AGM Alts Weekly | 12.15.24: Integration nation

AGM Alts Weekly #82: Making private markets more public, every week.

👋 Hi, I’m Michael.

Welcome to AGM, the meeting place for private markets.

I’m excited to share my weekly newsletter, the AGM Alts Weekly. Every Sunday, I cover news, trends, and insights on the continuing evolution and innovation in private markets. I share relevant news articles, commentary, an Index of publicly traded alternative asset managers, job openings at private markets firms, and recent podcasts and thought pieces from Alt Goes Mainstream.

Join us to understand what’s going on in private markets so you and your firm can stay up to date on the latest trends and navigate this rapidly changing landscape.

Presented by

LemonEdge is a leading fund, partnership, and portfolio accounting solution for private markets investment firms with backing from Blackstone Innovations Investments, amongst others. LemonEdge helps GPs, VCs, Family Offices and Fund Administrators transform their back-office operations, through making the complex, simple.

LemonEdge helps firms manage equity, real estate and infrastructure across closed-ended, open-ended and hybrid structures of any variety, with all management fee, waterfalls or other typical Excel based calculations all embedded in LemonEdge. Scale your operations with high efficiency and deliver exceptional LP / GP service.

Good morning from DC.

Earlier this week, I traveled to Omaha to speak at a meeting with the CFA Society of Nebraska. Lee Martin, Mutual of Omaha’s Head of High Yield Credit (and Alt Goes Mainstream subscriber), kindly invited me to share perspectives on the trends that are driving private markets. He expertly moderated a conversation that covered a lot of ground and included great questions from the audience, many of whom are also in investment management.

While in Omaha, I also had the opportunity to meet with other allocators in the city. It was not lost on me that while I had come to the CFA Society event to share perspectives on the wealth channel (which, in the past, I’ve called one of the new “institutional LPs”), the conversations I had in my meetings with a different cohort of LPs — insurance companies — made it clear that these LPs will continue to play an increasingly prominent role as allocators to private markets.

A number of conversations with insurance companies highlighted their focus on — and dedication to — private markets. Whether they have a fully built team or are earlier on in their journey of allocating to private markets, there’s clearly a desire to understand and invest in private markets in ways that fit their respective investment thesis and philosophy.

This sentiment was punctuated by news this week of $100B AUM alternative asset manager General Atlantic and $609B AUM MetLife Investment Management forming Chariot Re, a life and annuity reinsurance company.

Speaking of insurers allocating to private markets, one of the attendees at the CFA Society event asked a question about BlackRock’s acquisition of HPS and how it would impact both BlackRock and its competitors. A few months prior to BlackRock’s acquisition of HPS, Guardian Life struck a partnership with HPS where they would increase their minority equity stake in HPS and shift the investment management of $30B of assets to HPS across public high yield, investment grade private credit, and real estate debt and equity, in addition to committing up to $5B in new investment grade investments over the next several years.

Presumably, Guardian’s investment in the HPS management company turned out well for them, given BlackRock’s acquisition.

But an interesting topic was embedded in the attendee’s question about BlackRock’s acquisition of HPS: the integration of HPS into BlackRock.

Last week, I wrote about BlackRock’s landmark acquisition of HPS and what it means for the future of their private markets franchise — and beyond.

Surely, the synergies make sense on a multitude of levels. But now, they need to integrate two firms, two cultures, and two ethos together into a single organization. In an industry that’s in the mist of continued consolidation and early on its journey of working with the wealth channel, integration matters more than ever.

Integration nation

The currency of consolidation is greater than ever. Alternative asset managers that are able to expand their platforms by adding new investment strategies, LPs, and AUM are usually able to add to their valuation.

Acquisitions are a way to advance these ambitions.

As the below chart from a 2023 Bain & Company report illustrates, the industry has seen an uptick in acquisitions by the top 50 alternative asset managers. 2021 and 2022 reflected significant increases in the number of acquisitions by top alternative asset managers. Recent acquisitions were punctuated by BlackRock’s $12.5B acquisition of GIP and $12B acquisition of HPS, TPG’s $3.1B acquisition of Angelo Gordon, and General Atlantic’s acquisition of Actis.

The data surely favors firms that can integrate — and integrate well. A June 2024 report from Bain & Company on steps for a successful M&A integration finds that companies that do more M&A deliver better shareholder returns. And scale begets scale, as former Blackstone CFO and WestCap Founder & Managing Partner Laurence Tosi on his Alt Goes Mainstream podcast, so it would make sense that scale often enhances enterprise value. As does practice.

Frequent acquirers tend to achieve even better returns than their less acquisitive peers, with the shareholder returns by frequent acquirers doubling over the past 20 years, from 57% to 130% (note: this Bain report on M&A integration is not specific to alternative asset managers).

But integrations are also challenging. And when acquisitions fail, it’s the integration that’s the culprit. Not some of the time. 83% of the time, according to Bain & Company.

Perhaps this above chart explains why Blue Owl’s Co-CEO Marc Lipschultz recently posted about the firm’s focus on integration planning “long before the deal is closed.”

Blue Owl has been a prime example of an acquisitive firm in private markets. Their origin story started with a merger: bringing together two powerful businesses in private markets, Owl Rock (private credit) and Dyal Capital Partners (GP stakes), in 2021 to create what is today $235B+ AUM Blue Owl. They’ve since supplemented their investment platform in meaningful ways with a number of marquee acquisitions — Oak Street (real estate and what is now their Triple Net Lease business), Prima (real estate), Kuvare (insurance solutions), Atalaya (asset-based finance / direct lending), IPI (digital infrastructure / data centers).

Surely, these integrations couldn’t have been easy, but the rapid growth of Blue Owl’s business would suggest that they’ve figured out how to incorporate established brands or specialist managers into their broader platform and culture to generate benefits for their LPs, their shareholders, and their team.

In Blue Owl’s case, it probably also doesn’t hurt that their GP Strategic Capital business (GP stakes) has relationships with many top alternative asset managers via minority equity stakes. They are able to witness best-in-class operations and cultures and build relationships with managers before they acquire, as they did with $10B AUM Atalaya.

Currency of consolidation

The currency of consolidation has a double meaning.

There’s certainly a lot of value to be captured by scaled platforms adding new strategies and AUM to their business, particularly if they are publicly traded companies. Investors tend to look kindly on alternatives managers that have multiple strategies — and more fee-paying AUM.

The currency of consolidation also refers to the fact that the publicly traded asset managers are the ones that can use the currency of its public company stock to acquire smaller alternative asset managers. Unsurprisingly, it was the publicly traded alternative asset managers that consummated the lion’s share of the strategic acquisitions in recent years, as this chart from a 2023 Bain & Company report illustrates.

This is not a surprising data point, particularly when public shareholders typically look for 15%-plus annual organic growth in fee-paying AUM, according to the Bain report. When expanding to new geographies or new strategies, buying is often quicker than building.

EQT, which has been an acquisitive firm since it went public in 2019, recognized the importance of speed to market. In a Forbes article, EQT’s CEO Christian Sinding noted that their $7.5B acquisition of Barings Private Equity Asia came about because “[they] realized for us to be able to build that scale organically in Asia would probably take another 10 years.”

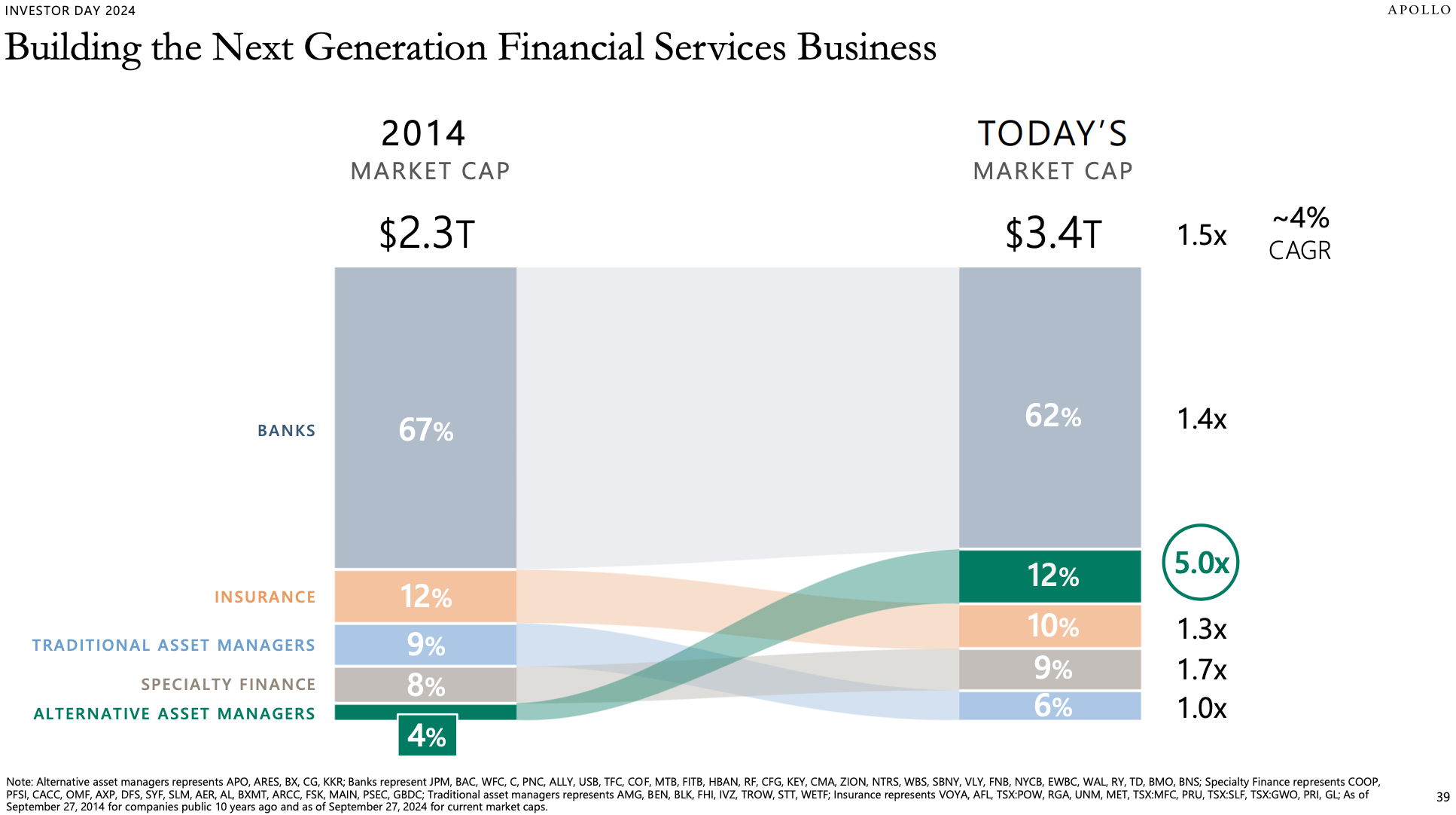

The currency of a public stock can be a double-edged sword. Right now, it appears to be an advantage for the alternative asset managers rather than the traditional asset managers. As the AGM Index often shows, it seems like market capitalizations and stock prices for alts managers go from strength to strength most weeks. Many have certainly had standout performances over the past year and past few years. Targets, of course, will be asking the question of whether these stock prices will continue to perform in the coming years, but it’s clear that alternatives managers are becoming an increasingly larger part of the financial services ecosystem — and the publicly traded equity markets, as a chart from Apollo’s Investor Day presentation shows.

But for traditional asset managers, the trend of outflows in traditional products and, in some cases, a flagging stock price might make target firms think twice about deciding to consolidate into a traditional asset manager.

Culture considerations

As Evercore’s Glenn Schorr said on the first episode of the “Going Public” series, the most important asset for an asset manager is its people: “People, and then people, and then some good people,” is what he said.

Talent is critical in the asset management business. In an acquisition, it’s imperative that talent is both appropriately compensated and motivated.

The other critical element of talent (which can enhance — or detract — from talent)? Culture.

How two firms integrate their cultures is crucial in achieving success in both investment performance and building an investment firm’s continued culture.

There are a host of questions that asset managers must consider when acquiring another firm.

Will the acquired firm maintain an independent culture?

Will they stay in the same office or move into the acquiring firm’s office?

How will a compensation windfall from the acquisition impact the acquired team’s drive and motivation?

How will the acquiring firm’s stock price performance impact the acquired team’s motivation?

What shared services can the acquired firm benefit from, and how does that impact its culture and firm operations?

Will the acquiring firm provide distribution and investor relations resources, and will the way in which those resources sell the acquired firm’s products represent the culture of the acquired firm?

These are just some of the questions that both the acquiring firm and the acquired firm must answer in order to create a successful outcome through integration.

The most important question of all: Will culture — or a change in culture — impact investment performance for LPs?

Ultimately, culture often manifests itself in investment performance. The decay of culture might not show up right away in investment performance, but the firms that figure out how to do integration well will understand the importance of laying the foundation of culture from the outset of an acquisition so that they don’t end up having issues with investment performance and future fundraises down the line.

What’s next?

Speed matters, particularly in an industry where the big are getting bigger, and that trend doesn’t seem to be abating.

The race is on in private markets — both for traditional asset managers and alternative asset managers — so large firms know they need to move quickly in order to achieve a presence in the wealth channel. That could mean build, buy, or partner depending on the firm’s strategy, culture, and desire to integrate.

I expect the coming years to be defined by continued consolidation in private markets, as I wrote about a few weeks ago.

Perhaps the next interesting consolidation play? Technology.

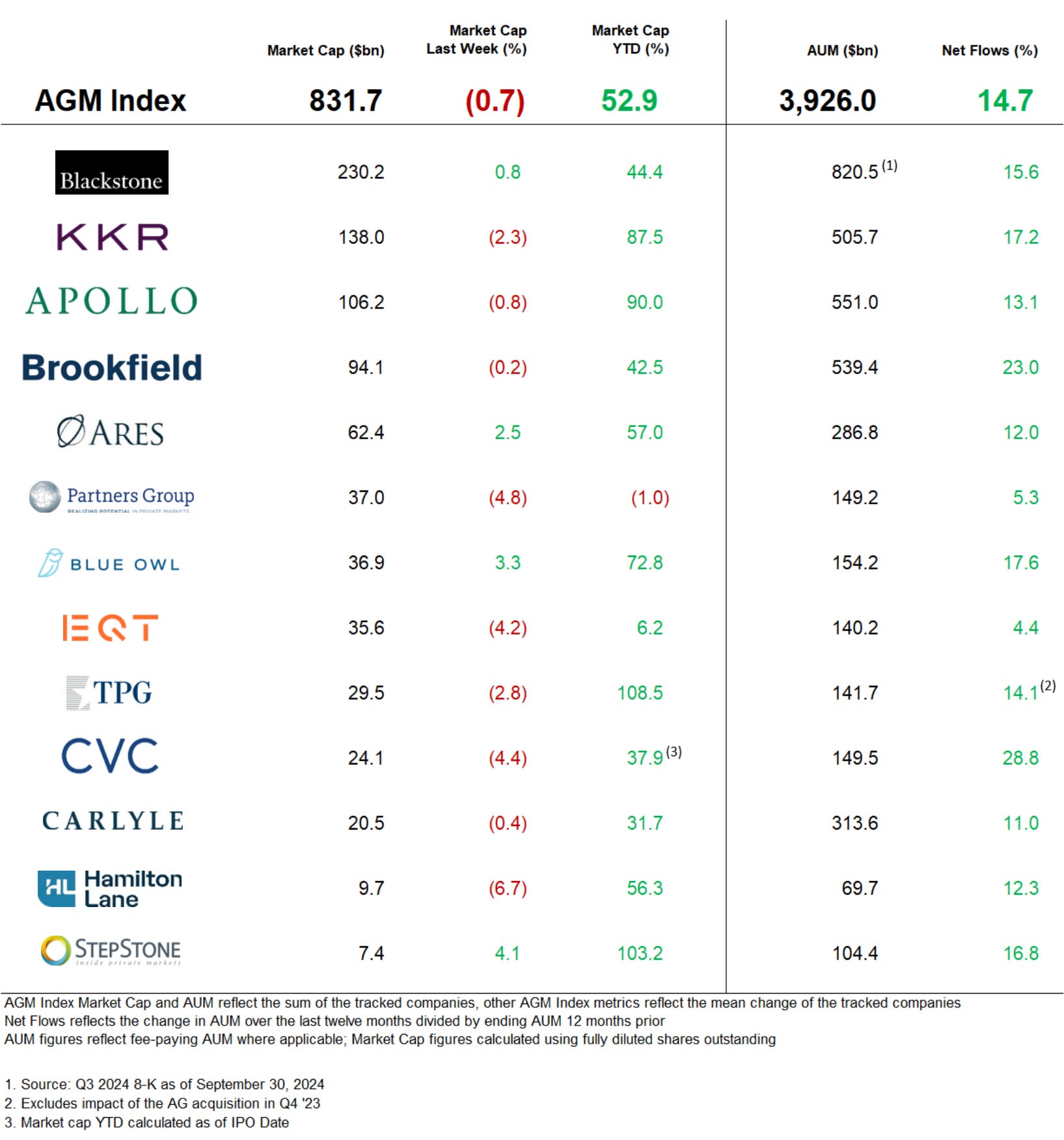

AGM Index

AGM has created an Index to track the leading publicly traded alternative asset managers.

Some of the industry’s largest alternative asset managers are publicly traded — and their net inflows can serve as a window into how private markets are being perceived by investors and allocators who are allocating capital into alternative investments.

Note: AUM figures are based on fee-paying AUM where applicable.

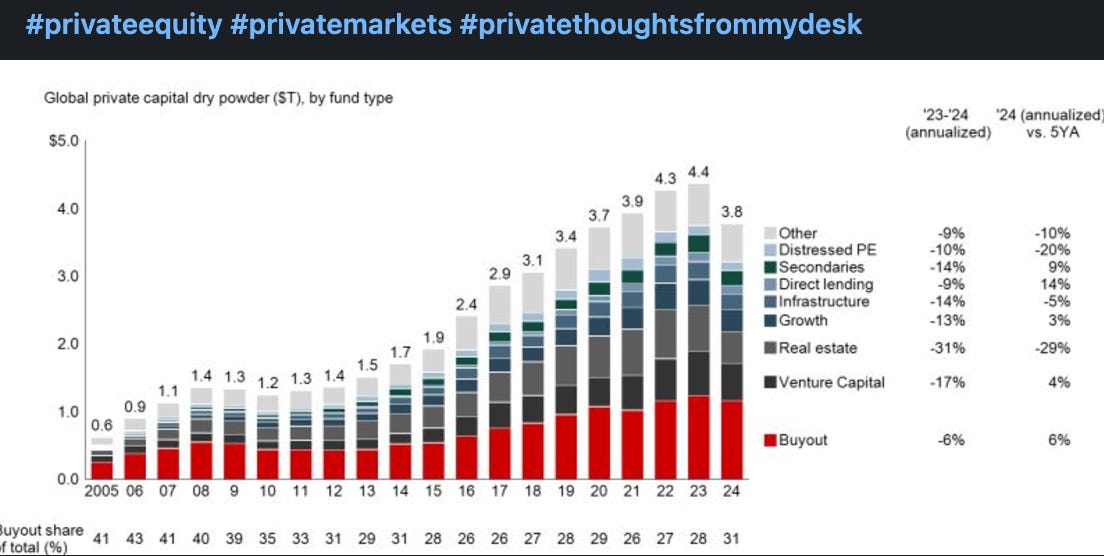

Post of the Week

Chairman of the Global Private Equity Practice at Bain & Company Hugh MacArthur shared a chart on LinkedIn that illustrates decreasing dry powder for buyouts.

Is this an early sign of a further decline in dry powder and a “healthy sign of normalization” for private equity?

AGM News of the Week

Articles we are reading

📝 Asset managers make existential dash into private assets | Antoine Gara, Financial Times

💡Financial Times’ Antoine Gara covers the growing trend of traditional asset managers pushing into private markets in a big way, either through acquisitions (such as BlackRock’s acquisition of GIP) or partnerships (such as KKR and Capital Group’s tie-up). It appears that many boardrooms believe they are in the midst of a fight for survival in an increasingly competitive investment landscape (see my weekly piece above for more on this topic). BlackRock, Franklin Templeton, and Capital Group in the US, and Amundi, Legal & General, Janus Henderson, and Schroders in Europe are all mentioned by Gara as leading the push into unlisted assets. Gara notes that private asset funds provide asset managers with the opportunity to earn higher fees than they would in their existing public markets products. But, as he also highlights, they also expose clients, particularly individuals and retirement savers, to new risks given the features of illiquidity and less frequent valuation cycles than public markets. The rise of evergreen funds has aimed to solve some of these challenges for wealth channel investors, offering LPs the ability to redeem a portion of a fund’s net asset value in any given quarter. But, as iCapital Chairman & CEO Lawrence Calcano said in a Bloomberg article last week, these funds are not entirely “liquid” products. Calcano said: “The idea of anything being marketed as semi-liquid never sits right with me,” he said. “Human nature is what it is; when people hear semi-liquid, we run the risk of people just hearing the word ‘liquid,’ and really, these types of assets and products comparatively speaking, are not liquid. Advisers and investors need to be attuned to that.”

Traditional asset managers are looking to figure out how to offer private markets products to their clients. And for good reason. Calcano told the FT that he sees this as a trend that will continue. “Most of the traditional asset managers are trying to figure out how to get into the alternatives space. Some of the firms, like Franklin Templeton, have gone out and made a few big acquisitions. Other people are figuring out how to partner with alternative asset managers. It is a trend we think is going to continue.” The recent acquisition of HPS by BlackRock would certainly suggest that the industry is in the middle of a consolidation phase, particularly for traditional asset managers that are looking to add capabilities to their investment platform, which will make for an interesting few years ahead for the industry.

💸 AGM’s 2/20: Private markets are in the middle of a major consolidation phase as both traditional and alternative asset managers are trying to figure out who they want to be and how they want to be who they want to be. Some firms, like BlackRock, have the size, scale, and public company currency to be acquisitive to the point where it will be a needle-mover for their platform. Others that don’t have the size and scale of certain firms will look to partner. Some firms have “build” in their DNA, so they will look inward rather than go down the path of buy and integrate, which, as I discuss above, is no simple feat. There is no single “right answer” for how a firm decides to enter private markets, but it feels like now is the time for them to make a decision. There are only so many firms left at the size and scale of HPS for a large asset manager to acquire. AGM’s Next Wave highlights some of the possible chess moves left on the board. Size isn’t the only consideration; culture must be factored in. That whittles down the possibilities of firms to be acquired by either traditional asset managers or larger alternative asset managers.

Some firms may choose to build. But that brings to bear questions about speed to market and brand. A traditional asset manager that chooses to build private markets capabilities might face questions from LPs about whether or not this is truly a core competency — and a true focus area for the firm. And how long will it take a firm to build these capabilities in-house? Identifying the right team, building the firm’s infrastructure and compensation plan, and raising capital all take time. That’s why the middle way of partnership might suit many firms best, as KKR and Capital Group have done. But partnership also raises crucial questions that must be answered. What becomes of brand in a partnership? Who is doing the investing? Who is doing the distribution? How will the partnership work?

There’s no simple answer to the chess moves that firms must make in this rapidly expanding and increasingly competitive ecosystem. But what’s clear? It certainly seems like the time to move is now.

📝 KKR’s Nuttall Presses Case for Private Assets in 401(k) Plans | Allison McNeely, Bloomberg

💡Bloomberg’s Allison McNeely reports on KKR’s Co-Chief Executive Scott Nuttall’s comments at the Goldman Sachs Financials Conference earlier this week. Nuttall said the long-term nature of 401(k) structures makes them a sensible vehicle for private markets investments. “People are saving for retirement in this target-date format, ” Nuttall said Tuesday. “They’re thinking about their asset allocation decades out — not having private markets as part of that solution just isn’t really sensible.” Bringing private markets investments into retirement solutions is not a simple task, which is something that Nuttall acknowledged. He noted that plan administrators will require safe-harbor protection from lawsuits in order to gain comfort investing into private markets. But it’s also KKR’s “hope and expectation that those protections will develop over time,” Nuttall said. Next year, KKR will focus on building and distributing products for individuals like retirement savers. Expanding the firm’s Global Atlantic insurance business and its long-term private equity ownership unit, KPEC, are also areas of focus. KKR is one of the largest and fastest-growing alternative asset managers, with $624B AUM as of September 30. The firm has made a major push into the wealth channel, building a product suited for individual investors and their advisors, K-Series. K-Series has $14B of AUM, up from $5B a year ago.

💸 AGM’s 2/20: KKR’s Nuttall highlights one of the next big frontiers for private markets: retirement assets. It’s early days for retirement assets having exposure to private markets products, but the trend is starting to pick up steam. A few weeks ago, I wrote about Fidelity International’s Diversified Private Assets LTAF (Long-Term Asset Fund) being inserted into their FutureWise investing strategy for UK-based workplace pension schemes. CITs have also provided for private markets assets to be included in their vehicles, and it’s something that one of the pioneers of private markets evergreen structures, Partners Group, has already done. The prize is certainly large. What’s at stake is trillions of dollars of assets to be unlocked to flow into private markets — and the industry has yet to even scratch the surface of what can be achieved here.

📝 Blackstone’s Wealth Boss Targets $1 Trillion in Assets | Benjamin Stupples and Anna Edwards, Bloomberg

💡Bloomberg’s Benjamin Stupples and Anna Edwards sat down with Blackstone’s Global Head of Private Wealth Solutions (PWS) Joan Solotar last week to discuss how she’s steered the firm’s wealth business and surpassed the firm’s $250B fundraising target four years ahead of schedule. Over the past five years, Blackstone’s PWS has grown its AUM by almost 5x as part of a global expansion by the firm into the wealth channel. In this interview with Bloomberg, Solotar discusses the firm’s evolution and next set of goals.

What’s next for Blackstone PWS after $250B?: “What’s next is $1 trillion, I hope,” said Solotar. She notes that the plan is to “build this business into something even more scalable.” She believes that they can double or triple the business over time.

Increasing allocations: Solotar said many allocators are looking to increase their allocations to private markets: “around the world you’re seeing an increase in private market allocations from virtually 0%. Most chief investment officers have a target of somewhere between 20% and 30% recommended private investments in a portfolio.”

“The path of travel is clear”: Solotar believes “the path of travel is clear: individuals will allocate more [to private markets].” She believes that private markets have reached the point where the various pieces of the puzzle across product development, technology, education, and operations and reporting have been unlocked to enable more investors to access private markets: “Private markets not only provide higher returns, but they’re also less correlated to stocks and bonds and provide good diversification. There are also more accessible quality products, while technology and education is getting better as well. To me, all of those are needed to unlock the market, and they’re happening simultaneously.”

Being a global business provides an advantage: Solotar discusses the nuances of working with investors in different regions of the world. There are not many firms that have the size and scale to be able to serve investors globally — and brand certainly factors into the equation.

💸 AGM’s 2/20: The macro trend is clear: private markets investments look like they will become a larger part of investors’ portfolios. Solotar’s comments illustrate just how early the industry is in its work with the wealth channel. Her views on how much Blackstone’s PWS business can scale AUM also signal that there’s plenty of room to run — for Blackstone and others in the industry. And while some may look at the $1T AUM number of private wealth assets that will be managed by Blackstone as a lofty ambition, I certainly wouldn’t bet against her or Blackstone. She and her team delivered on their $250B AUM goal — early, for that matter — so it would be far from surprising to witness a successful climb of the next mountaintop, particularly as we all know how much size and scale matter in private markets.

Who is hiring?

In order for alts to continue to go mainstream, we need the best talent to go into the space. Here are some openings at private markets firms. If you’d like to connect with any of these teams, let me know, and I’m happy to facilitate an introduction if appropriate. If you’re a company or fund in private markets, feel free to reach out to share a job description you’d like to be listed here to highlight for the Alt Goes Mainstream community.

🔍 Blackstone (Alternative asset manager) - Private Wealth Solutions - Product Marketing, VP, EMEA. Click here to learn more.

🔍 Apollo (Alternative asset manager) - Distribution & Wealth Services Associate. Click here to learn more.

🔍 iCapital (Private markets infrastructure investment platform) - RIA, Family Office Business Development - VP. Click here to learn more.

🔍 Vanguard (Asset manager) - Venture Investing - Senior Associate. Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Private Wealth Strategy Senior Lead - Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Private Wealth, Head of RIA Channel Marketing, Principal - Click here to learn more.

🔍 Blue Owl (Alternative asset manager) - Private Wealth, Alternative Credit Product Marketing, Vice President - Click here to learn more.

🔍 BMO (Asset manager) - VP, GAM Alternative Investments, Investor Relations. Click hear to learn more.

🔍 Hamilton Lane (Alternative asset manager) - Vice President, Data Intelligence. Click here to learn more.

🔍 JPMorgan (Asset manager) - Alternative Investments, Head of Alternative Investment Strategy and Market Intelligence. Click here to learn more.

🔍 Sagard (Alternative asset manager) - Head of National Accounts, Private Wealth Solutions. Click here to learn more.

🤝 Interested in partnering with Alt Goes Mainstream? 🤝

Alt Goes Mainstream is a community of engaged experts and executives in private markets.

Fill out this form using the link below to explore partnership opportunities.

The latest on Alt Goes Mainstream

Recent podcast or video episodes and blog posts on Alt Goes Mainstream:

🎥 Watch the second episode of Going Public on Alt Goes Mainstream with Evercore ISI Senior MD and Senior Research Analyst Glenn Schorr as we discuss trends and business models for the publicly traded alternative asset managers. Watch here.

📝 Read about the launch of the AGM Studio, a collaboration between Alt Goes Mainstream and Broadhaven Ventures to incubate, invest in, and help scale companies and funds in private markets. Read here.

🎙 Hear Balderton Capital General Partner and former Goldman Sachs Partner Rana Yared discuss why Europe can build global companies out of the region. Listen here.

🎙 Hear Churchill Asset Management by Nuveen’s MD, Senior Investment Strategist & Co-Head of the Chicago Office Alona Gornick discuss the evolution of private credit, the power of permanent capital, and the importance of the product specialist. Listen here.

🎥 Watch Stepstone Private Wealth CEO Bob Long discuss StepStone Private Wealth’s edge and nuances with their evergreen structures in the first episode of “What’s Your Edge.” Watch here.

🎙 Hear $5B AUM Ritholtz Wealth Management’s Director of Institutional Asset Management Ben Carlson bring a wealth of common sense to asset allocation and private markets. Listen here.

🎙 Hear Blue Owl, Inc. Board Member and Blue Owl GP Strategic Capital Senior Managing Director Sean Ward on how $57.8B AUM Blue Owl GP Strategic Capital has pioneered GP staking and transformed GP stakes into an industry. Listen here.

🎥 Watch HGGC Partner, Chairman, Co-Founder & Former NFL Hall of Fame Quarterback Steve Young and True North Advisors CEO & Co-Founder Scott Wood discuss how “the score takes care of itself” on the field and in investing / wealth management. Watch here.

🎥 Watch Eileen Duff, Managing Partner & Chief Client Success Officer at iCapital on episode 12 of the latest Monthly Alts Pulse as we discuss the future of AI and automation in private markets. Watch here.

🎥 Watch Co-Founder & Managing Partner of Cantilever Group and former Goldman Sachs and Broadhaven Capital Partners Partner Todd Owens discuss the middle market opportunity in GP stakes investing. Watch here.

🎙 Hear Intapp’s President, Industries, and Co-Founder of DealCloud by Intapp Ben Harrison discuss how data and automation are transforming private markets. Listen here.

🎙 Hear how a $1.59T AUM asset manager is approaching private markets with T. Rowe Price’s Global Head of Product Cheri Belski in a special live episode of the Alt Goes Mainstream podcast at a Pangea x AGM Breakfast in London. Listen here.

🎙 Hear Bernstein Private Wealth Management’s CIO Alex Chaloff discuss how a $125B wealth manager navigates private markets. Listen here.

🎙 Hear me discuss why and how alts are going mainstream on The Compound’s Animal Spirits podcast with Ritholtz Wealth’s Michael Batnick and Ben Carlson. Listen here.

🎙 Hear Mercer Investments’ US Financial Intermediaries Leader Gregg Sommer and CAIS’ MD and Head of Investments Neil Blundell on following the fast river of alts. Listen here.

🎙 Hear Manulife’s Global Head of Private Markets Anne Valentine Andrews share how to approach building a private markets investment platform at an industry behemoth and the merits of infrastructure investing. Listen here.

🎥 Watch Dan Vene, Co-Founder & Managing Partner, Head of Investment Solutions at iCapital on episode 11 of the latest Monthly Alts Pulse as we discuss the evolution of the industry. Watch here.

🎙 Hear Partners Group’s Co-Head of Private Wealth, Head of the New York Office, Member of the Global Executive Board Rob Collins share the how and why of one of the most exciting trends in private markets: evergreen funds. Listen here.

🎥 Watch Lawrence Calcano, Chairman & CEO at iCapital, on the AGM podcast discuss driving efficiency across the entire value chain to transform private markets. Watch here.

🎙 Hear VC legend New Enterprise Associates’ Chairman Emeritus and Former Managing General Partner Peter Barris discuss how he transitioned from operator to VC and transformed NEA into a venture juggernaut in the process. Listen here.

🎙 Hear Blue Owl’s Global Private Wealth President & CEO Sean Connor share insights and lessons learned from working with the wealth channel. Listen here.

🎙 Hear Ritholtz Wealth Management’s Managing Partner Michael Batnick share views on how wealth managers are navigating private markets. Listen here.

📝 Read about the evolution of GP stakes, why alternative asset management business models are better than SaaS, and our partnership with Todd Owens and David Ballard at Cantilever, a mid-market GP stakes firm anchored by BTG Pactual. Read here.

🎥 Watch internet pioneer Steve Case, Chairman & CEO of Revolution and Co-Founder of America Online, share lessons learned from building the first internet company to go public and an investment firm built for the Third Wave of the internet. Watch & listen here.

🎙 Hear how Chris Long, Chairman, CEO, and Co-Founder of Palmer Square Capital Management has built a $29B credit investment firm and a winning NWSL soccer franchise, the KC Current. Listen here.

🎙 Hear stories from building market-defining companies Blackstone, Airbnb, and private markets from Laurence Tosi, former CFO of Blackstone and Airbnb and Managing Partner & Founder of $7.6B investment firm WestCap. Listen here.

🎙 Hear Chris Ailman, the CIO of $307B CalSTRS, discuss how he manages a portfolio with ~40% exposure to private markets. Listen here.

🎙 Hear wealth management industry titan Haig Ariyan, CEO of Arax Investment Partners, share his thoughts on the private equity opportunity in wealth management. Listen here.

🎙 Hear Blackstone CTO John Stecher discuss how technology is transforming private markets. Listen here.

🎙 Hear investing legends John Burbank and Ken Wallace of Nimble Partners provide a masterclass on investing with both a macro and VC lens. Listen here.

📝 Read how 73 Strings CEO & Co-Founder Yann Magnan and team are leveraging AI to build a modern and holistic monitoring and valuation platform for private markets in The AGM Q&A. Read here.

🎙 Hear Robert Picard, Head of Alternatives at $117B AUM Hightower, discusses how they approach alternative investments. Listen here.

Thank you for reading. If you like the Alts Weekly, please share it with your friends, colleagues, and anyone interested in private markets.

Subscribe below and follow me on LinkedIn or Twitter (@michaelsidgmore) to stay up to date on all things private markets.

If you have any suggestions, would like me to feature an article, research, or would like to recommend a guest or topic for the Alt Goes Mainstream podcast, reach out! I’d love to include it in my next post or on a future podcast.

Special thanks to Michael Rutter and Nick Owens for their contributions to the newsletter.