Read about the expansion of Alt Goes Mainstream, with the announcement of AGM Community, the creation of the AGM Community RIA Advisory Board, and why we believe that the industry should have small, curated events and community-building efforts. Read here.

🎥 Watch Stonepeak’s MD and CEO of SP+ INFRA Cyrus Gentry discuss the why and the how of bringing infrastructure investing to the wealth channel. Watch here.

🎥 Watch Blue Owl’s Senior MD and President & CEO of Global Private Wealth Sean Connor discuss the firm’s focus on the wealth channel and how the firm is a growth company in a growth industry that is investing in megatrends. Watch here.

🎥 Watch the latest Alts Pulse with iCapital Chairman & CEO Lawrence Calcano where we go global and discuss Lawrence’s recent trip to Asia to peer into the nuances of the different wealth management markets around the globe. Watch here.

🎥 Listen and watch EQT’s Chairperson EQT Asia and Head of Private Capital Asia Jean Eric Salata share reflections on leadership, culture, and values from one of the world’s largest investment firms. Listen here and Watch here.

🎥 Listen and watch EQT’s Founder and Chairperson Conni Jonsson discuss how EQT has built a global private equity firm the Nordic way. Listen here and Watch here.

🎥 Watch Vista Equity Partners’ President and COO David Breach discuss how Vista has built a software investing powerhouse in the age of AI. Watch here.

🎥 Watch ING’s Anneka Treon, Global Head of Private Banking, Wealth Management & Investments, and Johan Kloeze, Head of Private Banking & Wealth Management NL, ING, share lessons learned from building a private markets platform for private wealth clients. Watch here.

🎥 Watch Oaktree Capital Management’s Co-CEO and Head of Performing Credit Armen Panossian share why investors shouldn’t “have to reach for risk to generate the right return.” Watch here.

🎥 Watch Franklin Templeton’s COO - Global Wealth Management Alternatives George Stephan discuss the evolution of Franklin Templeton’s Alternatives business and how the firm has brought public and private together. Watch here.

🎥 Watch iAlta Holdings’ Founding Partner Bill Crager discuss the evolution of wealthtech from building Envestnet as Co-Founder and CEO to why today is a “transformational moment” in wealth management. Watch here.

🎥 Watch Vista Equity Partners’ Founder, Chairman, and CEO Robert F. Smith discuss who will benefit from AI and how he built a $100B enterprise software scaled specialist firm. Watch here.

🎥 Watch Nomura Capital Management’s CEO Robert Stark discuss how they have built a private credit firm within a global bank. Watch here.

📝 Read The AGM Op-Ed with Blue Owl Senior MD and Head of Digital Infrastructure Matt A’Hearn on building the backbone of the digital economy. Read here.

🎥 Watch PGIM’s Global Head of Alternative Investments Dominick Carlino discuss the evolution of distributing alternative investments to the wealth channel. Watch here.

🎥 Watch Blue Owl’s Senior MD and Head of Digital Infrastructure Matt A’Hearn share why he believes there’s a generational opportunity in financing digital infrastructure. Watch here.

🎬 Watch AGM Originals The DNA - Season 1 with conversations with EQT’s Conni Jonsson, Jean Salata, Lennart Blecher, Geraldine O’Keeffe, Peter Beske Nielsen, Peter Aliprantis, Hari Gopalakrishnan, William Vettorato, and Ken Wong about the firm’s DNA and its different investing capabilities. Watch here.

🎥 Watch PGIM’s Head of Multi-Asset and Quantitative Solutions Phil Waldeck discuss the intersection of insurance and asset management. Watch here.

🎥 Watch Stonepeak Chairman, Co-Founder, CEO Mike Dorrell share his story as a pioneer in infrastructure investing. Watch here.

🎥 Watch Hg Partner and Head of Value Creation Chris Kindt discuss AI’s transformative role in value creation for private equity. Watch here.

🎥 In Permira Part 2, watch Permira Co-Chairmen & Co-CEOs Brian Ruder and Dipan Patel discuss how the collaborative leadership model in action has helped the firm scale to an €80B alternative asset manager. Watch here.

🎥 Watch Permira Co-Chairman & Co-CEO Dipan Patel discuss how to scale an €80B alternative asset manager. Watch here.

🎥 Watch Morningstar CEO Kunal Kapoor cover the most pressing topics in private markets today, including the convergence of public and private, liquidity vs illiquidity, investor education, the importance of transparency, and the why, what, and how behind evergreen funds. Watch here.

🎥 Watch The Compound and Friends (TCAF) Co-Hosts and Ritholtz Wealth Management Partners Downtown Josh Brown and Michael Batnick and I go back and forth about private markets on TCAF Episode 207. Watch here.

🎥 Watch Stonepeak Co-President Luke Taylor discuss what it takes to be a great infrastructure investor. Watch here.

🎥 Watch Arcesium MD and Head of Client and Partner Development David Nable discuss how to architect private markets technology infrastructure for the future. Watch here.

🎥 Watch Hg Senior Partner and Executive Chairman Nic Humphries discuss how Hg has grown into a $100B scaled specialist and how one of the industry’s leading private equity technology and services investors is “navigating investing at an inflection point in history.” Watch here.

🎥 Watch EQT Partner, Head of Private Wealth Americas Peter Aliprantis live from Miami on how EQT is bringing global local. Watch here.

📝 Read The AGM Op-Ed with Arcesium SVP, Business Development - Private Markets Jean Robert on why asset managers need to rethink reporting as a strategic advantage. Read here.

🎥 Watch Blue Owl Co-President and Global Head of Real Assets Marc Zahr share the story of how he built Oak Street from $17M in AUM in 2009 to what is now Blue Owl’s $67.1B AUM Real Assets business in a live Alt Goes Mainstream podcast at Future Proof Citywide. Watch here.

🎥 Watch Hg’s Partner and Head of Hg Wealth Martina Sanow discuss how Hg has unlocked opportunities for the wealth channel to invest in Europe’s largest portfolio of software and services businesses. Watch here.

🎥 Watch Goldman Sachs’ Partner and Global Co-Head of the Petershill Group at Goldman Sachs Robert Hamilton Kelly discuss the evolution of the GP stakes industry and how Goldman has become a market leading GP stakes investor. Watch here.

🎥 Watch Blue Owl’s MD, Head of Alternative Credit Ivan Zinn unpack private credit and why ABF has become a prominent part of the private credit ecosystem. Watch here.

📝 Read The AGM Op-Ed with Blue Owl Head of Alternative Credit Ivan Zinn on why “asset-based finance today mirrors the evolution of corporate direct lending from over a decade ago.” Read here.

🎥 Watch Krilogy’s Partner and CIO John McArthur discuss how an RIA can chart a growth path by building out its private markets capabilities. Watch here.

🎥 Watch New Mountain Capital’s Founder & Chief Executive Officer Steve Klinsky discuss how $55B AUM New Mountain has built a business that builds businesses. Watch here.

🎥 Watch Arcesium’s Private Markets Head Cesar Estrada discuss data silos and technology integrations in private markets. Watch here.

🎥 Watch GeoWealth President & COO Jack Hannah and iCapital SVP, Partnerships Michael Doniger discuss the ground-breaking BlackRock, iCapital, and GeoWealth unified managed account partnership live from iCapital Connect. Watch here.

🎥 Watch Goldman Sachs’ Managing Director, Global Head of Alternatives, Third Party Wealth Kyle Kniffen discuss how they are “standing on the shoulders of Goldman Sachs to be a complete partner” for the wealth channel. Watch here.

🎥 Watch Fortress Investment Group Managing Director & Co-Head of Private Wealth Solutions Adam Bobker discuss how Fortress has built a wealth solutions business from a whiteboard, leaning on the firm’s pioneering history of innovation. Watch here.

🎥 Watch Constellation Wealth Capital President & Managing Partner Karl Heckenberg on why there will be a $1T independent wealth management firm. Watch here.

🎥 Watch BlackRock Managing Director, Co-Head of US Wealth Business, Senior Sponsor for Retirement Business Jaime Magyera and iCapital Chairman & CEO Lawrence Calcano discuss the ground-breaking BlackRock, iCapital, and GeoWealth unified managed account partnership live from iCapital Connect. Watch here.

🎥 Watch KKR Partner & Co-CEO of KKR Private Equity Conglomerate LLC (K-PEC) Alisa Wood discuss how the firm has innovated in private markets, why KKR came up with the Conglomerate structure, and how evergreens can play a role in investors’ portfolios. Watch here.

🎥 Watch Cantilever Group’s Co-Founder and Managing Partner Todd Owens in a live podcast from BTG Pactual’s NYC office share why GP stakes can be the best of all worlds. Watch here.

📝 Read The AGM Op-Ed with Arcesium Private Markets Head Cesar Estrada on the rise of asset-based finance and why it’s the next growth engine for private credit. Read here.

🎥 Watch BlackRock’s Head of the Americas Client Business Joe DeVico, Head of Product for US Wealth & Head of Alts to Wealth Jon Diorio, and Partners Group's Co-Head of Private Wealth Rob Collins discuss their landmark private markets model portfolio partnership that could be the industry’s “iPhone Moment.” Watch here.

🎥 Watch Brookfield Oaktree Wealth Solutions CEO John Sweeney discuss how to build a high-performing wealth solutions team and why the word “solutions” matters when working with the wealth channel. Watch here.

🎥 Watch Cerity Partners’ Partner & Chief Client Officer Tom Cohn and Partner Amita Schultes talk about how and why they have combined a leading OCIO with a $100B AUM wealth management practice. Watch here.

🎥 Watch Marc Lipschultz, Co-CEO of Blue Owl, talk about how they have aimed to skate where the puck is going as Blue Owl has grown its AUM to $265B in nine years. Watch here.

📝 Read The AGM Q&A with Blue Owl Co-CEO Marc Lipschultz, where he highlights some of the trends that have propelled alternative asset management into the mainstream: scale, a focus on private credit, and a focus on private wealth. Read here.

🎙 Listen to Stephanie Drescher, Partner & Chief Client & Product Development Officer of Apollo, discuss what is safe and what is risky as she dives into both the convergence between public and private and the nuances of asset allocation. Listen here.

🎥 Watch Joan Solotar, Global Head of Private Wealth Solutions at Blackstone share why it’s not even early innings, but that it’s “spring training” for private markets adoption by the wealth channel. Watch here.

🎥 Watch Venkat Subramaniam, Co-Founder of DealsPlus on building a single source of truth for private markets. Watch here.

🎥 Watch Hamilton Lane Managing Director, Co-Head US Private Wealth Solutions Stephanie Davis and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the third episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch KKR Managing Director, Head of Americas, Global Wealth Solutions (GWS) Doug Krupa and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the second episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch Vista Equity Partners Managing Director, Global Head of Private Wealth Solutions Dan Parant and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the first episode of the Investing with an Evergreen Lens Series. Watch here.

📝 Read about a year in the book of alts — a compilation of the 1,000+ pages written in weekly newsletters on Alt Goes Mainstream in 2024. Read here.

📝 Read about the launch of the AGM Studio, a collaboration between Alt Goes Mainstream and Broadhaven Ventures to incubate, invest in, and help scale companies and funds in private markets. Read here.

🎥 Watch Stepstone Private Wealth CEO Bob Long discuss StepStone Private Wealth’s edge and nuances with their evergreen structures in the first episode of “What’s Your Edge.” Watch here.

🎥 Watch Co-Founder & Managing Partner of Cantilever Group and former Goldman Sachs and Broadhaven Capital Partners Partner Todd Owens discuss the middle market opportunity in GP stakes investing. Watch here.

🎙 Hear me discuss why and how alts are going mainstream on The Compound’s Animal Spirits podcast with Ritholtz Wealth’s Michael Batnick and Ben Carlson. Listen here.

📝 Read about the evolution of GP stakes, why alternative asset management business models are better than SaaS, and our partnership with Todd Owens and David Ballard at Cantilever, a mid-market GP stakes firm anchored by BTG Pactual. Read here.

🎙 Hear how Chris Long, Chairman, CEO, and Co-Founder of Palmer Square Capital Management has built a $29B credit investment firm and a winning NWSL soccer franchise, the KC Current. Listen here.

🎙 Hear stories from building market-defining companies Blackstone, Airbnb, and private markets from Laurence Tosi, former CFO of Blackstone and Airbnb and Managing Partner & Founder of $7.6B investment firm WestCap. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear Blackstone CTO John Stecher discuss how technology is transforming private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with both a macro and VC lens. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me and Alt Goes Mainstream on LinkedIn (and AGM’s LinkedIn page), Twitter (@michaelsidgmore), and YouTube to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Cameron Molnar, Ryan McCormack, Nick Owens, Michael Rutter for their contributions to the AGM Index section of the newsletter.

Disclaimer: Alt Goes Mainstream is an independent newsletter focused on the private markets industry. It is published for informational and educational purposes only and does not constitute investment advice, financial advice, legal advice, or any other form of professional advice. Nothing contained herein should be construed as a recommendation to buy, sell, or hold any security or investment product. The views expressed are solely those of the author and do not represent the views of any affiliated organization, employer, or third party. Some companies, individuals, or organizations featured or mentioned in this newsletter may be current or past sponsors of Alt Goes Mainstream. Sponsorship does not influence editorial coverage, but readers should be aware that a relationship might exist. The author may hold direct or indirect investments in companies, funds, or other entities mentioned in this newsletter.