AGM Alts Weekly | 6.15.25: Europe's time?

AGM Alts Weekly #107: Making private markets more public, every week.

👋 Hi, I’m Michael.

Welcome to AGM, the meeting place for private markets.

I’m excited to share my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in private markets so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Presented by

For too long, private equity funds have relied on manual processes — spreadsheets, scattered documents, disjointed data — to track complex investment and ownership structures. It’s slow, error-prone, and not scalable. And when regulators, investors, or auditors come knocking, it’s a fire drill every time.

At DealsPlus, we help private equity funds digitise investment and ownership structures, eliminating data silos. Our software helps power key workflows such as: quarterly reporting, audits, compliance, and exits.

Good morning from London.

As I walked down King’s Road in London yesterday, I heard the deafening boom of the British Royal Air Force planes flying overhead for the Trooping the Colour to mark the King’s official birthday. I couldn’t help but think about news of Blackstone’s announcement to increase its investment in Europe in the coming years.

Blackstone celebrated its 25th anniversary in London this past week.

The bigger news?

Blackstone’s Co-Founder Stephen Schwarzman said in an interview with the Financial Times last week that the firm is planning to invest “at least $500 billion” in Europe over the coming decade.

In a world where money talks, actions speak louder than words.

Just how big of a deal is the decision by Blackstone to signal that it will direct $500B in capital into Europe?

For context, Blackstone, which manages $1.2T in AUM, deployed $133.9B - in total - during 2024.

$50B deployed per year in Europe over the next ten years would represent a significant amount of Blackstone’s overall capital being deployed into the region.

Changing of the guard?

Schwarzman’s comments were underpinned by a changing of the guard in investor optimism for Europe.

In the interview, Schwarzman noted “We are seeing signs of change now in Europe. European leaders are generally becoming more sensitive to the fact that growth rates over the past decades have been quite low and it’s not sustainable for them. So they are looking at putting pressure on the European Union regarding deregulation. We think Europe has the prospect of doing better than they had in the past.”

Blackstone currently holds around $350B in assets across Europe, according to a video that celebrates the 25th anniversary of the opening of their European office.

By the looks of it, it appears Blackstone’s next 25 years in Europe will feature an even bigger commitment to the region.

Schwarzman said “Doing $500B [in investments] in ten years is clearly an acceleration.”

What is driving Blackstone’s increased interest in Europe?

According to Schwarzman, it’s largely around confidence in economic reforms that points towards increased deregulation in a region that’s large in size but more fragmented in culture and regulatory regimes.

Schwarzman also noted the gap in valuations in public and private markets — European companies have lower valuations than many of their US-listed peers. Schwarzman said a similar phenomenon is the case in private markets: “There are valuation differences obviously between the United States and Europe that we find in the private equity and real estate areas, as well as infrastructure.” But he also makes the point that economic reforms and declining interest rates are also important features of an attractive investment environment.

There’s likely another reason: political stability.

At SuperReturn, Blackstone’s Vice Chairman Thomas Nides said that increased political stability in France, Germany, and the U.K. means “shifting money into Europe is certainly not a bad bet.”

Blackstone isn’t the only firm that is putting its money where its mouth is with respect to intensifying its investing efforts in Europe.

Top of mind

Last week’s SuperReturn conference featured a number of the industry’s largest asset managers discussing the attractive European investment opportunity.

Blair Jacobson, Co-President of Ares Management, told the attendees at SuperReturn that there was a “feeling right now that European markets are very attractive” in an article from CNBC on the event.

Jacobson noted falling interest rates and Germany’s 500B Euro fiscal package, as did last year’s Draghi report, which has encouraged deregulation and increasing European competitiveness.

Jacobson said that “Europe is growing up and taking control of its own destiny, which can be positive for macro trends,” noting that there was more of a pull factor into Europe for investors, according to an article from CNBC.

Other industry peers echoed a similar sentiment at SuperReturn.

Sixth Street Co-CIO Julian Salisbury said “There’s a real opportunity for private capital [in Europe] to invest at lower valuations. There are still great businesses here.” Salisbury also called out the valuation gap as a driver of capital flows into Europe in a panel moderated by CNBC’s Leslie Picker. “Last year, everybody seemed all-in on growth in the U.S. That’s usually a sign you should start considering other options.”

But investing in Europe isn’t easy, particularly with different cultures and regulatory regimes. Goldman Sachs Asset Management’s Global Co-Head of Private Credit James Reynolds told CNBC’s Julianna Tatelbaum how much of a challenge it is to invest in Europe without the right firm infrastructure.

“The barriers to entry and the barriers to compete in Europe, we find are a bit higher than maybe anywhere else, you’re getting paid for complexity. You need to have offices all over. You need real presence, local presence. You don’t do a deal in the same way in northern Europe, Southern Europe,” Reynolds said.

Reynolds surfaces a theme that has perhaps defined why some firms that have European heritage have built such impressive investment engines and delivered on performance for investors.

Local but global

The very same features that make Europe a more challenging investment landscape also make it a favorable ecosystem for certain investors. For firms that are able to navigate local nuances, the opportunity is there for the taking.

Europe is the world’s third-largest economy — and a leader in sustainability and social standards, as a McKinsey & Company report on Europe notes.

Europe is aware that despite its position in the world economy it needs to rev up its engines to kickstart growth. Mario Draghi’s European competitive agenda laid out a need for additional investment of €800B annually between 2025 and 2030.

How can that be financed? By private capital.

Currently, European Union’s private capital sector is roughly half the scale of the United States’ when measured by AUM relative to GDP and investments. The European competitiveness agenda could unleash capital flowing into the system in droves: the level of private capital investment required to meet the standards of the competitiveness agenda is €100-150B more than the €100-150B invested today, according to McKinsey’s article.

McKinsey lays out a $4T investment gap to fill by 2030.

The good news for Europe?

Much of the investment opportunity in Europe centralizes around megatrends that many of the industry’s largest asset managers are well-equipped to finance.

Themes like decarbonization and financing the energy transition, building critical infrastructure, digitalization and AI, defense and security, and boosting productivity and outcomes in sectors like healthcare, education, energy, and financial services all require large amounts of capital.

The industry’s biggest players seem ready to meet the moment to fill this capital gap.

And Europe hasn’t been a bad place for both LPs and GPs to invest for outperformance.

In fact, private capital has outperformed public market equivalents for the past 20 years in Europe — and at an even higher rate than in the US.

Private capital funds in Europe have returned 1.2x the value of their public market equivalents during the past 20 years, compared with 1.1x in the US.

And in the past six years? EU value was as much as 1.4x that of its public market equivalents.

The opportunity to invest in Europe is there. Who will be well-positioned to win?

Scale matters

It’s hard to start this thought exercise without mentioning the firms that have the scale to invest in Europe.

They may not have European heritage in the same way that some of Europe’s homegrown high-quality private equity firms do, but they have the size, scale, and boots on the ground to both invest in the region and work well with the wealth channel.

When a firm like Blackstone signals that it will put $500B — or more — to work over the next ten years, it’s hard to ignore their ability to win parts of the market.

As former Blackstone CFO and WestCap Founder and Managing Partner Laurence Tosi said on an Alt Goes Mainstream podcast, scale itself can be a competitive advantage.

On our podcast, I asked L.T. about how alternative asset managers can balance scale with returns. His answer was fascinating.

Michael: That brings up such a fascinating point. I think it was Steve Schwarzman who said, scale is our niche. And that's such an interesting comment when you think about investing because when I think about that, I think about how do you balance the equilibrium of scale, as many of these firms like Blackstone and others are building, and the value that's created from that liquidity, like you say, with returns. And that's the other side of that for the investors and the other side of that marketplace, and generally, returns can be harder to come by the more scale you have. Because as more capital comes into a space, it gets harder to generate returns. How do you think about scale in the context of alternative asset managers and what's happening in private markets? And then how you balance that with returns while thinking about just the building of these marketplace businesses?

L.T.: I remember when Steve said that. That scale is niche. I'm going to add a second part, Michael, to that statement, which I guess gets less covered than he would say. He would also say that scale begets skill. And the more skill you can put against creating value, the more you can justify the scale [author emphasis]. So in the early days of Blackstone, shortly after we went public, there was a lot of confusion about, well, how's this different from The '40 Act shops that do mutual funds, et cetera. And the answer was we found businesses where skill really matters, i.e., finding businesses and knowing how to turn them around. And then we found a little bit of the golden rule that the more scale that we had, the more resources we would have at Blackstone to invest in creating alpha, if you want to call it that, or value creation. And so the scale actually made us more competitive. So, if I think back to when I joined the firm, I think our private equity fund was six billion, and our real estate fund was probably three billion. Those are about now both 30. That difference in those is not just adding more assets like you would to a mutual fund or a hedge fund. Those assets have translated to deep operating teams, asset management teams that can actually help create value during the course of the whole [author emphasis]. Also, going out and finding more deals, negotiating them. The golden rule in investing is where can you find a space that the more you invest in your returns, the greater the alpha you generate was. That's the right place to scale [author emphasis]. If you don't have that, then scale doesn't create what Steve said. It’s not your niche and doesn't create value. So that was the guiding force behind how that was built out.

L.T.’s comment at the end is quite interesting — and pertinent when it comes to understanding both why Blackstone is perhaps compelled to invest in Europe and why they are thinking of moving at such size and scale.

L.T. said, “the golden rule in investing is where can you find a space that the more you invest in your returns, the greater the alpha you generate was. That's the right place to scale.”

Perhaps that explains why Blackstone and its peers — KKR, Apollo, Ares, Brookfield, Blue Owl, EQT, and others — are turning such an intense focus to Europe.

A few weeks ago, Apollo President Jim Zelter said that the firm plans to invest as much as $100B in Germany alone over the next decade.

Even scaled specialist firms, like Thoma Bravo, have made Europe a strategic priority. Thoma Bravo recently planted a flag in Europe by opening a European HQ and has ramped up its deal activity.

Thoma Bravo opening up a European HQ is notable. It brings us to the next key feature of winning in Europe: being local matters.

“Locals with locals”

EQT has branded itself as a firm that has taken a localized approach to winning in markets and regions.

The firm has made its “locals with locals” mindset a core part of its philosophy.

Take it from EQT’s website, where they emphasize the importance of possessing local knowledge, which comes from having local business relationships and a local presence as an integral part of their investment playbook.

The local element of investing in Europe is critically important to investment success. While Europe is a large market and economy, despite a number of shared values, at times, it can be broken up into a disparate set of cultures, norms, and regulatory regimes.

That feature of Europe makes having a local presence and understanding of the culture of a particular country a crucial ingredient for firms looking to invest well in Europe.

Firms that have the ability to invest in building a local presence will put themselves in a position to succeed. This will impact everything from investment returns to the ability to create and manage evergreen fund strategies and work with the wealth channel. In a world where evergreen funds matter, dealflow is key. Firms must have enough dealflow to be able to support running and managing an evergreen structure. In Europe? That means having enough boots on the ground in key hubs across the region to be able to actively build and manage relationships that lead to ample dealflow.

Which types of firms have the ability to both cover enough end markets with boots on the ground and have the capability to invest enough resources into doing that well?

Scaled specialists.

Specialists with scale

In addition to the multi-strategy scaled platforms that have both the size and capital to invest in covering Europe well (and have done for years past), it’s the scaled specialists that appear to have an opportunity to cover Europe well.

That could be either because they’ve built their business in Europe, creating a brand and culture that is distinctly European, or because they have the size to be able to invest heavily into building a European presence and brand.

There are a number of firms with the size and capabilities to continue to win in Europe in categories where they are distinctly unique and strong firms.

A non-exhaustive list would include firms with European heritage, such as Hg and Permira, in software investing, as well as US firms with track records and specialist brands that are investing heavily in building out a European presence, like Thoma Bravo and Vista.

In categories like infrastructure, where so much capital is required to fill the demand to usher in the development of megatrends, a scaled specialist like Stonepeak might excel.

A firm like Hg has grown to over $85B in AUM by being a focused enterprise software investor in categories they possess deep knowledge and by having a “sleep well” investment strategy, as a slide from the publicly available presentation from its UK-listed investment trust, HgTrust, illustrates.

Hg, which has over 70% of its portfolio headquartered in Europe, has a number of stories of investment success by investing in a market leader and winner that won its home market first. Visma, P&I, and IFS are all examples in the Hg (and some of its investing peers’) portfolio.

In some respects, European companies have to do the hard part earlier on in its company’s life. Yes, they have to win their home markets, as Norwegian company Visma did in the Nordics and P&I did in Germany, but then they have to figure out how to expand pan-regionally, as Visma also did. That has included building out strong in-country teams as they’ve moved to new countries — and building an engine to acquire companies in specific countries or competencies that can fuel growth. Just last year, Visma made 11 acquisitions across Europe, including Finthesis, the fifth acquisition in the French market in 2024, and a handful of companies in the Benelux markets.

While the US market, particularly software companies, have been the apple to the eyes of many software investors public and private, the European markets have growth stories, too.

Visma is perhaps one of Europe’s best examples of this growth story for a European grown software business.

In 2023, when Visma did a share sale at $21B valuation to fund international expansion, Hg Senior Partner and Executive Chair Nic Humphries discussed Visma’s remarkable growth in a Reuters article.

“Today Visma is Europe's largest private equity owned software business, growing twice as fast now compared to when we first invested in 2006, despite having become a business that's over 20 times larger,” said Humphries.

Firms that have a technology bias to their investing, as well as focus on AI, could also do well in Europe. Europe is becoming a hub for AI talent, which should bode well for software specialist investors like Hg, Thoma Bravo, and Vista, amongst others.

Some of the fastest-growing companies in AI — Mistral, Lovable, Granola.ai, Fyxer.ai, to name a few — have been built in Europe, which have already hit the radar of growth and private equity firms due to their rapid growth.

“Fortune favors the small and the brave”

The mid-market also represents an opportunity for European firms — and for US or international investors looking to gain exposure to a region on the rise.

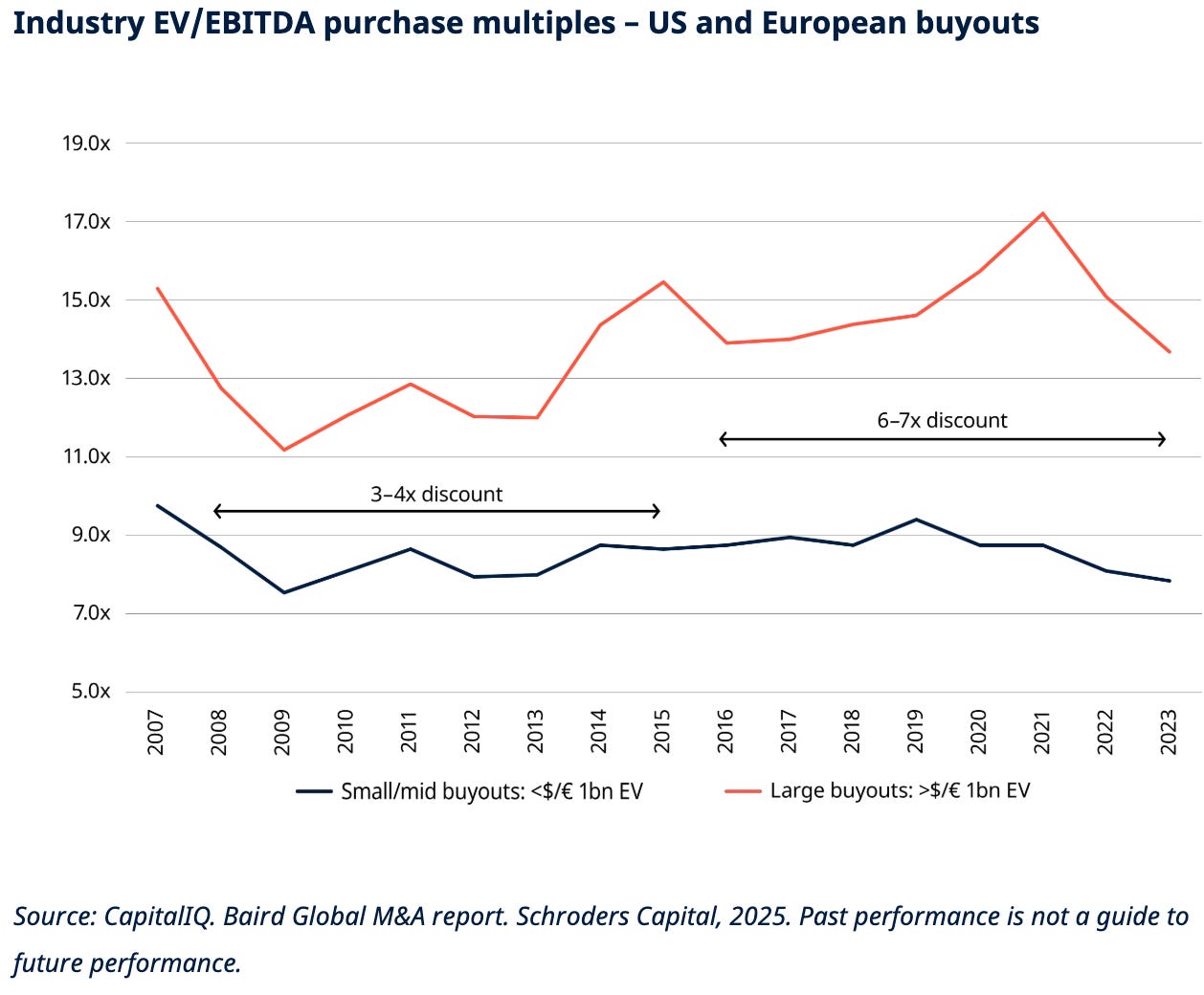

Purchase price does matter (as Apollo often says) — and that’s particularly the case in the middle market.

The European middle market tends to have lower entry prices, which can help to create better return outcomes, as the below illustration from a Schroders Capital article highlights.

Returns in Europe, particularly in the middle market, have also outpaced other regions, as the below chart from Invest Europe (based on Cambridge Associates data up to 2024) shows.

What does the possible outperformance of the European middle market private equity landscape mean for the region?

Perhaps, given how important it is to have a local presence and brand, as well as a deep understanding of the cultural nuances of European markets, US firms will look to acquire European alternative asset managers.

That would seem to bode well for European-focused GP stakes firms like Armen and AXA IM Prime, which are based in Europe and solely focused on the European asset management landscape, in addition to larger players like Blue Owl and Petershill, which are actively covering the space. European firms look to be open to selling a stake, as a 2023 Dechert survey found that 57% of EMEA GPs were planning to take in a GP stake over the next 24 months.

Who will be the new kings in private capital? Other regions of the world will still be important in the investing landscape, but perhaps a number of the industry’s leading firms will emerge from Europe or maintain dominance because of a focus on investing in Europe going forward.

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

AGM Post of the Week

Blackstone celebrated the 25th anniversary of planting its flag in Europe. This past week, the firm announced that it would be investing at least an additional $500B into the region over the next ten years.

AGM News of the Week

Articles we are reading

📝 Avoid the 'gateway drug': How and why $130bn Cerity Partners reinvests profits | Sam Bojarski, Citywire

💡 $130B AUM Cerity Partners CEO Kurt Miscinski discussed the importance of organic growth at Citywire RIA’s CIO Summit, reports Citywire’s Sam Bojarski. Miscinski dissected the firm’s rapid growth, which has included a focus on reinvesting profits back into the business. “We’ve always invested 100% of our profitability into the business,” Miscinski told Citywire, adding that he was intent on avoiding an overreliance on distribution cash flow. “I tell my colleagues and partners that distributions can ultimately become a gateway drug,” he said. Miscinski noted that the lion’s share of the firm’s capital expenditures is directed towards its team, which has grown to over 1,500 people through both organic growth and M&A. Almost 1/3 of the firm is focused on what Miscinski described as oriented on “how [they] become a better firm.” Miscinski noted that Cerity Partners is making significant investments into marketing and business development.

Building brand is critical in the mind of Miscinski.

Cerity Partners helps its individual partners and its advisory practices grow their personal brands as they look to showcase specialization and their differentiating features to clients.“All of our partners and our partner practices, we have partner landing pages, many of our partners are proactive in content writing,” Miscinski said. “Effectively, we want to promote our talent.”

💸 AGM’s 2/20: It’s not just asset managers that need to focus on building brand; it’s wealth managers too. Miscinski’s comments echo that of the asset management industry’s largest players. Much of the strategy that Cerity Partners seems to be employing appears to be very similar to how the industry’s largest traditional and alternative asset managers are building their brand. Alternative asset managers, like Blackstone, KKR, Apollo, Blue Owl, EQT, and others, have turned a heavy focus to brand-building to resonate with both companies and prospective investors. Wealth managers would do well to follow the blueprint of asset managers who have cracked the code on how to build brand well. It appears that Cerity Partners is very much on that track — and, importantly, is making the investment required to do it well. It’s an interesting development to think about as the asset management industry and wealth management industry become increasingly inextricably linked. It’s impossible to talk about the rise of the wealth channel as a major LP without referencing how private equity is playing an increasing role in helping to determine the growth of the wealth management space. This has manifested itself in helping many of the large RIAs build out investment functions that can properly source, diligence, vet, invest, and manage investments into private markets, just as an institutional investor would. That’s in part why the industry has seen firms like Cerity Partners merge in OCIO businesses like Agility, and Hightower acquire NEPC (you can listen to Cerity Partners’ Tom Cohn and Amita Schultes share thoughts on the merger between Cerity Partners and Agility on the Alt Goes Mainstream podcast here). It’s also why we’ll likely see increasing crossover between wealth management and asset management, both in the form of investment and how these businesses themselves evolve, as Constellation Wealth’s Karl Heckenberg discussed on his Alt Goes Mainstream podcast.

Another notable development at the intersection of asset management and wealth management occurred this past week, with BlackRock, via recently acquired HPS Investment Partners, taking a minority stake in $30B AUM Lido Advisors, which already features investment from Charlesbank and Constellation Wealth Capital. If there’s a firm that has figured out how to build brand well in traditional asset management and became a pioneer for educating investors on ETFs and model portfolios, it was BlackRock. Perhaps BlackRock will take some of that know-how and experience and share that with Lido as the firm looks to be on a growth path to $100B in AUM.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know, and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Blackstone (Alternative asset manager) - Private Wealth Solutions - Content Marketing, Vice President - Tokyo. Click here to learn more.

🔍 KKR (Alternative asset manager) - Global Wealth Solutions - Investor Relations - Principal. Click here to learn more.

🔍 Apollo Global Management (Alternative asset manager) - Vice President, Strategy & Innovation – Model Portfolios and Annuity Solutions. Click here to learn more.

🔍 Ares (Alternative asset manager) - Vice President, Product Management & Client Services, Wealth Management Solutions, APAC. Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Strategy & Corporate Development Associate. Click here to learn more.

🔍 Franklin Templeton (Asset manager) - Head of Marketing - France, Benelux, and the Nordics. Click here to learn more.

🔍 BlackRock (Asset manager) - Global Head of Product Strategy, Private Market Solutions - Managing Director. Click here to learn more.

🔍 Brookfield (Alternative asset manager) - SVP - GCG Head of Content Strategy. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - RIA, Family Office Business Development - Vice President. Click here to learn more.

🔍 Arcesium (Private markets technology company) - SVP Business Development, Private Markets. Click here to learn more.

🔍 Goldman Sachs Alternatives (Alternative asset manager) - Private Markets for Wealth - Executive Director - Frankfurt. Click here to learn more.

🔍 Ultimus Fund Solutions (Fund administrator) - SVP, Business Development. Click here to learn more.

🔍 Lincoln Financial (Insurance) - Alternative Investment Sales Specialist Account Executive. Click here to learn more.

🤝 Interested in partnering with Alt Goes Mainstream? 🤝

Alt Goes Mainstream is a community of engaged experts and executives in private markets.

Fill out this form using the link below to explore partnership opportunities.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

📝 Read The AGM Op-Ed with Blue Owl Head of Alternative Credit Ivan Zinn on why “asset-based finance today mirrors the evolution of corporate direct lending from over a decade ago.” Read here.

🎥 Watch Lincoln Financial’s EVP and CIO Jayson Bronchetti discuss the role of insurance companies in private markets as he discusses how he manages a portfolio of $300B in assets. Watch here.

🎥 Watch Krilogy’s Partner and CIO John McArthur discuss how an RIA can chart a growth path by building out its private markets capabilities. Watch here.

🎥 Watch New Mountain Capital’s Founder & Chief Executive Officer Steve Klinsky discuss how $55B AUM New Mountain has built a business that builds businesses. Watch here.

🎥 Watch Arcesium’s Private Markets Head Cesar Estrada discuss data silos and technology integrations in private markets. Watch here.

🎥 Watch GeoWealth President & COO Jack Hannah and iCapital SVP, Partnerships Michael Doniger discuss the ground-breaking BlackRock, iCapital, and GeoWealth unified managed account partnership live from iCapital Connect. Watch here.

🎥 Watch Goldman Sachs’ Managing Director, Global Head of Alternatives, Third Party Wealth Kyle Kniffen discuss how they are “standing on the shoulders of Goldman Sachs to be a complete partner” for the wealth channel. Watch here.

🎥 Watch Fortress Investment Group Managing Director & Co-Head of Private Wealth Solutions Adam Bobker discuss how Fortress has built a wealth solutions business from a whiteboard, leaning on the firm’s pioneering history of innovation. Watch here.

🎥 Watch Constellation Wealth Capital President & Managing Partner Karl Heckenberg on why there will be a $1T independent wealth management firm. Watch here.

🎙 Listen to Ted Seides, Founder of Capital Allocators, and I discuss the convergence of the institutional world and the wealth world as we dive into the intersection of private markets and private wealth to kick off a Capital Allocators mini-series on Private Wealth. Listen here.

🎥 Watch BlackRock Managing Director, Co-Head of US Wealth Business, Senior Sponsor for Retirement Business Jaime Magyera and iCapital Chairman & CEO Lawrence Calcano discuss the ground-breaking BlackRock, iCapital, and GeoWealth unified managed account partnership live from iCapital Connect. Watch here.

🎥 Watch EQT Partner & Head of Private Wealth Americas Peter Aliprantis discuss how the firm is bringing EQT’s success to the US wealth market. Watch here.

🎥 Watch KKR Partner & Co-CEO of KKR Private Equity Conglomerate LLC (K-PEC) Alisa Wood discuss how the firm has innovated in private markets, why KKR came up with the Conglomerate structure, and how evergreens can play a role in investors’ portfolios. Watch here.

🎥 Watch Cantilever Group’s Co-Founder and Managing Partner Todd Owens in a live podcast from BTG Pactual’s NYC office share why GP stakes can be the best of all worlds. Watch here.

📝 Read The AGM Op-Ed with Arcesium Private Markets Head Cesar Estrada on the rise of asset-based finance and why it’s the next growth engine for private credit. Read here.

🎥 Watch BlackRock’s Head of the Americas Client Business Joe DeVico, Head of Product for US Wealth & Head of Alts to Wealth Jon Diorio, and Partners Group's Co-Head of Private Wealth Rob Collins discuss their landmark private markets model portfolio partnership that could be the industry’s “iPhone Moment.” Watch here.

🎥 Watch the third episode of Going Public on Alt Goes Mainstream with Evercore ISI Senior MD and Senior Research Analyst Glenn Schorr as we discuss separating the forest from the trees and Glenn’s “Final Four” firms he would pick in honor of March Madness. Watch here.

🎥 Watch Brookfield Oaktree Wealth Solutions CEO John Sweeney discuss how to build a high-performing wealth solutions team and why the word “solutions” matters when working with the wealth channel. Watch here.

🎥 Watch Cerity Partners’ Partner & Chief Client Officer Tom Cohn and Partner Amita Schultes talk about how and why they have combined a leading OCIO with a $100B AUM wealth management practice. Watch here.

🎥 Watch Marc Lipschultz, Co-CEO of Blue Owl, talk about how they have aimed to skate where the puck is going as Blue Owl has grown its AUM to $265B in nine years. Watch here.

📝 Read The AGM Q&A with Blue Owl Co-CEO Marc Lipschultz, where he highlights some of the trends that have propelled alternative asset management into the mainstream: scale, a focus on private credit, and a focus on private wealth. Read here.

🎙 Listen to Stephanie Drescher, Partner & Chief Client & Product Development Officer of Apollo, discuss what is safe and what is risky as she dives into both the convergence between public and private and the nuances of asset allocation. Listen here.

🎥 Watch Eric Satz, Founder & CEO of Alto share thoughts on why retirement assets could be the next frontier for private markets. Watch here.

🎥 Watch Mike Tiedemann, CEO of $72B AUM AlTi Global share why being a global wealth manager can be a differentiator. Watch here.

🎥 Watch Joan Solotar, Global Head of Private Wealth Solutions at Blackstone share why it’s not even early innings, but that it’s “spring training” for private markets adoption by the wealth channel. Watch here.

🎥 Watch Jeff Carlin, Senior Managing Director, Head of Global Wealth Advisory Services at Nuveen live from Nuveen’s nPowered conference on why “it’s all about the end client.” Watch here.

🎥 Watch Venkat Subramaniam, Co-Founder of DealsPlus on building a single source of truth for private markets. Watch here.

🎥 Watch Yann Magnan, Co-Founder & CEO of 73 Strings discuss the opportunity for AI to automate private markets. Watch here.

🎥 Watch Lawrence Calcano, Chairman & CEO of iCapital on episode 14 of the latest Monthly Alts Pulse as we discuss whether or not private markets has moved from access as table stakes to customization and differentiation. Watch here.

🎥 Watch Hamilton Lane Managing Director, Co-Head US Private Wealth Solutions Stephanie Davis and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the third episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch KKR Managing Director, Head of Americas, Global Wealth Solutions (GWS) Doug Krupa and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the second episode of the Investing with an Evergreen Lens Series. Watch here.

🎥 Watch Vista Equity Partners Managing Director, Global Head of Private Wealth Solutions Dan Parant and iCapital Co-Founder & Managing Partner Nick Veronis discuss the evolution of evergreen funds on the first episode of the Investing with an Evergreen Lens Series. Watch here.

📝 Read about a year in the book of alts — a compilation of the 1,000+ pages written in weekly newsletters on Alt Goes Mainstream in 2024. Read here.

📝 Read about the launch of the AGM Studio, a collaboration between Alt Goes Mainstream and Broadhaven Ventures to incubate, invest in, and help scale companies and funds in private markets. Read here.

🎙 Hear Balderton Capital General Partner and former Goldman Sachs Partner Rana Yared discuss why Europe can build global companies out of the region. Listen here.

🎙 Hear Churchill Asset Management by Nuveen’s MD, Senior Investment Strategist & Co-Head of the Chicago Office Alona Gornick discuss the evolution of private credit, the power of permanent capital, and the importance of the product specialist. Listen here.

🎥 Watch Stepstone Private Wealth CEO Bob Long discuss StepStone Private Wealth’s edge and nuances with their evergreen structures in the first episode of “What’s Your Edge.” Watch here.

🎙 Hear $5B AUM Ritholtz Wealth Management’s Director of Institutional Asset Management Ben Carlson bring a wealth of common sense to asset allocation and private markets. Listen here.

🎙 Hear Blue Owl, Inc. Board Member and Blue Owl GP Strategic Capital Senior Managing Director Sean Ward on how $57.8B AUM Blue Owl GP Strategic Capital has pioneered GP staking and transformed GP stakes into an industry. Listen here.

🎥 Watch Co-Founder & Managing Partner of Cantilever Group and former Goldman Sachs and Broadhaven Capital Partners Partner Todd Owens discuss the middle market opportunity in GP stakes investing. Watch here.

🎙 Hear Intapp’s President, Industries, and Co-Founder of DealCloud by Intapp Ben Harrison discuss how data and automation are transforming private markets. Listen here.

🎙 Hear Bernstein Private Wealth Management’s CIO Alex Chaloff discuss how a $125B wealth manager navigates private markets. Listen here.

🎙 Hear me discuss why and how alts are going mainstream on The Compound’s Animal Spirits podcast with Ritholtz Wealth’s Michael Batnick and Ben Carlson. Listen here.

🎙 Hear Manulife’s Global Head of Private Markets Anne Valentine Andrews share how to approach building a private markets investment platform at an industry behemoth and the merits of infrastructure investing. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, on the AGM podcast discuss driving efficiency across the entire value chain to transform private markets. Watch here.

🎙 Hear VC legend New Enterprise Associates’ Chairman Emeritus and Former Managing General Partner Peter Barris discuss how he transitioned from operator to VC and transformed NEA into a venture juggernaut in the process. Listen here.

🎙 Hear Blue Owl’s Global Private Wealth President & CEO Sean Connor share insights and lessons learned from working with the wealth channel. Listen here.

🎙 Hear Ritholtz Wealth Management’s Managing Partner Michael Batnick share views on how wealth managers are navigating private markets. Listen here.

📝 Read about the evolution of GP stakes, why alternative asset management business models are better than SaaS, and our partnership with Todd Owens and David Ballard at Cantilever, a mid-market GP stakes firm anchored by BTG Pactual. Read here.

🎙 Hear how Chris Long, Chairman, CEO, and Co-Founder of Palmer Square Capital Management has built a $29B credit investment firm and a winning NWSL soccer franchise, the KC Current. Listen here.

🎙 Hear stories from building market-defining companies Blackstone, Airbnb, and private markets from Laurence Tosi, former CFO of Blackstone and Airbnb and Managing Partner & Founder of $7.6B investment firm WestCap. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear Blackstone CTO John Stecher discuss how technology is transforming private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with both a macro and VC lens. Listen here.

📝 Read how 73 Strings CEO & Co-Founder Yann Magnan and team are leveraging AI to build a modern and holistic monitoring and valuation platform for private markets in The AGM Q&A. Read here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, discusses how they approach alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Michael Rutter and Nick Owens for their contributions to the newsletter.